Breaking down Banking as a Service

Drivers and opportunity

What is BaaS

Banking as a Service or BaaS is a key concept within the Fintech space and has been for the last 3-4 years. BaaS is essentially where a bank offers some of its core capabilities as a service to third parties for a fee. These capabilities could be compliance, KYC, identity, payments, accounts or the balance sheet.

11:FS have an amazing report on BaaS and it’s a must read for anyone interested in the space. As usual my interest is always to understand the origins of a commercial trend within the Fintech space and understand how it could be applied in our markets i.e. Sub-Saharan Africa.

Origins

The origins of BaaS can be traced to the post-GFC western hemisphere. I keep repeating post GFC in my articles but it’s amazing how one event has had such an impact on modern-day Fintech. The financial crises gave impetus to entrepreneurs and innovators seeking to redesign finance to make it more convenient, user friendly, safer and more trustworthy for its users. Additionally, the increased regulatory pressure gave rise to the following core themes;

Banks shied away from lending to specific segments - predominantly retail and SME;

It became more difficult to get a bank charter across the Western World;

Regulatory complexity made the costs of compliance skyrocket;

The Dodd-Frank act introduced some new regulations such as the Durbin Amendment that capped interchange fees for banks with balance sheets greater than US$ 10 billion;

A good teardown of the drivers of BaaS can be found in the first half of this video by Andreesen-Horowitz partner Angela Strange;

The increased demand for novel financial services coupled with the difficulty and complexity of founding and running a bank essentially led to the conception of the BaaS business model. Fintechs realised that banks have developed some useful competencies in some areas such as compliance, payments, kyc and balance sheet management. Rather than taking on that headache, why not partner with them and use their competencies as a service.

To add to this, as Angela Strange notes in the video, technology has enabled finance to be embedded into the customers day to day life in the exact moment when finance is needed. The prediction being that every company will be a Fintech company. Embedded finance and the rise of open banking particularly in Europe have added impetus to the BaaS concept.

Breaking down BaaS

BaaS is driven by APIs, it is a completely API reliant business model. In BaaS, banks offer specific capabilities via APIs to their partners. An example is say Uber in Kenya wanting to drive value within its ecosystem by enabling both drivers and riders to maintain wallets. It could do this so as to reward highly rated drivers with bonuses or give highly rated customers discounts. It could also do this so as to enable direct lending to drivers in the form of overdrafts or insurance premium finance at a lower cost. Commercially, the cost of inter-wallet payments would be free to Uber thus improving the economics around payments.

To do this, it would have to partner with a bank through APIs. The core APIs needed would centre around the creation of an account/wallet, exchange of KYC data, initiation of loans and basic payments. The bank in this case would be offering its banking capabilities as a Service.

