#76 - What the Neobank Greats get Right (Free Read)

Evaluating which are the best Neobanks globally and looking at the factors that make them standout to inform future Neobanking efforts.

Illustrated by Mary Mogoi - Website

Hi all - This is the 76th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

Reach out at samora@frontierfintech.io for sponsorships, partner pieces and advisory work. Spaces are becoming limited on my advisory hours. I help clients with market entry, market mapping, strategic insights, sounding board to founders and general advisory across Pan-African Fintech.

Sponsored by Oradian

Built for Local Realities

Scaling a fintech or financial institution in Africa means navigating unique regulatory, operational, and market-specific challenges. Many global core banking solutions—built with mature markets in mind—lack the flexibility to accommodate local realities. A prime example? Loan fee structures. In many African markets, lenders need the ability to amortize fees over the length of a loan—a feature that most global core banking platforms don’t natively support. Fintechs and banks are forced to rely on cumbersome workarounds or build expensive custom solutions just to meet everyday business needs.

Oradian solves this by offering a core banking system designed specifically for dynamic markets. Our configurable platform adapts to local requirements, allowing financial institutions to operate seamlessly without compromise. From flexible fee structures to regulatory-ready workflows, Oradian provides the infrastructure you need to scale efficiently. Stop forcing global solutions to fit local challenges. Discover how Fairmoney uses Oradian to power its advanced lending business;

Introduction

Since the beginning of Nubank, we have believed that the future of financial services globally is of digitally-native companies. - David Velez;

Our vision is to evolve into a global AI-driven digital banking model that, in 20 to 40 years, banks 80% to 90% of the world population, and we don't have any branches. - David Velez

The reality of what we’re trying to achieve is to build a ten times better financial services company that is ten times cheaper as well - Nik Storonsky

Around 10 years ago, I was at a town called Bukavu in the DRC. It’s a trading town that sits at the border of Rwanda and DRC whilst having the beautiful Lake Kivu surround it. It was a business trip and I was there with some of the board members from the bank. Given we were in banking, the discussion largely centred around the regional banking sector. One of the board members quipped that “Kenyan Banks have had it good for the last 10 years, but now they’re about to get whats coming for them”. For him, that run of hyper growth from the early 2000s couldn’t go on for too long. I was of a completely different opinion but I bit my tongue given I was still wet behind the ears from a professional perspective.

Well, was he right? Since that time, total banking sector revenues in Kenya have almost doubled from around US$ 2.4 billion to US$ 4.7 billion representing a CAGR of 7.9%. The sector’s balance sheet has grown from US$ 24 billion to US$ 59 billion a growth of 2.4x and a CAGR of 10.4%. Whilst the CAGR’s are not exactly rock-star numbers, they’re not by any means a crisis. It’s been solid growth.

My insight at the time was that financial services in Africa are at ground zero in almost every metric. In 2013, 25% of adult Kenyans were considered to be completely excluded from financial services and a further 7.2% used informal financial services. By 2021, exclusion had dropped to 11.6% and it keeps dropping. Across the continent, only 12% of Africans have borrowed from a formal financial institution compared to over 65% in Europe. Kenya leads the pack due to Mobile Money. In South Africa, only 19% of the population has borrowed formally and in Nigeria this number ranges from 2-5% depending on your information source. The point was, there is so much to be done and there’s so much more growth to be had.

Whilst the last decade in Africa has been around enabling people to have store of value products, the next wave of financial inclusion will be all about empowering people through providing the right financial service at the right time and in the right context. This is what Nik Storonsky means when he says that the aim is to “build a ten times better financial services company that is ten times cheaper as well”. This is the insight that has enabled WeBank in China to onboard over 25% of the Chinese population onto its client base. David Velez in an interview with Nik Stebbings talked about how in the future, banks will be able to provide private banking type services through AI. This will enable an SME in Rio de Janeiro get the same quality of service from a digital relationship perspective as a Goldman Sachs corporate client.

