# 71 - How to Select A Fintech Market in Africa

What factors enable some markets to create more unicorns than others and why its important to understand them.

Illustrated by Mary Mogoi - Website

Hi all - This is the 71st edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

Reach out at samora@frontierfintech.io for sponsorships, partner pieces and advisory work. Spaces are becoming limited on my advisory hours. I help clients with market entry, market mapping, strategic insights, sounding board to founders and general advisory across Pan-African Fintech.

Sponsored by Skaleet

Overcoming technical debt through Robust APIs and Pre-Built Connectors

Integrating a new platform with a legacy core can be complex, but Skaleet simplifies this process with a powerful API suite and pre-built connectors for traditional core banking systems. These tools ensure smooth, seamless data flows across the bank’s operations, maintaining a unified customer experience. With Skaleet, banks avoid the usual disruptions associated with adding a new system, as Skaleet handles data synchronization and minimizes downtime during integration.

Skaleet also offers low-code / no-code extensibility tools designed to facilitate easy communication between the next-gencore and legacy systems as well as use cases’ customization needs, reducing integration complexity. These pre-built tools prevent operational disruptions and maintain data consistency, enabling banks to focus on delivering exceptional customer service without being bogged down by technical hurdles. This is crucial because in my view technical debt is the biggest latent blocker to product innovation in Africa’s financial system.

Introduction

When a great team meets a lousy market, market wins - When a lousy team meets a great market, market wins. - When a great team meets a great market, something special happens. - Marc Andreesen

In African tech circles, there are always conversations about which markets are venture markets and which ones aren’t. In the most recent Africa Tech Summit, one consensus perspective that was emerging was that Kenya is not good for venture particularly in Fintech. A number of factors were thrown about such as the quality of entrepreneurs and the commercial culture that exists. Things happen much faster in other markets such as Egypt and Nigeria as compared to Kenya. For sure, some of this is true. I think that there is a much more aggressive entrepreneurial environment in Nigeria and Egypt. When you put so many people within large agglomerations like Cairo and Lagos, you expect Darwinianism to lead to outstanding entrepreneurs emerging. However, that alone cannot explain what seem to be vast differences in venture outcomes across the continent, particularly in Fintech. All Unicorns are from Nigeria, Egypt and South Africa with none from markets such as Ghana and Kenya.

If you believe in Gaussian distributions, then you’d expect talent and grit to be evenly distributed across the continent. Therefore, if entrepreneurial talent is evenly distributed, something else must be driving the varying outcomes within the African Fintech ecosystem. With this in mind, I decided to lay down a framework for evaluating how attractive a Fintech market is and therefore the probability of a venture scale business emerging in that market. Whilst great entrepreneurs are critical to success, the right market is often the more critical factor. As Marc Andreesen wrote almost 20 years ago; “I'll assert that market is the most important factor in a startup's success or failure. Why?In a great market -- a market with lots of real potential customers -- the market pulls product out of the startup.”

To evaluate the quality of the market, you need a scientific approach. One that standardises variables across many markets and uses these variables to predict outcomes. Often, we hear about factors such as increasing internet penetration, economic growth, demographics and improving regulation. These are all true, but these are increasingly looking the same across most markets. Simply, they are beginning to cancel each other out. You have to dig deeper and find unique variables that can explain the different outcomes in the continent.

In this week’s article, we’ll determine the core factors that drive different Fintech outcomes in the continent, create a ranking framework that enables us to determine which market is “better” or has more potential, evaluate these rankings across five countries; Nigeria, Egypt, Ghana, South Africa and Kenya. Finally, we’ll use these rankings to make some predictions about where various Fintech opportunities exist in the different markets. As always, I’m inspired by the late Charlie Munger and the core mental model that will be used is the idea of Lollapalooza effects. As he said “"Lollapalooza effects occur when multiple forces or factors move in the same direction. The key is that when forces combine, they don’t just add up; each force builds off of and strengthens the other, creating an explosive effect with huge results." The factors that define Fintech outcomes are multiplicative in nature. Using this framework, it becomes clear why some markets offer up 10x the opportunity than other markets.

We’ll constrict the market opportunities to four segments; Neobanks and Digital Wallets, B2B Cross-Border Payments, Merchant Acquisition and Digital Credit Provision.

The Factors that Shape Markets

We need factors that explain why Moniepoint was able to take off in Nigeria but a similar model hasn’t taken off in Kenya despite the demographics, urbanisation and internet penetration stories. Why is Fido Credit in Ghana doing so well but a similar model is not hyperscaling in South Africa? There’s nuance and it’s important to unpack this nuance. I’ve narrowed down to four key factors that when looked at together can give an explanation into how Fintech in Africa has been shaped.