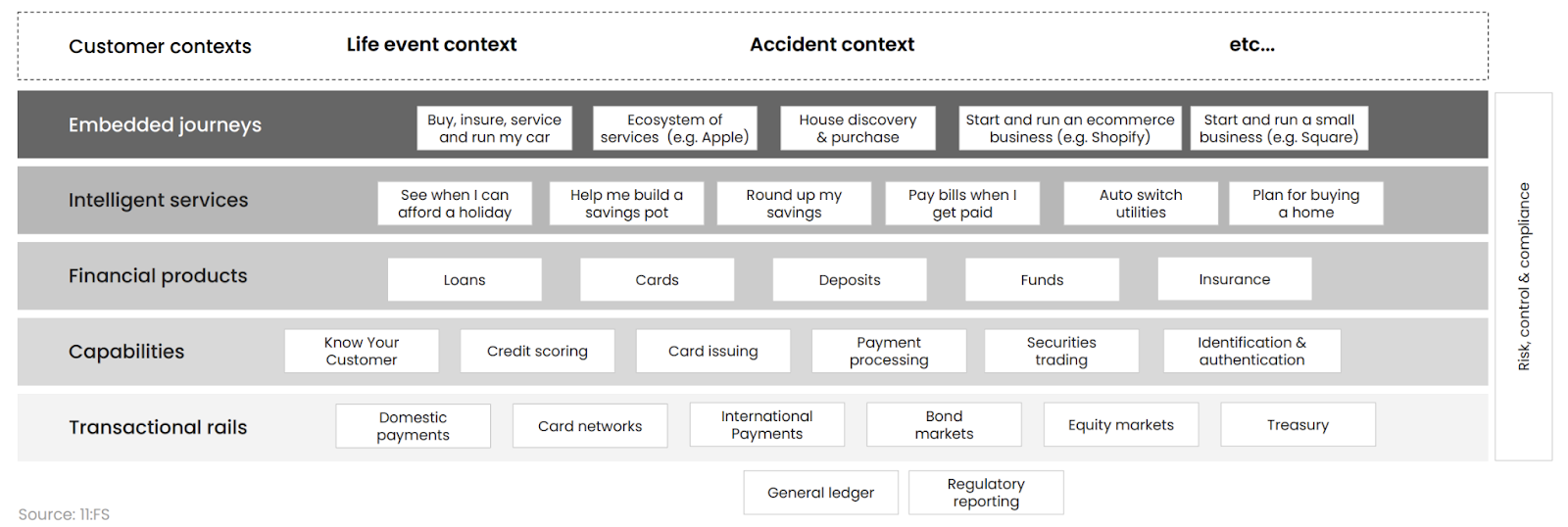

Source: 11:FS

11:FS have done a very useful job in defining the core elements of a BaaS offering. At the top is a brand in this case Uber, in the middle there’s a banking stack which is largely an API layer and at the bottom is an institution licensed to offer those banking services. The brand relies on the capabilities of its BaaS partner in areas such as Treasury, KYC, payments, operations and risk management. It focuses on driving value within its existing business through embedding relevant finance. Of course, this works well where brands have the following core characteristics;

A sizeable and growing user base;

High levels of DAU or daily active users in the case of Uber, both riders and drivers can be expected to use the app daily;

A history of financial transactions happening within the ecosystem;

High levels of trust from its customers;

Some examples are Amazon and Shopify who have all announced BaaS offerings. A classic example of BaaS before the term hit the big leagues is the M-Shwari offering by NCBA and Safaricom. NCBA enabled Safaricom to offer savings and lending capabilities to M-Pesa customers. Similar partnerships have been announced within the continent.

From the diagram above, the BaaS capabilities usually come in at the lower three levels i.e. financial products, specific capabilities and access to transactional rails such as local ACH, RTGS and instant payment systems. Brands often have the unique customer insights that are required to create a very powerful offering.

Different Elements of the BaaS stack;

Different markets have different implementations of BaaS as well as different underlying drivers for the BaaS model. In the USA for instance, the Durbin amendment and its implications on interchange fee have had an impact on how BaaS works as regards to what types of banks can offer BaaS profitably. In Europe, PSD2 and open banking have had an impact on the market structure there. BaaS is typically more profitable in the USA due to the high penetration of cards and the interchange fees that can be earned on cards.

Within BaaS offerings, there are typically three types of BaaS providers. Pure BaaS API providers, pure license providers and hybrid players who provide both the license and the APIs. The market can be broken down as follows;

Pure BaaS API Plays

Pure BaaS API providers focus on creating open APIs that link to a bank partner. They usually don’t have banking licenses and act as a bridge between banks and fintechs. Usually banks are running on legacy technology and don’t have the sophistication to offer world class and reliable APIs to Fintechs. Some of the key names within the pure API play are Marqeta and Galileo in the USA and Bankable and Railsbank in Europe.

The economic model here is largely utility like, a fact even mentioned by the founder of Railsbank Nigel Verdon. These companies provide simple and reliable APIs that enable Fintechs to prototype and launch their offerings. The returns are driven by API fees as well as other revenue lines such as interchange. It seems nonetheless that American BaaS providers are more lucrative. Marqeta for instance had reported revenues of US$ 300 million in 2019 and the CEO Jason Gardner mentioned that 2020 revenues were growing at a steeper rate. Marqeta raised US$ 150 million dollars in mid 2020 at a valuation of US$ 4.3 billion dollars.

Railsbank in 2019 reported revenues of US$ 3.5 million as at December 2019. The company recently raised US$ 37 million in Q4 2020 at an undisclosed valuation. At first blush it seems that the USA is more lucrative.

Hybrid BaaS providers

Hybrid BaaS Providers offer both the banking license as well as the APIs and integrate directly to Fintechs without the “middle man”. The economic model here is two-fold, on one hand you have a balance sheet play where you raise deposits and originate loans on your balance sheet on behalf of your brand partners. On the other hand you can also ride on interchange fees, payment commissions and API fees. Some of the main players in this sector are Solaris Bank in Germany and Cross River bank in the USA.

Cross River is the BaaS partner for Affirm where it originates loans for Affirm which it then securitises and sells to investors, often it retains 10% of the loan amount. Cross River actually didn’t start as a BaaS play, the founder Gilles Gade has a background in Wall Street and actually started the bank to take advantage of the fact that bigger banks were selling their assets so as to derisk their books and reduce their capital requirements. The bank has nonetheless evolved to offer a world class BaaS Platform.

Since 2015, Cross River has grown its revenue by a CAGR of 57% largely on the back of higher interest incomes. Commission revenues have only grown by a CAGR of 21%, lower than interest income which has grown at 69%.

The balance sheet has also grown although it had a significant spike in 2020 due to Paycheck Protection Program driven lending. It’s fintech first approach made it the natural partner for these loan disbursements. Of course, as an analyst one can point that PPP was a one-off but in business, one-offs can be your big break. Cross River executed 2020 perfectly and this drove validation of their BaaS model.

