#21: A rethink of Banking as a Service - the case of Vodeno

A Q&A with the team at Vodeno on their approach to technology and banking

Hi all - This is the 21st edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. 🚀

First a disclaimer - this is not a sponsored post and there was no commercial interaction between Frontier Fintech and Vodeno.

This week I had the privilege of interacting with the team at Vodeno, a company I have featured before in my Core Banking Platform article and a real innovator in the European fintech space. Vodeno is a digital core banking platform company that is backed by Warbug Pincus. Together with Aion Bank, similarly backed by Warbug Pincus, they have teamed up to build one of the most comprehensive BaaS propositions in Europe. Warburg Pincus is a storied Private Equity firm with an over 50 year heritage. Some of the companies it has backed globally include Airtel Africa, Ant Group, Gojek, Varo and Trax.

Aion Bank is a fully serviced digital bank based in Belgium, it traces its heritage to the acquisition of Montei dei Paschi di Siena’a Belgian operations by Warburg Pincus in mid 2019. The acquisition was part of a long-term digital strategy that would see a full modernisation of the bank. Part of this included a core banking transformation that was executed within 5 months and saw the bank shifting to the Vodeno Cloud Platform (VCP). Aion as a fully licensed bank by the European Central Bank and can offer banking service across all EU member states. Here is a very useful breakdown of Aion Bank’s business model and approach to the market.

Recently, Vodeno and Aion Bank formed a 10 year strategic partnership with Bankable, a leading BaaS provider to solidify their BaaS Proposition. The target is to provide the most functionally rich BaaS experience in Europe to banks and non-banks.

In this week’s post, I want to understand Vodeno’s approach to technology and banking particularly as regards to their positioning within the European Baas Space.

The Banking as a Service Model

In a recent post, I did a deep dive on Banking as a Service where I discussed the global trends that were driving BaaS. In essence, BaaS is an API driven business model where banks offer up their capabilities as a service to their partners. Their partners in this case could be other banks or fintechs as well as brands who want to embed financial services onto their platform. Shopify is the perfect example where through a partnership with Stripe, they enable Shopify merchants to hold balances, make payments and issue cards. The idea is that financial services should be designed based on consumer journeys and be embedded at the most suitable part of the journey. The diagram below from 11:FS’s fantastic BaaS report perfectly summarises this.

Source: 11:FS

Consumer journeys can include the purchase of a car, ecosystem services such as gaming and app stores, buying a house as well as starting and running a business both online and offline. Financial products such as loans, cards, store of value accounts, foreign exchange as well as insurance can then be embedded at the point where they are most useful. For instance, a customer buying a car on Carvana can get a car loan, car insurance as well as execute the payment all within the Carvana website. In this instance, those services have been embedded into the customer journey.

To make BaaS work, deeper capabilities are required such as KYC and AML, credit scoring, payments processing as well as reporting and compliance. The role of API’s in the modern economy is largely to drive efficiency and better customer propositions by allowing firms to focus on where they add the most value. In the case of BaaS, the idea is that banks have deep expertise in regulatory compliance, payment networks as well as KYC. By combining the technical expertise and customer focus on fintechs and non-financial brands with the regulatory compliance of banks, better customer propositions can be built.

