Part 2 of Digital Transformation in Banks

Focus on Goldman Sachs and DBS

This week with feedback from some of you guys, I have introduced a summary infographic that captures the gist of the article. Frontier Fintech on the Go!

Last week we discussed the context in which banks in Africa are operating as regards Technology and the threat of Fintechs. The discussion was that banks in Africa are still relatively profitable and that existing business models can continue to produce results in the medium term. Nonetheless, demographic and technology challenges lurk. Additionally, there was a discussion about some of the organisational challenges banks are facing as regards recruitment, training and general incentive design when seen from the prism of modern tech companies.

This week, we take a look at Goldman Sachs and DBS Bank of Singapore who seem to have handled their digital transformation projects well. On each, a brief history, contextual discussion and insights into their strategic initiatives will be done.

Goldman Sachs

History

Goldman Sachs is a pillar of the modern financial system. Tracing its roots back to 1869 when a German Migrant Mr. Marcus Goldman moved to New York and opened an office in Manhattan. Mr. Goldman spotted an opportunity in the trading of promissory notes (think modern day commercial paper) - he would buy promissory notes from merchants in New York at a discount and sell them to larger institutions. At the time, bank credit was tight and this was an attractive mode of financing for merchants, with most of his clients being Jewellers and Tanners. In 1882, Samuel Sachs, Mr. Goldman’s son-in-law joined and they formed a partnership with the name Goldman Sachs & Co. Mr. Goldman was 48 years old when he started the firm and he was known for having a gift for numbers, being ambitious and harbouring an exceptional entrepreneurial spirit - a spirit that has formed the DNA of Goldman Sachs up to today.

Watch this for a great background of the firm.

The firm grew over 150 years largely by being an innovator in various forms of financing. For instance, Goldman Sachs ventured into Investment Banking in the late 19th century and helped General Cigar and Sears Roebuck raise funds. The key innovation was that Goldman valued the firms based on earnings power and intangible assets like brand and goodwill which at the time was unheard of. Firms were valued primarily by the value of their fixed assets given that most of them were Railroads financed by the venerable J.P. Morgan. This was very attractive to investors and raised the firm's stock amongst the investor class. Later blockbuster IPO’s included the Ford Motor Company. Interestingly at the time, Goldman Sachs disrupted the industry’s then incumbent investment bank JP Morgan. In the modern era, Goldman is having more success with its tech efforts as well.

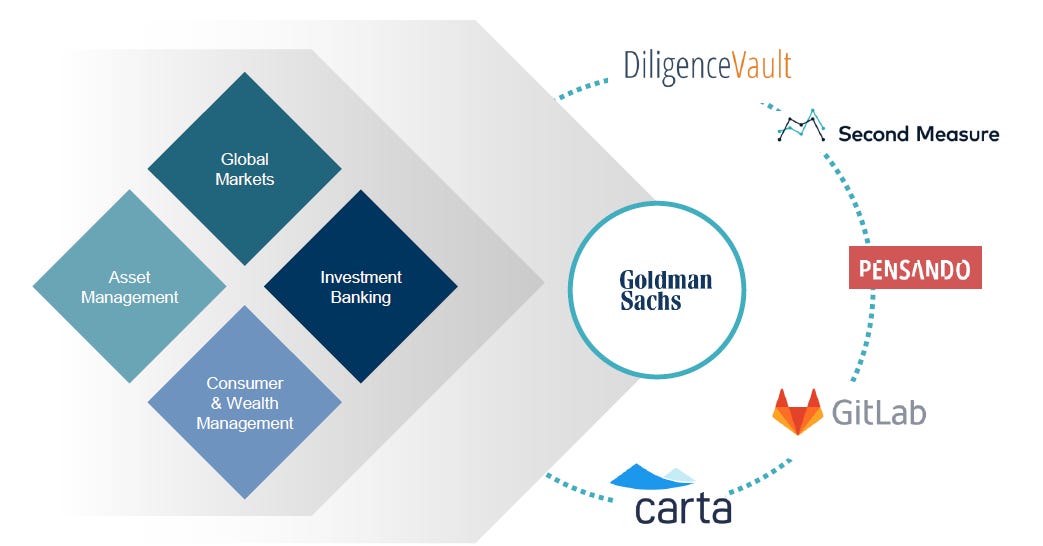

Goldman Sachs is now a powerful financial institution with a presence across the world. Goldman primarily operates in four key markets;

Global Markets - Primarily Fixed Income, Commodities and Currency (FICC);

Investment Banking;

Asset Management; &

Consumer and Wealth Management;

Strategic Context

Context is always key. Goldman’s digital efforts were driven by a few key themes;

The traditionally successful FICC business was significantly impacted by tighter regulations. Trading incomes peaked at US$ 23.9 billion in 2009 and were recently at US$ 11.5 million in FY 2020, having grown by over 53% from 2019.