Goldman Sachs is also pursuing a hybrid strategy and has had some successes for instance their partnership with Stripe.

Pure License Providers;

Within the BaaS stack, we have pure license providers who just offer up their licenses to fintechs as well as some basic APIs. There’s nothing much to be said about these players other than they are typically small community banks who can enable fintechs to earn high interchange fees due to the Durbin amendment. The key revenue driver is a share of interchange, but largely it’s a liability play. Evolve Bank and Trust as well as Lincoln Savings Bank are some of the key players in the USA.

Some core considerations

When deciding which part of the stack you want to play in, I think the following are the key considerations;

A pure API play as well as a hybrid play requires significant tech talent. Tech talent can be costly and thus you have to ask yourself whether you can compete for the top tech talent in the current market;

Most BaaS plays both in Europe and the states are centred on cards - existing banks are wary of getting into that space due to the potential to cannibalise their own cards business. You have to also figure out whether cards are significant in your market. BaaS is not that big in Asia where mobile payments are dominant;

Different market dynamics are at play - for smaller community banks, they tend to have a stable balance sheet with a reliable clientele, the license provision is a clever liability play;

Revenue drivers - in some markets such as Africa, interchange may not be a big consideration. Nonetheless, interest rates and exchange rate revenue can play a part in your BaaS considerations in the continent;

Additionally, BaaS can be a significant long-term threat to big banks. The reality is driven by the following core factors;

AWS changed the dynamics of software and IT completely. In the past, large banks had an advantage over small banks due to their ability to expense significant sums on their IT capex and the resultant depreciation. Smaller banks simply couldn’t compete. Now with cloud computing and SaaS core banking platform models, smaller banks can offer an even better and more reliable product than their larger incumbents. Size is no longer a big advantage, in the cloud era, innovation and strategy will play a bigger role;

The API-fication of the world continues at pace and the banks that develop pure API plays could be the giants of the future. In the past, the banks that built their physical distribution the fastest won;

The two factors above are driving a tend towards partnerships in the provision of financial services. Before, banks focused on building a financial super-market model where there was ownership of different finance companies under a big bank brand name. This included an insurance brokerage, stock brokerage, investment banking and asset management. This model was largely hit and miss and now faces irrelevance in an era of APIs. The focus would just be to partner strategically with a partner who can deliver what you need - Cross River Bank’s partnership with Affirm being a prime example;

Is there a BaaS Opportunity in Africa?

Infrastructure often has a “build it and they’ll come” component to it. It’s difficult to answer this question because BaaS is barely built in the continent. Stripe for instance has enabled a number of businesses to emerge just on the back of enabling easier internet payments, Substack is a good example of a stripe-enabled business model.

There are very few if any BaaS propositions that are built specifically to provide Banking as a Service. Often, existing banks tend to offer their existing functionalities to Fintechs, but these often breakdown due to the following;

Unreliable APIs - most banks don’t have open APIs, what instead they do is to expose their existing internal APIs to third parties. This tends to result in a buggy experience for the Fintechs due to issues around reliability;

A number of banks still operate on older core banking platforms which really weren’t built for the demands of modern Fintech;

Those banks that do transform their core banking system often focus on ensuring business continuity - rarely is a transformation done with a view to shift strategy entirely;

Of course, tech talent is an issue. A number of local banks are really struggling to maintain their tech talent in the face of global competition for talent and increasing VC funding for African start-ups that’s luring all the tech talent away.

In my view, BaaS has huge potential in the continent. If you think of some of the larger trends taking place in the continent such as;

A very young and increasingly educated populace;

The prices of smartphones and data trending downwards;

Increased internet speeds, and;

Apps becoming the de-facto mode of distributing services;

It seems that all factors point towards the BaaS model being a game changer.

Global Baas Threats

Despite all the potential, there are some threats to BaaS globally. Some of the main ones in my view are;

Crypto and De-Fi, I see the current financial system running two separate experiments. On the one hand, Fintech seeks to digitise the existing financial system most times creating digital on-ramps to the existing rails. On the other hand, you have crypto and De-Fi which is truly digitally native. In the medium term, the two will co-exist and even be synergistic but in the longer-term, it seems that there’ll have to be one winner;

Regulation is always a threat. In the US for instance, if the Durbin amendment is repealed, existing BaaS models will face an existential threat. In Nigeria, we have witnessed a lot of regulatory activity that has affected Fintechs. In Africa you are just one circular away from total wipeout.

It will be interesting to watch how this space plays out. SoFi acquired Galileo in April 2020 so as to bolster its BaaS offering at a valuation of US$ 1.2 billion. This was even more validation of the BaaS business model. Banks within the continent need to think through having a long-term BaaS play.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@gmail.com;