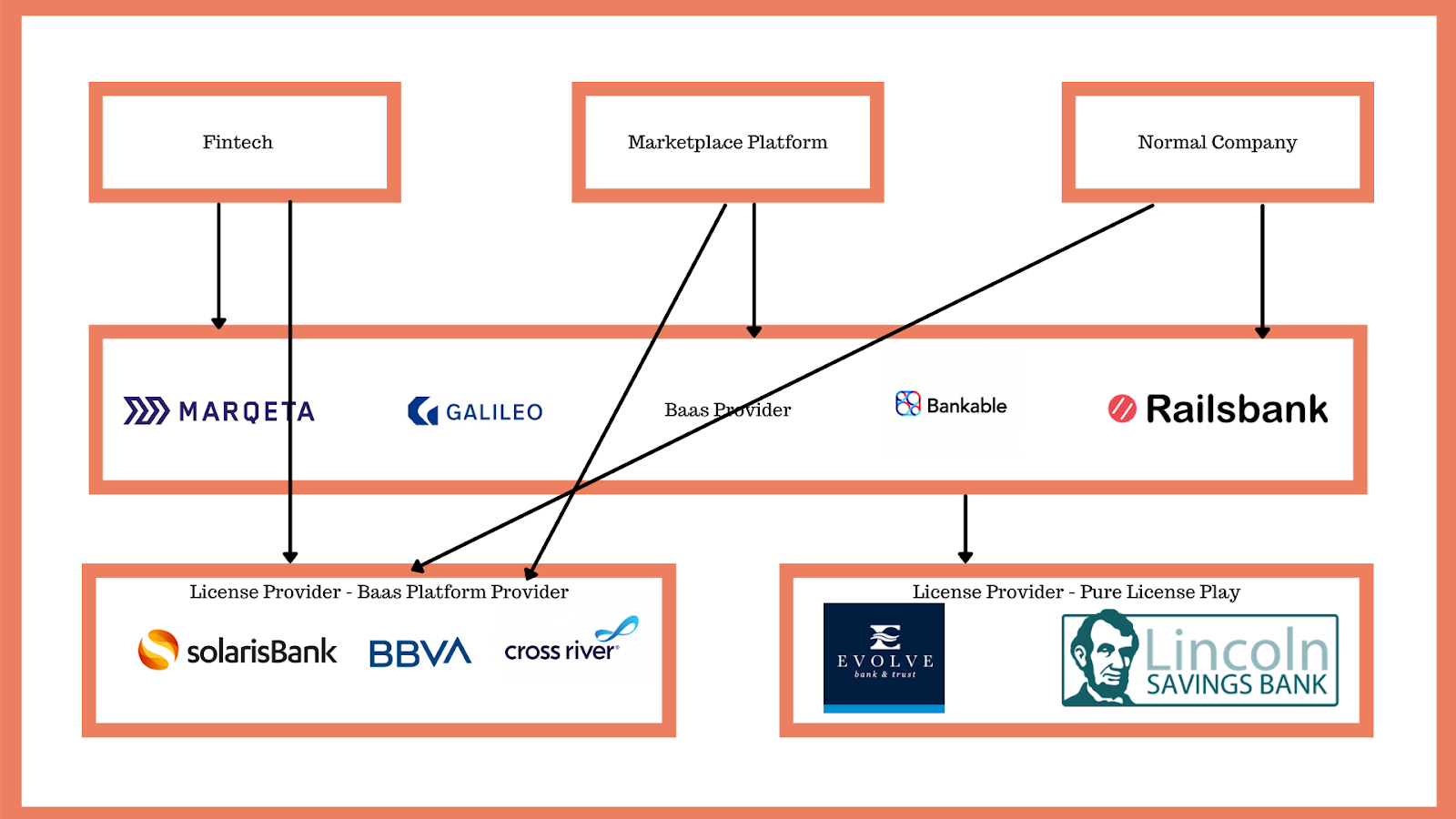

There are three types of BaaS providers;

Pure API Plays - Here, players such as Marqeta, Railsbank and Bankable act as an API bridge between banks and fintechs. The pure API play has utility-like economics with revenue fueled by API fees as well as interchange. American firms such as Marqeta have an advantage over their European counterparts largely due to the Durbin Amendment and their ability to charge higher interchange fees. Marqeta made US$ 290 million in 2020 with over 70% of its revenues coming from Square;

Hybrid BaaS providers - Here some banks such as Cross River in the USA as well as SolarisBank in Germany offer both the banking license as well as the APIs enabling a more comprehensive BaaS proposition. The economic model here is two-fold, on one hand you have a balance sheet play where you raise deposits and originate loans on your balance sheet on behalf of your brand partners. On the other hand you can also ride on interchange fees, payment commissions and API fees.

Pure License plays - banks like Sutton and Lincoln Financial in the USA have a pure license offering where they partner with BaaS API plays like Marqeta. This is largely a liability play;

The diagram below summarises the different models.

Nonetheless, some issues arise within the BaaS space particularly when it comes to execution;

Some of the License banks still operate legacy cores weakening their API capabilities;

Having multiple partners to integrate to as a Fintech or non-bank slows down time to market whilst increasing operational complexity. To launch a service, a Fintech needs to integrate to different partners for Payments, lending, cards etc;

Different services in different markets, if you want to launch a service in multiple markets, you have to sign multiple BaaS agreements;

Vodeno and the Value Proposition;

Anyone looking to launch a financial service therefore has a number of things to consider;

Type and structure of core banking platform;

BaaS provider;

PaaS and IaaS provider;

Licensing and compliance;

Amongst a number of other considerations. This is where Vodeno comes in, according to Tom Bentley the Chief Commercial Officer “... the main difference is that different players emerge for specific parts of the banking ecosystem for both fintechs and brands. Vodeno is fully focused on banking as a service… We’ve gone and partnered with different partners, offering one contract, a holistic solution with one SLA”.

Vodeno has partnered with best in class providers such as Mastercard for issuing, Form3 for payments as well as readID and Bottomline for digital ID and onboarding. Given that there’s a long-term partnership with Aion Bank, Vodeno can then offer the full stack leaving a Fintech or brand to focus solely on servicing their customers.