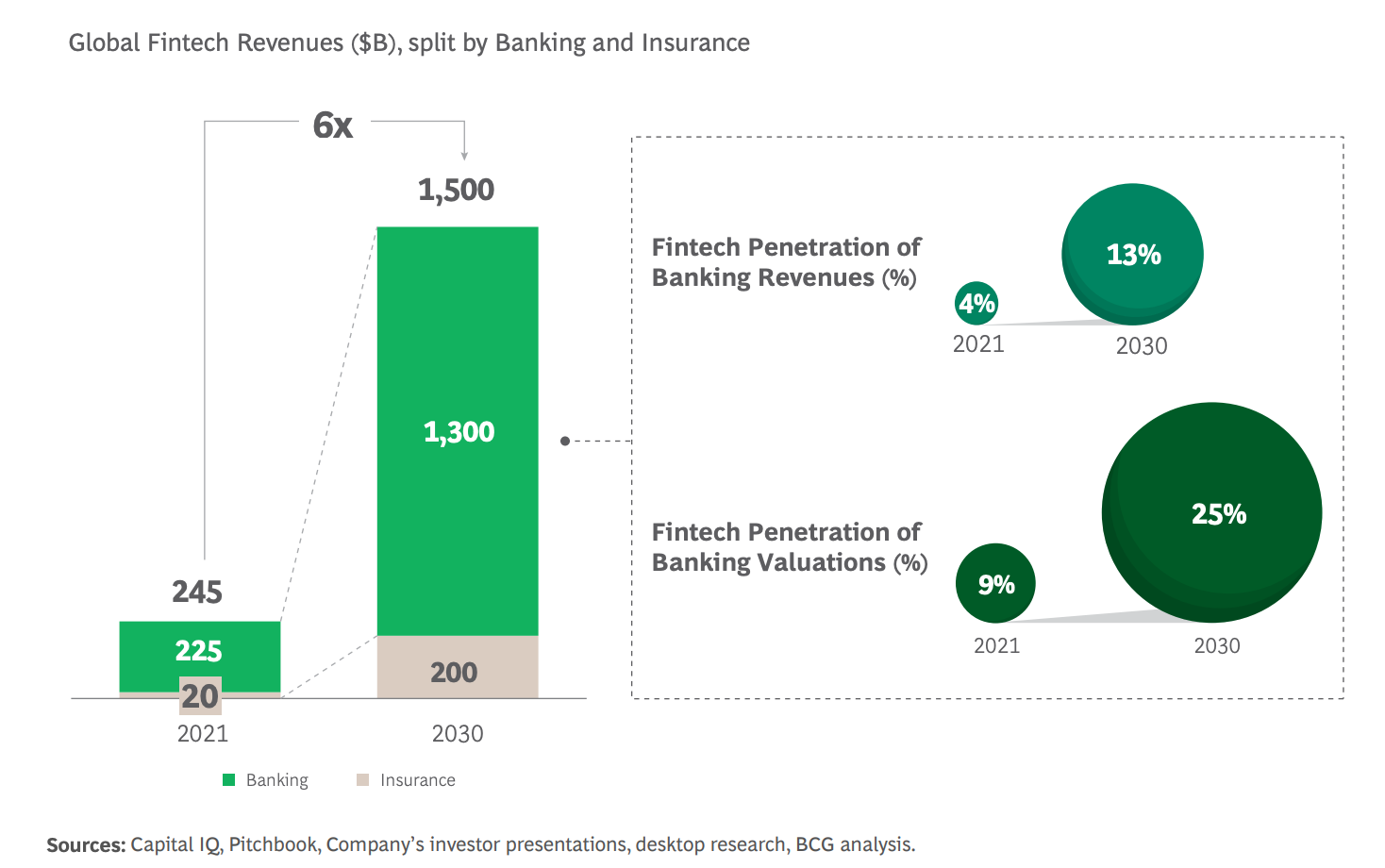

This in essence is the Neobank opportunity. A study by QED and BCG did a great job in highlighting it. Firstly, the financial services industry is the most profitable industry globally. Out of a total revenue pool of US$ 12.5 trillion, the FS industry generates profits of US$ 2.5 trillion representing a margin of 20%, one of the highest across all industries. On top of this, global banking and insurance revenues are expected to reach US$ 21.9 trillion in 2030 representing a CAGR of 6%. Of this, Neobank revenue penetration is expected to grow from 4-13% of total industry revenues. This means that Neobank revenues are expected to stand at US$ 2.7 trillion.

Source: BCG and QED

Interestingly, Africa is expected to have the highest growth. Whilst global growth is pegged at 6x, African Fintech revenues in banking and insurance are expected to grow by 13x. The diagram below shows how growth will differ across regions.