Below, I’ll walk you through some of the factors that I think matter;

FX Markets and Capital Account

Every country in Africa has a different approach to managing its capital account i.e. how easy it is to move money in and out of the country. Different countries have had different approaches to capital account liberalisation over the last 40 years. In the 70s and 80s most countries in the continent had relatively closed capital accounts and moving currency in and out was difficult. There was heavy licensing often regulated by the Central Bank or currency boards with opaque management.

In the 90s, a lot of this changed with many countries moving towards liberalising their currencies. The notes below show how FX is managed across different African countries;

🇳🇬 Nigeria (Partially Open)

✅ Allowed:

Foreign Direct Investment (FDI) is permitted in most sectors.

Portfolio investment (stocks, bonds) allowed but regulated.

Repatriation of profits and dividends is allowed with proper documentation.

Foreign loans can be accessed with approval from the Central Bank of Nigeria (CBN).

🚫 Restricted:

Strict FX controls and multiple exchange rates make it hard to access USD.

Some capital outflows are restricted or delayed.

Foreign loans require CBN approval.

Repatriating funds can be delayed during FX shortages.

The implications in Nigeria are that due to the FX controls, a parallel market develops. Simply, if there are restrictions on getting money out of the country, most businessmen will maintain off-shore balances and importantly, exporters won’t repatriate all the money they make. What then happens is that demand and supply don’t clear and there are pricing differences between the parallel markets and the official markets that reflect this imbalance. In such markets, large corporations have to work with banks and banks are always playing catch up to fulfil their FX requirements given this liquidity challenge. Given that banks will always prioritise their larger corporate clients, a massive market emerges for supporting the long-tail of importers and exporters with their cross-border payment challenges.

The thing to note about markets like Nigeria is that given that there has been a history of capital controls, a political economy is built around this scarcity. Connected businessmen and politicians participate in this political economy and there are entrenched interests in maintaining the status quo.

🇰🇪 Kenya (Open with some Restrictions)

✅ Allowed:

Foreign investment is welcome across most sectors.

Portfolio investment and foreign loans are permitted.

Profits and dividends can be repatriated (subject to tax compliance).

FX purchases and foreign payments are generally permitted;

🚫 Restricted:

Large FX transactions require justification (banks ask for purpose) but don’t restrict;

Central Bank intervenes to manage exchange rates when necessary - This is a normal operation to stabilise the economy;

Kenya has a relatively open capital account, there are few restrictions if at all on FX purchases by individuals and businesses. Moreover, local corporations can take hard currency loans and hold their balances in foreign currency. The restrictions that exist are largely KYC related but not specific restrictions on FX movements. In Kenya, like any African countries, there are liquidity challenges but these challenges are not endemic i.e. they tend to be seasonal. What this means is that most of the time, businesses will source FX from banks.

🇬🇭 Ghana (Partially Open)

✅ Allowed:

FDI and portfolio investments are permitted.

Repatriation of profits is allowed for foreign investors.

International loans and bond issuances are permitted.

🚫 Restricted:

FX shortages sometimes lead to USD restrictions.

Some capital outflows face controls (especially in crisis periods).

The Central Bank of Ghana limits forex speculation to stabilize the market.

Ghana shares a lot of similarities with Kenya, there is a relatively open capital account and markets only break during periods of crisis. Nonetheless, at a steady state, there is generally good liquidity in the market.

🇿🇦 South Africa (Partially Open – Advanced Market)

✅ Allowed:

Free movement of capital for FDI and portfolio investment.

No major restrictions on profit repatriation.

South African businesses can invest abroad with some approvals.

🚫 Restricted:

Large capital outflows require approvals.

Some limits on foreign borrowing by local residents.

Institutional investors must get approval for large offshore investments.

South Africa has an interesting capital account environment. It’s one of Africa’s most advanced economies thereby it benefits from significant FDI in key industries such as mining, banking and technology. It also has sufficient inflows due to a very strong export sector. Nonetheless, individuals face some controls in their FX purchases but these are mostly procedural i.e. you have to present specific documents to get access to currency. To this end, despite having some semblance of controls, South African businesses and individuals don’t struggle as much as their African peers to get access to currency for importing.

🇪🇬 Egypt (Partially Open)

✅ Allowed:

FDI is allowed in key industries (real estate, energy, manufacturing).

Portfolio investment is permitted but requires registration.

Profits and dividends can be repatriated.

🚫 Restricted:

FX controls are tight, especially during USD shortages.

Restrictions on USD withdrawals and outflows in times of economic stress.

The Egyptian government occasionally imposes capital controls to stabilize the economy.

