#57 Building the Next Banking Giants - What Today’s Challenger Banks Can Learn from the Past

The playbook for how today's challenger banks can become industry giants, lessons from the rise of Capital One and Guaranty Trust Bank

Artwork by Mary Mogoi - Website

Hi all - This is the 57th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

Introduction

When we were building and selling Sote’s services, I remember meeting bankers, specifically the trade finance guys and walking them through our core proposition. Our pitch was that we’d allow a bank to follow its money as it moves across the world and through the supply chain. It was a very well crafted pitch aimed at telling the bankers that their inability to follow the money once it leaves their account was the biggest problem in trade finance. This is where cargo and money diversion would happen leading to losses in their trade finance book. With us, they could grow their trade finance books without the need for traditional collateral. More often than not, after repeating our well crafted pitch, we’d be met with keen interest but we’d always be asked; “So you’re like a collateral manager?”.Collateral managers take custody of goods in a warehouse on behalf of a bank, securing the bank’s right to those goods which are acting as collateral for a transaction. It’s often used for commodity transactions such as oil and sugar.

Initially, this was frustrating us because we didn’t want to be a collateral manager. We thought that the economics of collateral management were bad and that in the long-term, the market would value a collateral manager less than it would value what we were trying to build.

Nonetheless the collateral management references stuck and we learned to lean in on it. We’d say “yes, we’re a collateral manager” and then go on to specify how we differentiate ourselves. This differentiation actually got more people interested because they saw the value in collateral management as well as our additional services. It was a good lesson in business.

Ultimately, there are very few new things in business. Most business models have been done before and there’s very little new stuff that can happen. Google’s ad business was still a media selling business but its differentiation was game changing. A small payments business will grow up to look like a large payments business and its economics will mirror those of incumbents. It’s with this framework i.e. that there are not many new business models out there, rather there are enhancements to business models, that we should look at neobanks. In fact, using this lens we should even stop calling them neobanks and call them challenger banks.

Every new challenger bank being built should eventually become a large bank. This has been proven in the recent BBC survey that showed how Revolut has been named in more fraud complaints than any other large bank or e-money services firm. Ultimately, the industry is looking at Revolut like a bank and saying that your fraud detection is not as good as other banks. Challenger banks will grow to be like banks and therefore what should matter to us is; how do challenger banks disrupt incumbents and what does their growth journey look like? How can a challenger bank use its initial wedge and take its place amongst the large banks in the market? This framing led me to write this week’s article where I look at Capital One and GT Bank’s growth stories and take out key learnings that should feed into challenger banks. Tosin of Moniepoint rightly stated in an episode of The Flip Africa that “Fintechs will look like banks and banks will look like Fintechs”. He’s right.

This week, we’ll cover;

Capital One’s growth story;

GT Bank’s growth story;

Shared lessons from Capital One, GT Bank and other challenger banks from the last generation;

How the current crop of challenger banks can replicate the success of the last generation;

Capital One

The story of Capital One begins with the stories of Richard Fairbank and Nigel Morris. After completing their MBAs, Fairbank from Stanford (Finishing top of his class) and Morris from the London Business school, the two went to work in consultancy. They met at Strategic Planning Associates (SPA) which later became Mercer Consulting. Fairbank and Morris were both really smart people, Fairbank came from a heritage of scientists with both his parents being physicists. Morris on the other hand was known to be an empiricist, believing strongly that everything needs to make sense. Growing up, Morris wanted to be a psychologist and was on a constant reading diet of Carl Jung and Sigmund Freud. Through this he increasingly came to the conclusion that everything psychologists said was made up. He became in his words “a raving empiricist… If I couldn’t measure it, it didn’t exist”. This combination of empiricism and erudition led the two men to realise that the way credit cards were managed was a complete mess. The two of them through their work at SPA did a lot of consultancy for banks and the lack of data science in the management of credit cards was appalling to them. In fact according to Joy Morgan in her book “Capital One - The Untold Story” she remarked that “At the time every single solitary customer of every credit card issuer had the same annual percentage rate; 19.8%, plus a 20$ fee, Not only that but half of Americans couldn’t even get a credit card. Fairbank referred to that as a classic example of a one-size fits all approach.”