Other core providers focus solely on the core banking platform and provide APIs for connecting to different services. This is then a re-think of how core banking players operate and serve their customers. Tom states that Big banks have been very positive given that “banks want true banking as a service capabilities that let them launch services quickly with components already pre-integrated’.

In essence, some of the core issues around BaaS execution such as unreliable APIs from banks, legacy core platforms and multiple partners to connect to are solved by Vodeno and Aion Bank’s approach.

The Q&A

The team at Vodeno were kind enough to do a Q&A with Frontier Fintech to better elucidate their plans, ideas and long-term strategy.

1. What is the founding story of Vodeno, who are the founders and why did they decide to found this company and when - Vodeno was founded in 2018 by Mirosław Forystek, former CIO at ING, and Wojciech Sobieraj, who founded and served as CEO at Alior Bank in Poland, with the backing of one of the world’’s largest private equity firms in the world, Warburg Pincus LLC. The concept behind the creation of the company was to build a financial services technology company that was ‘born in the cloud’ with no legacy principles. Working with an ecosystem of 80+ partners, including global players Google and Mastercard, the intention was to remove friction in the delivery of digital transformation for banks and to enable embedded finance for non-regulated entities (e-commerce brands, SMEs, etc.).. Since our inception, we now have 12 customers and are scaling fast across Europe.

2. You're a cloud native core banking platform - why is this the right time to be purely cloud native and what advantages do you see accruing to cloud native players like yourselves vis-a-vis the traditional players such as Temenos and Oracle? - The Vodeno Cloud Platform (VCP) operates entirely in the cloud. The fundamental difference with a ‘no legacy’ principle is that we are using the latest development frameworks from the start and do not need to manage previous migration journeys that traditional software houses have to consider. Utilising VCP solutions like smart contracts and real-time data, we are able to build any financial product without the traditional cost burden that is associated with the development of code. This also means we can provide not only real-time insights to our customers but also to all of the down-stream systems, i.e. regulatory reporting outputs, through our ‘curated’ ecosystem of partners. This provides a true account of any customer or business line at any given time. We have one of the best engineering teams in the industry with a mix of talent from both the banking community and best of breed technology players.

3. Why did you choose to partner with Google and not AWS like most of your competitors are? Is there any technical or commercial advantage? - We need to adapt at speed to stay ahead of our competitors, while at the same time satisfying a constantly evolving set of banking regulations. To do that, we chose to build our platform on Google Cloud with microservices architecture and a CI/CD pipeline to create a robust, adaptable and customizable platform. This also enabled it to build in scalability for forecasted exponential growth in customer digital interaction and data lake services such as batch processing, speed processing, analytics and reporting. We are able to offer ‘active active’ deployments across Google’s multi-regional reach, and they have been a fantastic partner from the inception of the company.

Note: Here’s a deeper breakdown on the Google Cloud platform website.

4. Some of your competitors like Mambu have decided to develop a much thinner offering largely because it's more efficient to manage the code base with a thinner offering, there's less demand for customisations. It's my understanding that Vodeno is a much more comprehensive offering - how will you handle the additional complexity whilst scaling your clientele and offering a cloud only service? The core banking industry features a wide variety of choices, and each player has a different view on how transformation should be deployed. When Vodeno was built, we started with our blueprint to run enterprise-grade scaled banking systems, not just for the core, but for the full landscape you need in order to truly run a regulated banking operation. While some banks may choose to run just a headless core or replace a particular component — which we absolutely support through our microservice driven architecture — we believe in order to understand the ‘true cost’ of a customer, you need to consider the whole process from onboarding all the way to the regulatory reporting and controls you need to meet the appropriate demands of the regulator. Therefore, with our first customer - Aion Bank in Belgium - we took every component of the system from the technology to the contractual and operational efficiencies to consider the full process from start to finish. We curated the best fintechs in the market, including Tink, Form3 and BottomLine out of the 80+ VCP partners integrated in the platform to bring the full banking proposition together under a single contract. I would argue we simplify the complexity you mention as we have a singular service that is already proven in the market for the last 12 months. Other customers would need to procure, implement and operationally manage these partnerships alongside existing vendors. For clients who want a modern digital experience combined with a singular service that considers the full banking platform from start to finish, we believe we have the strongest and most unique proposition in the market.