Source: QED and BCG Research

This may seem dramatic but it’s already happening. In Brazil, Nubank’s total revenues at the end of 2024 stood at US$ 11.5 billion with profits coming in at US$ 2.8 billion. For context, Itau Unibanco made US$ 7.2 billion dollars in profits in 2024. The top five banks in Brazil made US$ 21.3 billion in 2023. Nubank’s total revenues have grown by a CAGR of 223% over the last four years. Moreover, revenues are growing at twice the rate of operating expenses meaning that a 100% growth in revenues will lead to a 200% growth in profits. Assuming that it maintains a conservative 75% CAGR in profits over the next four years, Nubank’s total profits will stand at US$ 26.5 billion by 2028, exceeding the top 5 banks 2023 results. This is not a crazy outcome, it’s very likely to happen particularly as it expands. Nubank counts 50% of Brazilians as its customers and around 30% of Brazilians have Nubank as their primary bank account. This will only grow.

Revolut, Moniepoint, WeBank, Nequi, TymeBank are all executing this playbook and will likely exceed the BCG projections of achieving a 13% penetration of industry revenues.

The future is being built and it's important to understand; who are the current winners in the Neobank game and more importantly, what are they getting right? Ideally, this should provide a playbook for investors, founders and executives in banks to shape their digital banking strategies. I argued in a past article that each generation creates bank winners who end up being top 1 or 3 players in their markets. This is likely to happen with the current generation of Neobanks and moreover, the current generation has AI as a tailwind enabling a real paradigm shift in the way financial services are delivered.

In this article, we’ll analyse 16 global neobanks from a number of criteria, narrow down to the top 6 and evaluate any similarities across a number of dimensions such as tech platform, background of founders etc. Through this, we’ll be able to come up with some insights into what the successful ones have gotten right and hopefully what traits future Neobanks have to possess for them to join this hallowed group.