The insight that Fairbank and Morris had was that through data science, they could create a deeper personalisation of credit cards by offering the right product to the right person at the right price. Simply, instead of having a standard price for everyone and moreover ignoring half the market, the two of them could better price risk and create a personalised credit card for everyone. Armed with this insight, they built the first version of what later came to be known as the “Information Based Strategy” and went selling to banks. They needed a sponsor bank that would adopt their approach of personalising credit card offers. As is always the case, almost everyone rejected them apart from Signet Bank. Signet Bank was based in Richmond Virginia and was a notable player in the credit card industry, in fact it was one of the oldest continually operating bank card issuers in the U.S., having commenced operations in 1953. In 1988, the two men reached an agreement with Signet to start their credit card operation and that the two were to join as executives in Signet as opposed to it being a side project. With this agreement in place, they were off to the races though it was not a smooth start. Richard Fairbanks remembering a board meeting in the earlier years had this to say;

“I’m not sure Signet was in possession of all of their faculties when they hired two folks who were so inexperienced. I remember a senior management meeting in 1991.I was presenting to the top management of Signet and one of their executives and a good friend of mine said. “Rich, you are one of the most eloquent people I know. And I’ve been watching your eloquence for four years, but I can’t find one dime of that eloquence in our P& L. I think we are just about out of patience. And I tried to explain to him that everything was in place, tests were in the incubator, you know. It would be a tragedy to stop the program now just when we really had put everything in place. And unbeknownst to us was that a few weeks before the results came out for the product that really transformed. Capital One, and ultimately the credit card industry, which was the low rate balance transfer product”

Richard Fairbank

The low-rate balance transfer product was the pinnacle of the two men’s work thus far. In essence, they pioneered a product that would enable someone to transfer their credit card balance to Signet at a lower rate. This was a big selling point as clients could refinance their credit cards and benefit from lower, more personalised rates. It worked, over the next three years, the Signet card operation grew from their one million customers to a stunning five million customers. Furthermore, Signet’s managed loans went from $ 1 billion to an impressive $ 7 billion. The management of Signet had the foresight to realise that this new credit card operation would be more valuable as a standalone business and therefore the decision was taken to spin it off with a listing in 1994. Writing in the 1996 Annual Report, Richard Fairbank commented that;

“Capital One began with a strategic vision: clear, dynamic, inexorable. We saw that the technology and information revolution had transformed the credit card business into an information business. One that is extraordinarily data-rich, allowing the capture of information on every customer interaction and transaction. With this information, we can conduct scientific tests; build actuarially-based models of consumer behaviour; and tailor products, pricing, credit lines and account management to meet the individual needs and wants of each customer. By exploiting this insight, we have transformed the one-size-fits-all credit card industry and created one of the fastest growing companies in America. Because our strategy is information-based, not product-based, we are in an excellent position to ride the macro trend of the information revolution and apply our strategy to other industries as they too are reshaped by information.”

By the end of 1996, Capital One had achieved phenomenal growth. They had broken barriers on multiple levels. The company boasted 11.7 million customers and claimed $ 14.2 billion in outstanding loans. In 1997, Capital One experienced its third consecutive year of twenty percent earnings growth. In addition, net income rose to $ 155.3 million on revenues of $ 2.1 billion. The bank continued to grow driven by better data and more experimentation. At a point, according to Oracle Corporation they had the largest database and were conducting over 28,000 experiments in 1998.

Capital One grew organically and through acquisitions. They acquired Hibernia National Bank in 2005 expanding into the regional banking markets in Louisiana and Texas. This was followed by North Fork Banking Corporation in 2006, Chevy Chase Bank in 2008, HSBC’s U.S. card business, which made it the third-largest card lender in the U.S. after JPMorgan and Bank of America and ING Direct USA in 2012. Capital One also expanded to auto loans and mortgages to diversify from what was a cyclical credit card business.