Egypt has a more aggressive approach to managing its currency. For one, it's a managed float i.e. the Egyptian Central Bank permits their currency to move within a specific band. In situations of FX scarcity, of course this leads to significant challenges to access FX. Moreover, there are surrender requirements for exporters. For instance, Agricultural exporters in Egypt must surrender 70% of their FX proceeds to the Central Bank i.e. sell them at a pre-agreed price.

Summary of Capital Openness:

🇿🇦 South Africa is the most open but still has some exchange controls.

🇳🇬 Nigeria & 🇪🇬 Egypt manage FX policies strictly and restrict USD access during shortages.

🇰🇪 Kenya & 🇬🇭 Ghana are liberalized but intervene in FX markets when needed.

Urbanisation

Urbanisation is happening across Africa. Countries are approaching the 50% urbanisation mark driven by two factors. More people are moving towards urban centres and formerly rural towns are becoming urban in their own right. The stats show that Urbanisation in the continent has shifted from 31% in 1990 to 54% in 2020. Moreover, the number of cities has grown from 3,290 to 8,999. Across the continent, secondary cities like Kumasi, Warri, Ibadan, Nakuru, Kisumu, Giza, Port Said and Mombasa are emerging as key engines of urbanisation and economic growth. The point around urbanisation particularly as it relates to Fintech formation is that once you move to the city, you lose ties to the social support systems that exist in the village. In the city, you have to manage your own risk and life as an economic participant in a larger trading environment. Through this, demand for both credit and insurance rise. The intersection of urbanisation and mobile phone penetration is demand for digital credit which is one of the trends that will shape Fintech markets over the next 10 years.