Who are the Existing Winners in the Global Neobank Space

The Neobanks

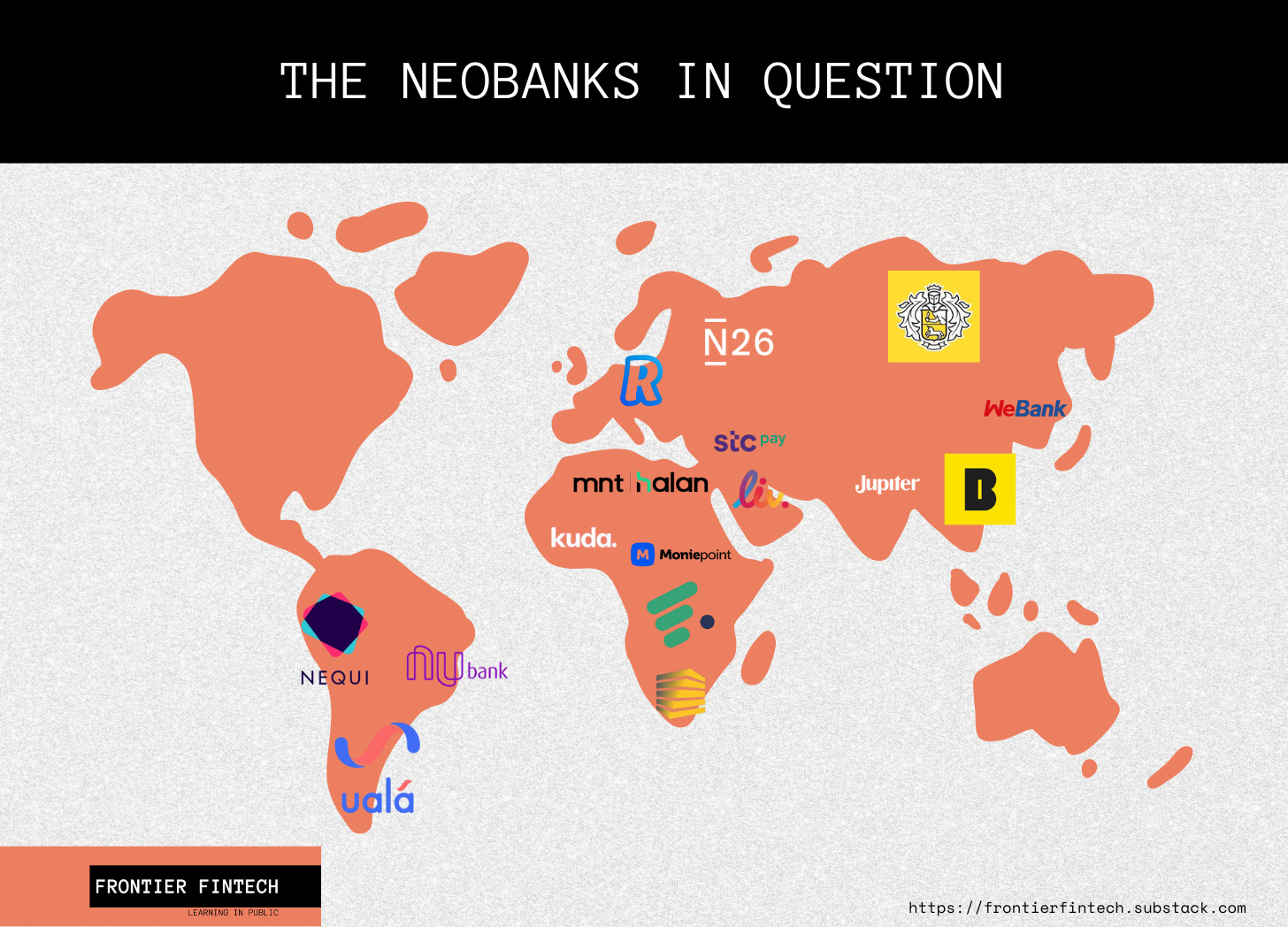

I started off by selecting some of the biggest names in global neobanking. The criteria was simply around the amount of funding raised and market dominance within the specific region or country. There was not much science behind this and it was an effort aided by my army of AI assistants. Nonetheless, one would argue that the selection process highlighted the most interesting Neobanks in the different regions across the world. I specifically left out the USA because aside from SoFI, most other American Neobanks operate on inter-change models and partner banking. This weakens the case for Neobanks becoming key banks in the markets in which they operate in. Nonetheless, leaving out the USA doesn’t weaken the analysis at all. The Neobanks selected are;

Africa

Fairmoney provides digital banking and instant loans up to ₦3M to over 9 million customers via its app and agent network. It targets Nigeria’s unbanked, expanding into India with a hybrid model.

Kuda offers digital banking and free transfers to over 8.5 million customers through its app. It focuses on financial inclusion in Nigeria’s 200 million-strong market.

Moniepoint delivers banking and payment solutions to over 10 million customers via its app and agents. It processes over 1 billion monthly transactions with its proprietary system.

TymeBank provides digital banking to over 10.7 million customers through its app and retail partnerships. It’s South Africa’s first digital bank, recently achieving unicorn status.

Asia

Jupiter offers digital banking and investments to over 6 million customers via its app. It enhances financial access in India’s 1.4 billion market with UPI services.

KakaoBank provides digital banking to over 24.88 million customers via its app and KakaoTalk. It’s South Korea’s first mobile-only bank, serving nearly half of 51 million people.

WeBank delivers microloans and payments to over 400 million users via its WeChat Mini Program. It’s China’s first internet bank, handling 840 million daily transactions.

Europe

N26 offers digital banking to over 8.7 million customers across 24 European markets via its app. It provides seamless banking in a market with over 400 million people.

Revolut - UK and Global (Europe-focused)

Revolut provides banking and crypto to over 50 million customers in 38 countries via its app. It’s UK-based with licenses in the UK and EEA.

Tinkoff offers digital banking and investments to over 43 million customers via its app. It’s Russia’s “super app” bank, serving 145 million people.

Latin America

Nequi provides digital banking and nanocredits to over 25 million customers via its app. It’s a Bancolombia spin-off, serving Colombia’s 50 million population.

Nubank - Brazil, Mexico, Colombia

Nubank offers banking and credit to over 114 million customers via its app. It’s Latin America’s largest neobank, operating in a 500 million-person region.

Uala delivers digital banking and credit to over 5 million customers via its app. It targets financial inclusion in a 150 million-person market.

Middle East and North Africa (MENA)

Liv Bank provides digital banking and lifestyle services to ~900,000 customers via its app in the UAE. Launched by Emirates NBD, it targets millennials in a 10 million-person market.