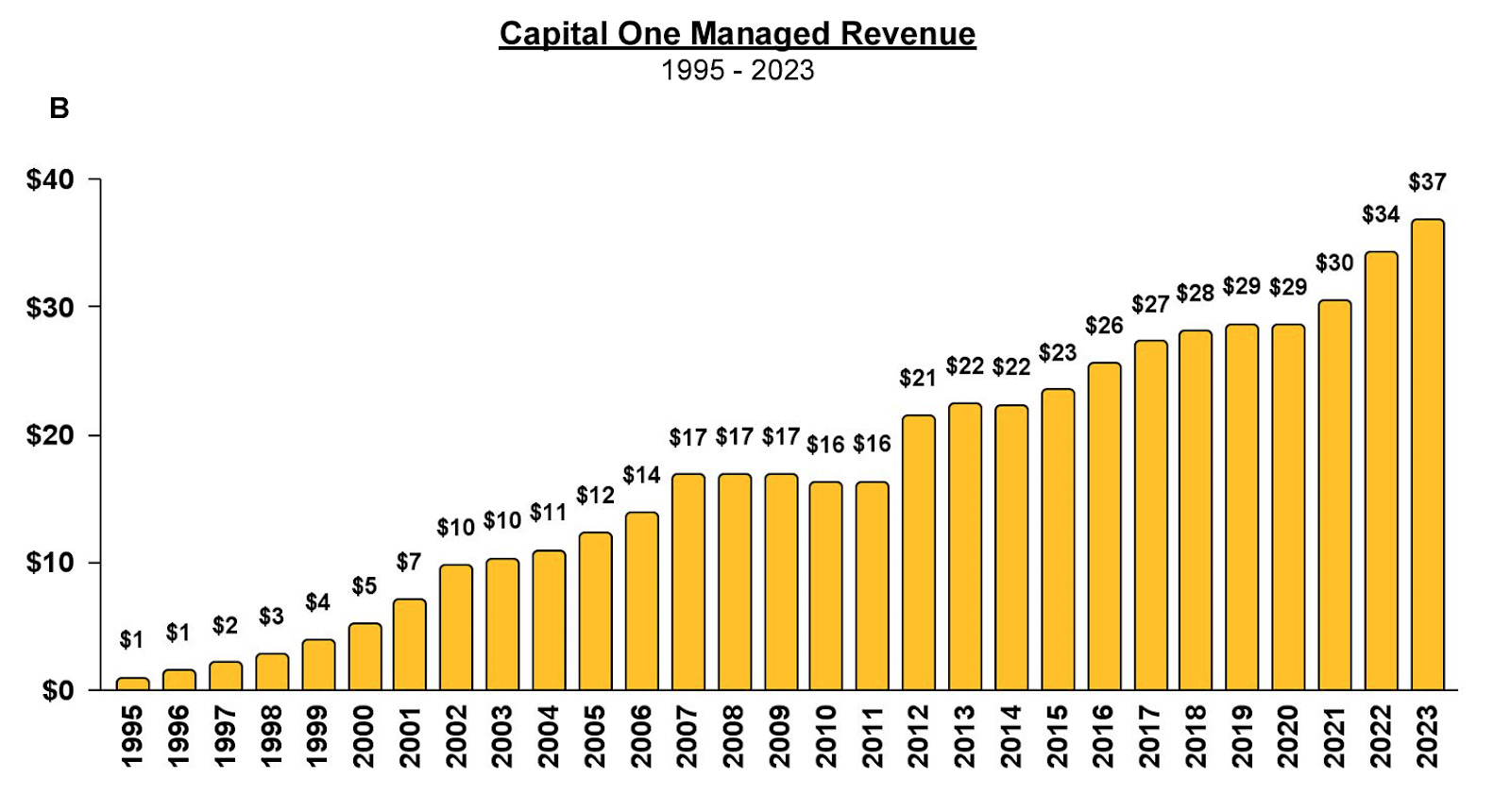

The graph below shows how they’ve managed to grow revenue over the years. Capital one is now the 9th largest bank in the USA with a balance sheet in excess of US$ 400 billion.