5. The recent announcement of a 10 year partnership with Aion Bank and Bankable looks very interesting. What was the rationale of this move and how do you see it evolving over the next five years from a commercial perspective. What I mean is that, what are the revenue lines you're targeting and what factors will drive these revenue lines from a macro market perspective? - Bankable is an established player in the Banking as a Service industry and has a great ecosystem of clients across Europe. Alongside Bankable’s own tech stack, they will be leveraging both the Vodeno platform and our relationship with Aion Bank to set up pan-European, pre-approved account and card programmes to accelerate the time-to-market for banks, global brands and fintechs. Bankable will also be launching a new ‘Credit-as-a-Service’ offering through our partnership. This was only possible through our relationship with Aion Bank. With Aion’s European banking license, we are able to service non regulated entities. We believe more fintechs and banks will partner to form alliances to enable comprehensive solutions to the wider marketplace.

6. Does Vodeno have global ambitions or are you focusing on Europe mostly? If the former, are you looking at forming similar partnerships across the world? Do you believe that this is the natural evolution for core banking platforms? Europe is the focus with our capabilities already proven in the market. However, the global ambition is definitely there, and we are giving particular focus on geographies such as South East Asia, Australia and MEA. We already partner with service delivery institutions such as GFT to explore mutual opportunities, and through our investors, we are exploring how we can bring our unique services to a wider audience.

7. Could you give some details about Vodeno in terms of number of staff, percentage in engineering, total amount funded, number of existing clientele, number of offices and planned expansion? We have an amazing international team of more than 200 people, with around 65% of the team solely focused on engineering and product development. We currently have four offices across Poland and Belgium, with additional teams in the UK, France, Netherlands and Germany. We have signed multiple customers spanning traditional banks and consumer brands, and we expect to continue to expand our team as we grow our client base.

8. Could you speak to the reliability of your system particularly API and cloud up-time as well as auto-healing capabilities? What factors within your design and architecture drive these outcomes? As a modern, cloud-native and microservice-based architecture that enables auto-scaling and auto-healing, we have had zero breaches or downtime on our system to date. We believe our SLA and the availability of our services is one of the best in the industry with a full contractual commitment to compliance and regulatory maintenance. Nearly all of the software providers mainly try to push back compliance onto their end customer, and we believe what differentiates us is being able to offer a transparent cost model with no hidden cost.

9. Lastly, a major issue with core banking transformations is the sheer complexity of managing the transformation. How does Vodeno approach working with legacy banks and making it easier for them to shift onto your modern platform? There are many different approaches and lessons learnt from the last few years. We see lots of discussion on progressive renovation and, in particular, greenfield deployments that start afresh. Banks can either replace their whole core,or they can pick and choose the modular components that will allow them to deliver a superior customer experience and deploy them at their own pace. While we can offer many different models, we believe the Aion Bank transformation is a great case study of a successful legacy bank migration. Within five months we were able to upgrade all of the legacy technology to the cloud and transform all of the manual processes into digital self-service applications. This also included the training of the staff and the set-up of the new operational model for Vodeno to provide the full platform ‘as a service’. Key to Aion’s digital transformation was modular components that were completely cloud-native and built using cutting edge technologies to precisely manage the complexity of the legacy migration. Additionally,set processes could easily be adopted ‘off the shelf’ through the back-to-back agreements we had already established with the 80+ fintechs in the wider VCP ecosystem. Therefore, under one SLA and one contract, we were able to create a comprehensive model that allowed Aion to quickly launch the full platform rather than considering just one component. Our implementation process is fully modular and can be tailored to each client’s needs. This is a game changing approach for financial service transformation.

Summing it all up;

Many factors add credence to the strategy that Vodeno has taken. These include;

The growing digitisation driven particularly by Covid-19;

The growth of MSME’s and gig workers driving demand for niche financial offerings;

Demand by existing incumbents to launch digital propositions;

Nonetheless, the business model doesn’t seem to have any significant barriers to entry. Replication of a similar offering where a core banking provider partners with a digitally focused bank can be executed. This is likely to drive price competition leading to reduced margins. All that said, the partnership is really useful for founders. Looking forward, one of the concerns I’ve harboured around Fintech has been the expense required to launch a service in terms of both cost and technical expertise. The Vodeno strategy is somewhat similar to what Stripe is doing by abstracting the complexity of launching a Fintech or embedded finance. It will be interesting to see how the space evolves over time. What is clear is that digital financial services are still at the foothills and I am confident that growth will continue being non-linear in the short-term favouring businesses such as Vodeno.

Another interesting development worth noting is the shift towards banks having digital propositions as their retail strategy whilst relying on BaaS as their wholesale, corporate strategy. All this nonetheless needs to be backed by an end to end rethink of their core platforms. It will be interesting to see how this BaaS strategy unfolds and particularly how existing players in the core banking space react.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@gmail.com;

Here's a link to the Vodeno website https://www.vodeno.com/