MNT Halan offers banking and loans to over 8 million customers via its app and 100+ branches across Egypt, Turkey, Pakistan, and the UAE. Its Neuron platform serves the region’s unbanked.

STC Bank delivers digital banking and investments to over 12 million customers via its app in Saudi Arabia. It supports Vision 2030 goals for 36 million people as an STC subsidiary.

The Filtering Mechanism

Once I selected the 16 challenger banks that I want to analyse, it was important to come up with a criteria. The criteria should cover growth, customer affinity and impact in their respective markets. The metrics chosen to convey these qualities are;

Average Customer Growth Rate: Measures the average yearly increase in total customers over the past five years, reflecting a neobank’s ability to expand its user base.

Average Revenue Growth Rate: Tracks the average yearly revenue growth over five years, indicating financial scalability.

Customer Rating: Uses app store ratings adjusted for the number of reviewers (e.g., 4.9 from 5 million vs. 50,000) as a proxy for satisfaction, due to limited NPS data.

Profitability: Assesses whether a neobank is profitable, breaking even, or losing money, noting scale varies by market but status is key. The scale of the profitability is not what’s being measured, simply whether it’s profitable or not.

Operating Leverage: Compares revenue growth to expense growth (revenue change ÷ expense change), using estimates where data is incomplete, to gauge efficiency.

Product Velocity: Ranks speed of product releases over 24 months (very high to low), highlighting a competitive edge in tech-driven markets.

Customer Penetration: Calculates the percentage of a market’s population as customers (e.g., Nubank’s 50% in Brazil, 28% overall), showing market impact.

Data Control: Scores data quality and availability, favoring neobanks like Nubank and Tinkoff, to mitigate estimation errors.

Each variable is ranked out of 10 to give a simpler ranking mechanism. For instance, a company whose customer growth rate is 100% and above would be ranked 10 whereas one who’s growth is 40% would get 4 points. If a company has grown at 200%, it will be given a 10. Whilst imperfect, it enables standardisation. For variables such as profitability and product velocity, I’ve assigned scores based on the specific variable. For instance, very high product velocity gets 10 points, high gets 7.5 points and low gets 2.5 points. Whilst not perfect, it gives results that can actually tell a story.

The Results

Notes on the Outcome;

Data quality was a major issue particularly for some entities like Uala, Liv and Kuda. This adversely affected their results;

There’s a large group between STC Pay and TymeBank that are very close in their outcomes and thus it's hard to make a distinction between them;

Nubank did very well based on growth metrics for both customers and revenue. Additionally operating leverage, product velocity and specifically its impact made it stand out. Over 28% of the population of Mexico, Colombia and Brazil have a Nubank account, that’s a population of over 360 million people.

Revolut does really well on all metrics except impact. Revolut is in over 38 countries whose combined population is 1.2 trillion whilst only having 50 million customers. This is a core difference between Nubank and Revolut. David Velez in a podcast interview mentioned that for Nubank they want to go to fewer countries but go deep in each market to be the primary account for the bulk of the population. Revolut on the other hand have a plan to be in 100 markets whilst generating revenues of US$ 100 billion;

Moneipoint does well largely due to its extreme growth. If the growth rankings weren’t capped at 10, Moniepoint would easily be ahead of Revolut and Nubank. In the last five years both revenue and customer numbers have grown at over 200% on average and continue to scale at this incredible pace. Moreover, Moniepoint has been profitable for most of its existence. Moniepoint loses ground based product velocity which is high but not as high as those of Revolut and Nubank. Nonetheless now that they are doing consumer banking, I expect that in a year, their rate of product velocity will be as high or exceed that of Nubank and Revolut. Moreover, Moniepoint is growing but their 10 million customers are only 0.44% of the population. Lastly, Moniepoint doesn’t publish its results so it suffers from a data reliability gap. All that being said, in a couple of years, I expect it to comfortably lead the rankings;

WeBank comes fourth on the list. If this ranking was done 5 years ago, WeBank would be well ahead of everyone else. With over 360 million customers, customer and revenue growth are harder now than they were 5 years ago. It’s a leader in product velocity and impact;

Nequi is an interesting inclusion. With over 25 million customers, it has a great impact affecting 48% of Colombia’s population. Moreover it has been growing rapidly whilst proving incredible operating leverage. It’s an interesting one because it’s one of the few Neobanks that has emerged from a commercial bank. It has nonetheless not achieved the revenue growth rates of some of its peers;

Tinkoff or T-Bank as it is now called remains a leader in the Neobanking category as it continues to show strong growth and sustained profitability. No mention of global Neobank leaders can ignore this company;

From an African perspective, Fairmoney does well from a revenue growth perspective and in terms of product velocity. It suffers nonetheless from its impact and the availability of data. Tymebank on the other hand suffers from impact and recent customer growth which has slowed down a bit. Lastly, it has a lower customer rating score than its peers Nubank and Revolut largely based on the number of people who have rated it on the respective app-stores.