Writing in their 2023 Annual Report, Rich Fairbanks said; “We have spent a decade building a full-service, digital first national retail bank that is unique in financial services. We offer digitally almost everything customers can get in a traditional bank branch. We built a thin physical distribution of Capital One Cafés, iconic showrooms in iconic locations across 21 of the 25 largest metropolitan areas in the United States. Our digital first business model supports unrivalled pricing for checking accounts: no fees, no minimums, no overdraft fees, and some of the nation’s best savings rates. Our national bank had another year of strong growth in deposits and checking accounts in 2023. Two decades ago we weren’t even a retail bank. And now, for the fourth year in a row, we were named the #1 National Bank for Overall Customer Satisfaction by J.D. Power.”

Interesting Takeouts

Despite their aggressive growth, Capital One had an intense focus on risk, the image below is from their Annual Report in 1996;

Capital One were the first bank to hire a Chief Data Officer back in 2002;

Capital One was the first bank to shift their entire database to cloud, they started the process in 2015 and had migrated everything by 2020;

Capital One had an extreme focus on talent. Rich Fairbanks and Nigel Morris were known to run a very intense recruitment process and went heavy on stock based compensation. According to an article in American Banker in 1998, ”In addition to an employee’s regular salary in those early years, they (the associates) received the majority of their compensation in stock options. This brilliant technique gave employees real ownership in the company and an incentive for high achievement.

Capital One made early forays into AI using their vast database to inform areas such as fraud prevention, credit risk analysis, pricing, AI voice assistants and customer service;

Capital One has generated good returns for its investors returning a 2,660% return since 1995;

GT Bank

Understanding the history of GT bank requires an understanding of the Nigerian political economy of the late 80s. The former CEO and Founder of Access Bank Aig Imokhuede does a great job of this in his book “Leaving the Tarmac”. Like most African countries, Nigeria was in the midst of a less than democratic government coupled with structural adjustment programmes instituted by the IMF. This led to the common cocktail of liberalisation and corruption teaming up to shape the banking industry of the time. This was common everywhere and not just Nigeria. Aig states;

Around 1988, when I started my banking career, the military government led by General Ibrahim Babangida had commenced the issuance of new banking licences as part of its economic liberalisation programme, ostensibly to support the country’s economic growth and development. You needed a minimum capital of three million naira, (US $ 600,000), for a merchant banking licence and six million naira (US $ 1.2 million) for a commercial banking licence. Most investors applied for merchant banking licences, believing that the ‘Big Four’ commercial banks were just too enormous to compete against. It was also much easier to raise three million than six million….There was a general perception amongst the Nigerian public that a large proportion of the many banks then operating in the market were backed by wealthy individuals, known generally as ‘Ogas’ or ‘Godfathers’. In Europe or America the term ‘godfather’ would suggest senior figures in a criminal organisation, but in Nigeria it is closer to the original religious role of someone who provides support and protection to another of lesser standing. In Nigeria the ‘Godfather’ is like the traditional feudal barons of Europe, men of wealth and influence who extend their patronage to protect and assist others. Many of these godfathers would have amassed both their fortunes and their networks of contacts while serving in senior positions in the army and the government, or as contractors to the government. Having grown wealthy through their influence they would then use their banks to consolidate their positions within society. There was generally believed to be a godfather behind every bank and there was also a perception that without such a person it was not possible to even start, let alone build such a business. Inevitably, as political and military reputations waxed and waned, the fortunes of their various banks would follow suit.

This combination of free-wheeling licensing and the “Oga Culture” had the additional context that regulators were not set up to manage the increased number of poorly run banks. Naturally, what followed was small, poorly run and poorly capitalised banks that existed to serve the commercial interests of their well-connected backers. Again, this is not a Nigerian story, it’s an African story. The state of customer service in banks was best captured by Joke Giwa, a branch manager and early employee at GT Bank;

“What you need to understand is that at that time, it could take four to six hours just to cash a cheque at a branch. It was a manual process that had to be passed by seven different people. At each stage of the process, the cheque would enter a queue to be processed and you needed to be there. The whole process was characterised by a lack of trust between the bank and the customer; the tellers were behind cages and the branches were not desirable places to be. If you were lucky, a kind teller would give you an indication of where your cheque was in the queue and how long until the next stage so you could go out of the bank and do some errands, grab lunch…”

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.