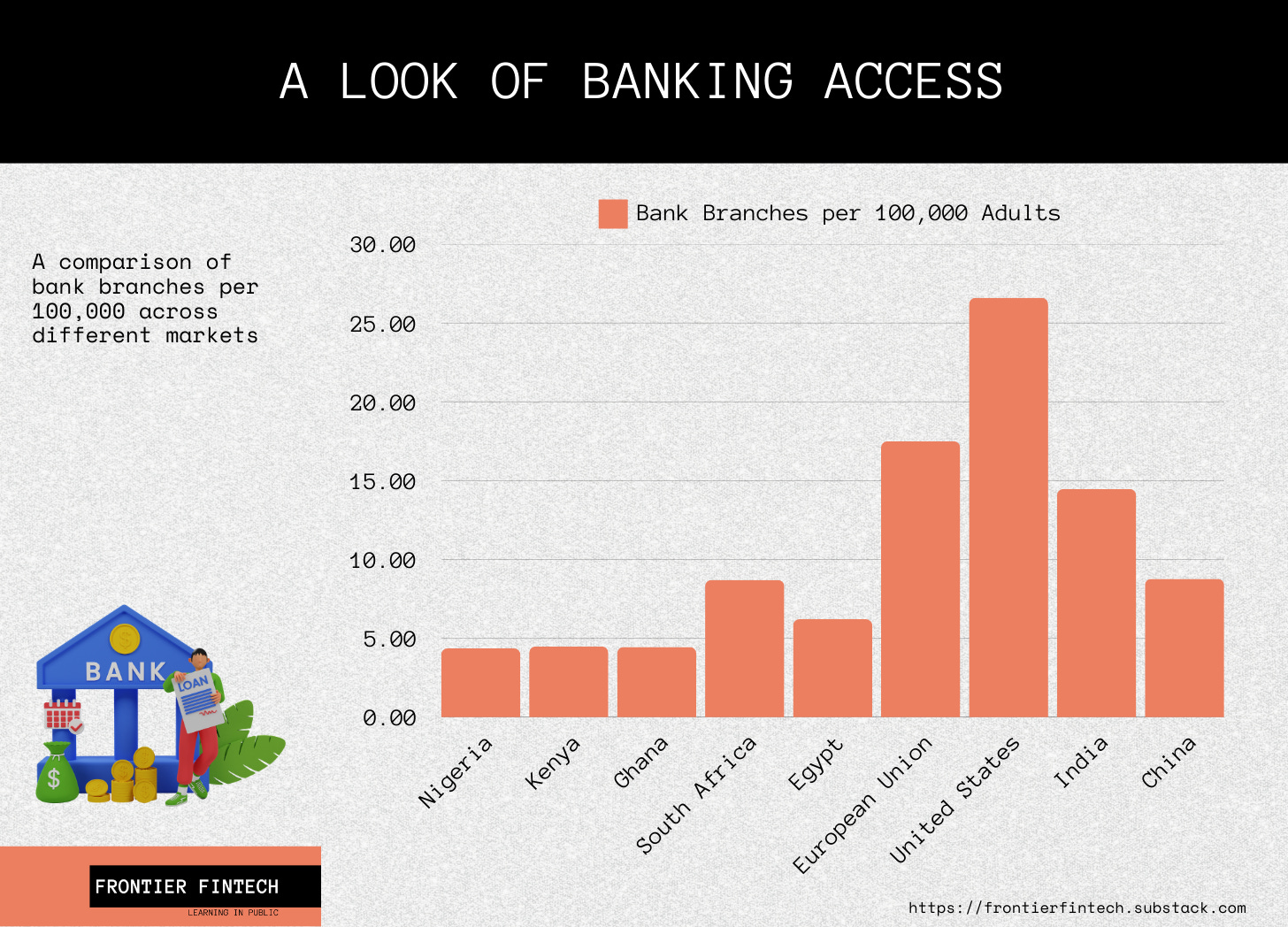

Depth of Traditional Banking Infrastructure

This is centred around both the breadth and depth of banking infrastructure in a country. With regard to breadth, the best way to look at this is to look at bank branches per 100,000 people. With regards to depth, the best metric for this is private sector credit as a percentage of GDP. In both metrics Africa lags but there are some differences within Africa that are worth mentioning.

Source: World Bank Data

Starting with breadth, South Africa and Egypt have relatively good access compared to Nigeria, Kenya and Ghana. South Africa has around 9 bank branches per 100,000 people compared to around 4.5 across Nigeria, Kenya and Ghana. Of course this can be compared to the US that has over 26 branches per 100,000 people. This just shows that it’s harder to include people in Africa using the banking system. This metric is always useful when you include GDP per capita and size of the country in your mental arithmetic. Given that countries like Nigeria are almost as big as large parts of Western Europe, then it's clear that it's almost impossible to cover large sections of the population using traditional approaches.

In addition to breadth, there are intra-continental differences in access to credit. South Africa for instance has an advanced credit market with private sector credit as a percentage of GDP standing at almost 100%. Nigeria and Ghana perform relatively poorly with both having 13% private sector credit to GDP. This shows that both markets have untapped potential for credit growth that the banking sector is structurally unable to meet in its current format.

Mobile Money Penetration

Mobile money penetration differs across the continent. It’s clear that different countries have taken different approaches to mobile money enablement with bank-led models in Egypt, South Africa and Nigeria and MoMo led models in Ghana and Kenya. Why this matters is because traditional banking cannot scale in Africa using the branch based model. This is not likely to change in the interim. Mobile Money is well placed to solve these problems given that it’s a service that is bundled with traditional telecom services. This reduces CAC making MoMo an attractive business for a telco.

The stats are clear across the continent as to how widespread MoMo is in various countries. The best place to look at this is in Flutterwave’s end of 2024 report.

Source: Flutterwave End of Year Report

The infographic below shows the most popular payment methods processed by Flutterwave in different countries. Whilst Egypt’s figures weren’t there, one can assume that they’d look a lot like South Africa’s figures, a mix of cards, bank transfers and a smidgen of mobile money. Nonetheless what this shows is that Ghana and Kenya have fully adopted MoMo whereas it’s not a popular method in Nigeria and South Africa. This means that there is an opportunity for players to come in and plug the access gap i.e. bridge the structural challenges in bank-led inclusion and the existing low levels of inclusion. It’s no wonder that both Nigeria and South Africa have seen the most Neobank adoption.

Country Rankings

Our goal is to determine which country has the biggest Fintech Opportunity. So the higher the ranking, the bigger the Fintech opportunity in that market. The rankings therefore need to make sense. For instance, a country that has a high urbanisation rate has a high baseline demand for digital financial services and therefore higher Fintech demand. Also, a country that has issues with its capital account has more challenges with making cross-border payments and therefore there is an opportunity for Fintechs to support cross-border payments. However, note that this is not a verdict on Fintech outcomes. In fact, a small Fintech opportunity means that that country has done a good job in expanding access and payment capabilities.

Now that we have evaluated some factors that matter for Fintech adoption in different countries, it’s important to build a framework to evaluate the different opportunities in the different markets. Before doing this, it’s critical to note that these factors work in a lollapalooza way i.e. they’re multiplicative in nature. Two factors when combined amplify their effects. To this extent, then when creating a composite score, you need to multiply the rankings rather than adding them.

Developing the Ranking

One can start by creating a ranking out of 10 for each factor. A higher rating would be given for how broken a specific factor is so that the country that receives the highest score is the country with the biggest Fintech opportunity. This will be counter-intuitive;

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.