Analysis

With our chosen six, it’s useful for current Neobank investors and builders to understand what core characteristics matter if anything for success. I’ll look at seven dimensions that range from tech choices, market dynamics and the structure of the organisation and team.

Proprietary Banking Platform

Nubank - Proprietary core platform

Revolut - Proprietary core platform

Moniepoint - Proprietary core platform

WeBank - Proprietary core platform

Nequi - Third-party platform (Finacle)

Tinkoff - Proprietary core platform

Over the past decade, new digital banks have increasingly built their own tech, including core banking systems that manage ledgers, products, and integrations like crypto and AI, driving product velocity essential for customer acquisition and loyalty in a fast-evolving landscape. Of the six banks, all except Nequi (using Finacle) have proprietary core platforms, with Revolut and Nubank exemplifying this vertical integration—Revolut building everything in-house in a vertical integration model that mirrors Standard Oil. Nubank’s tech focus was validated when Sequoia’s Doug Leone, initially skeptical of CTO Edward Wible, saw a board member fully endorse his platform decisions.

Having said that, I argued in an older post that part of the decision to build core banking systems back then was down to the core banking ecosystem then. There were very few truly cloud-native systems that could provide the platform that a Neobank needed. Fairmoney for instance has shown impressive product velocity whilst relying on Oradian as a core banking platform. TymeBank has also built a multi-country operation relying on Mambu. I however think that with Nubank leading their most recent funding round, the idea could be to migrate Tymebank to Nubank’s global platform.

Existing Market Dynamics

I always argue that every country has an M-Pesa moment where the right product, team, technology and organisation meet a failed market. This is the back-story to every generational financial services company. 25 years ago it was Equity Bank, Capitec and Access Bank. The core conditions that must exist is that their has to be a serviceable market that has completely been ignored and which can now be profitably served using a new technological approach. For Nequi and Nubank the issue was a highly concentrated banking system that is super profitable as well as a market that has been excluded on the basis of the market structure of the banking system.

Every company in the top 6 has attacked a market that has largely been ignored by incumbent organisations and applied technological prowess to serve that market in a new and profitable way;

Nubank - A no-fee credit card via an app tackled Brazil’s 30% unbanked—60 million of 200 million—in a concentrated banking system.

Revolut - A multi-currency app with low-cost forex served Europe’s constrained users, despite only 10%—40 million of 400 million—being unbanked.

Moniepoint - A digital payment platform with POS capabilities addressed Nigeria’s 40% unbanked—68 million of 170 million—in a cash-heavy market.

WeBank - A WeChat-integrated microloan service targeted China’s 40% unbanked—over 500 million of 1.4 billion—ignored by traditional banks.

Nequi - A free digital wallet app served Colombia’s 25% unbanked—12 million of 48 million—facing high fees in 2016.

Tinkoff - A digital credit card platform addressed Russia’s 20% unbanked—29 million of 145 million—in an inefficient system in 2006.

All of the companies above had a unique approach to a significant problem in the delivery of financial services. The problems were structural in nature. For Moniepoint for instance, banks didn’t have the requisite cultural and technological capabilities to provide off-line merchant capabilities and the Fintechs that existed largely provided on-line acceptance targeting a Pan-African market from the start. I argued in a recent article that the nature of the market is the biggest determinant of success. That is why successful credit focused Neobanks such as Fairmoney and Carbon have emerged in Nigeria.

Product Focus

Different Neobanks launch with different products. For instance, Fairmoney, MNT-Halan, Nubank and Tinkoff all led with credit. Revolut and Moniepoint led with payments. Is there a relationship between the nature of your core product and the probability of success? Below are what our chosen six decided to focus on;

Nubank - Credit - Launched in 2013 with a no-fee credit card to serve Brazil’s unbanked in a high-fee market.

Revolut - Payments - Introduced in 2015 with a multi-currency app for low-cost payments in Europe.

Moniepoint - Payments - Emerged with a payment platform riding on agents and merchants to tackle Nigeria’s cash-heavy economy.

WeBank - Credit - Began in 2014 with microloans via WeChat to reach China’s vast unbanked population.

Nequi - Store of Value (Wallets) - Launched in 2016 with a digital wallet to simplify banking for Colombia’s excluded.

Tinkoff - Credit - Started in 2006 with a digital credit card to bypass Russia’s inefficient banking system.

No single service dominates the list, Nubank, WeBank and Tinkoff have led with credit whilst Moniepoint and Revolut led with payments. Nequi on the other hand launched with a digital wallet. They have all broadened their offerings so Revolut and Moniepoint have launched lending products whilst Nubank has gone deeper into payments. What this means is that there’s no right way to launch a Neobank. It’s all contextual and dependent on the previous prescriptions around the nature of the market. That being said, I find that credit products particularly in Africa enable you to earn significant revenues earlier on. However this is all dependent on whether you build out your credit operation properly.

Distribution

Building a great product is great, getting it to your customers in the right manner at the right price point is even greater. The approach through which Neobanks then build distribution matters.

Nubank - Purely Digital - Nubank distributes its credit card and banking services entirely through a mobile app, targeting Brazil’s unbanked without physical branches or agents.

Revolut - Purely Digital - Revolut offers its payment accounts and services solely via a mobile app, serving customers globally with no physical infrastructure.

Moniepoint - Mix of Digital and Physical - Moniepoint combines its mobile app with an agent network to deliver payment and banking services in Nigeria’s cash-heavy market.

WeBank - Purely Digital - WeBank provides its microloan and payment services exclusively through a WeChat Mini Program, reaching China’s unbanked digitally.

Nequi - Purely Digital - Nequi delivers its digital wallet and banking services entirely through a mobile app, serving Colombia’s excluded population.

Tinkoff - Mix of Digital and Physical - Tinkoff uses a mobile app for banking but employs couriers for card delivery and KYC, blending digital and physical distribution in Russia.

Most neobanks operate purely digitally, except Moniepoint and Tinkoff, which blend physical and digital—Moniepoint mirrors Block by managing merchants physically and engaging consumers digitally, while Tinkoff built a proprietary courier network to meet Russia’s KYC laws, later turning it into a competitive advantage—and WeBank leverages WeChat’s vast ecosystem for scale. In Africa, Moniepoint, TymeBank, and Fairmoney highlight the hybrid model’s edge, with Adia Sowho, ex-CMO of MTN Nigeria, arguing in Afridigest that “distribution equity—built through presence, price, and accessibility—outweighs brand equity from marketing spend in African markets, where trust hinges on tangible touchpoints,” and Shameer Patel, I&M Bank’s Retail and Business division lead, revealing in an upcoming podcast that opening a physical branch spikes digital onboarding in that location, as customers trust the brand more even if they never visit.

Approach to Banking License

In Fintech, there has always been debate about licensing as a Neobank. One one hand, the US model relies on bank partners with the argument that being a bank slows you down and will affect your valuation. Both David Velez of Nubank and Nik Storonsky of Revolut have repeatedly argued that this completely misses the point. For Nik Storonsky, his argument is centred around the lack of control that comes with having a bank partner given that they have to approve even marketing material. For David Velez, his argument is centred around the idea that being a primary bank is the core long-term differentiator that drives long-term sustainability. In my view what matters is not so much whether a Neobank is licensed but rather its founders approach to licensing. The Neobanks are listed below;

Nubank - As per different sources, Nubank has a full banking license in Brazil. In Mexico, it is gearing up to get a full banking license whereas in Colombia it works with Bancolombia as it aims to get a license there in the future. Having said that, their IPO prospectus expressly states that none of their Brazilian subsidiaries is licensed to operate as a bank so this is a point of confusion. Their core companies in Brazil have Payment and Financing Institution licenses that enable them to provide credit and payment services. Nonetheless as discussed, David Velez the founder has mentioned that they want to be the primary bank for their entire client base so full licensing must be on the cards. Remember, the intention to get licensed is what is being evaluated;

Revolut - Holds a UK banking license (July 2024, initially restricted) and a Lithuanian banking license (2018), transitioning from an e-money institution since 2015. Founder has mentioned the goal to be a global bank;

Tinkoff - Operates with a full banking license from the Central Bank of Russia since its founding in 2006 as Tinkoff Credit Systems.

WeBank - Launched with a full banking license from the China Banking Regulatory Commission in 2014, Tencent’s first banking venture;

Moniepoint - Holds a Microfinance Bank (MFB) license from the Central Bank of Nigeria since April 2022, not a full banking license; a commercial banking license application is in process as of November 2024.

Nequi - Operates under Bancolombia’s full banking license since its launch in 2016, lacking an independent full banking license of its own.

All the successful Neobanks are clear that banking is the ultimate goal and this clarity has existed from the start. This in my view is a characteristic that consistently shows itself amongst the top Neobanks. In a discussion with a founder in the space for an up-coming podcast episode, he highlighted that he wishes he had this clarity from the start as it would have prepared him for the complexity of running a bank.

Founder Background

The debate over whether domain expertise or a fresh perspective drives success in neobanking leans toward expertise, as seen in founders like Nubank’s Cristina Junqueira (banking operations), Revolut’s Nikolay Storonsky (FX trading), Moniepoint’s Tosin Eniolorunda and Felix Ike (payment systems), and Tinkoff’s Oliver Hughes (Visa payments), who brought industry know-how to their ventures. While outsiders like David Vélez and Oleg Tinkov innovated, they relied on experienced co-founders or advisors—Vélez with Junqueira and Tinkov with Hughes—suggesting domain expertise enhances execution, a view Vélez reinforced in a podcast, wishing he’d hired more seasoned operators early on.

Nubank -

Founders: David Vélez, Cristina Junqueira, Edward Wible;

Backgrounds: Vélez analyzed markets at Goldman Sachs and Sequoia; Junqueira managed operations at Itaú Unibanco; Wible engineered software at tech firms.

Revolut

Founders: Nikolay Storonsky, Vlad Yatsenko

Backgrounds: Storonsky traded at Lehman Brothers and Credit Suisse; Yatsenko built systems at UBS and Deutsche Bank.

Moniepoint

Founders: Tosin Eniolorunda, Felix Ike (via TeamApt)

Backgrounds: Eniolorunda managed engineering at InterSwitch; Ike engineered payment systems there, later building bank software at TeamApt.

WeBank

Founders: Tencent-led (key figure: Gu Min)

Backgrounds: Tencent, under Ma Huateng, ran WeChat’s ecosystem; Gu Min worked in finance at Ping An Insurance.

Nequi

Founders: Bancolombia initiative (Juan Carlos Mora)

Backgrounds: Mora led Bancolombia’s banking operations; its IT team brought financial tech experience.

Tinkoff

Founder and Key Figure: Oleg Tinkov, Oliver Hughes (early CEO)

Backgrounds: Tinkov ran a brewery and retail chain; Hughes led Visa’s operations in Russia.

Conclusion

The greatest Neobanks have all shown impressive growth, sustained profitability, product velocity and impact in terms of number of clients reached. Based on these metrics Nubank will continue to scale and Moniepoint could soon become a global leader based on my ranking system. Within a few years, product velocity will scale up and it will likely have over 25% of Nigerians on its platform. This is not a ridiculous take.

The successful Neobanks seem to have a few things in common;

Most of them have built their own proprietary tech platforms or at the very least, partnered with Neocore platforms that are cloud native;

All of them have founding teams that have domain expertise in the specific areas they’re building in. It doesn’t have to be banking in its entirety but the core initial product. Revolut had FX expertise, Moniepoint had payments expertise;

All of them are clear that they are banks and act like it from day one. Revolut for instance has world class reporting and all others have been clear on regulatory engagement from the start - This is a key point;

All of them solved a core problem around financial inclusion or empowerment with technology that fundamentally reduced the cost to serve thereby creating a new economic structure around that product.

Distribution is context specific - whereas China has a massive mini-app ecosystem, African markets require a mix of digital and physical.

Lastly, it doesn’t matter what specific wedge you start with. This again is context specific just like distribution;

These are the core things you need to get right to succeed in the Neobank game. It would be interesting to get your feedback especially on what metrics could be used to refine the analysis and what areas such as distribution and tech can be used to better evaluate them.