The Investment Banking culture is known to be grueling and relentless with analysts working 100 hour weeks. Millennials are known to seek more work-life balance and this has made investment banks like Goldman less attractive to top talent;

The same challenges that applied to global banks and alluded to in Part 1 of this article also applied to Goldman;

Key Strategic Initiatives;

The main strategic push can be summed up in a comment the former chairman Mr. Lloyd Blankfein made in 2017 when he said “We are a technology company, we are a platform”. Goldman Sachs’s business has traditionally been split into two parts. A client facing investment banking and wealth management function and a back-end trading and execution function. Goldman then had to strategise around becoming a platform company whilst using technology to develop new business lines that were previously difficult to enter into.

The two main thrusts of its strategy could be summarised as;

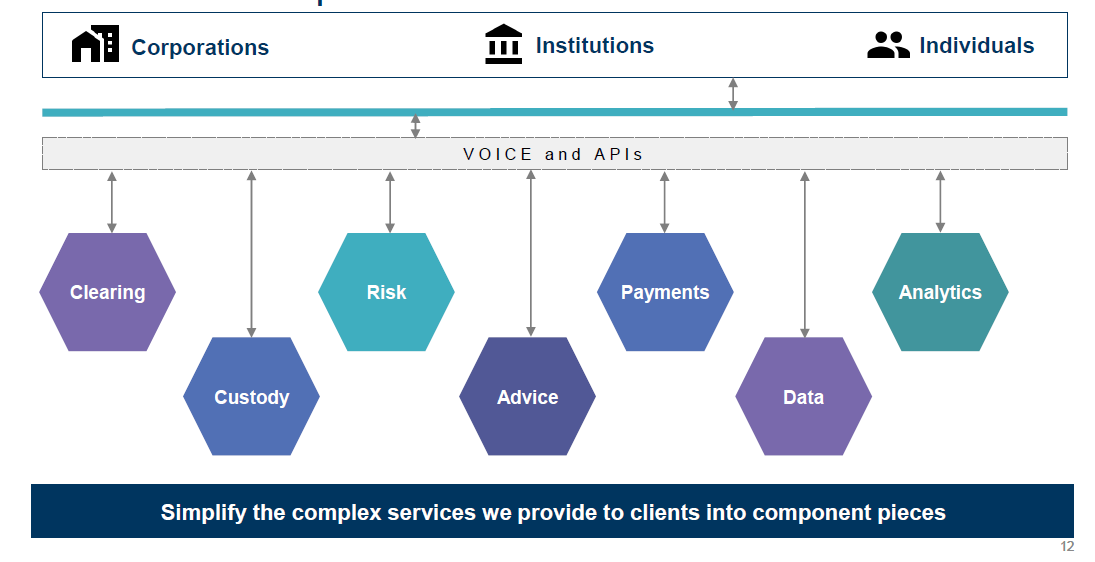

Re-platforming the existing business and driving productivity enhancements - this included having an API strategy to abstract the complexity of its offerings in trade and execution whilst building productivity tools for its client facing staff;

Launching a new proposition to diversify its business - Marcus and BaaS;

The replatforming effort included a new approach to technology. Traditionally, the bank built almost everything in house. As far back as 2013, Goldman had more people in its engineering and technology department than Facebook had in total headcount. Goldman then changed this approach by having a filter which enabled them to decide whether to build, buy, invest or partner. The key insight being that API’s enable you to compose best of breed apps together therefore building your own products doesn’t give you any distinct advantage.

Essentially, the firm enables its clients to raise capital, invest, trade and additionally create new business lines through partnerships. Applying the build, buy, partner and invest framework, the firm could then re-imagine how it would deploy those capabilities using best in class technology, either built in house or acquired.

Source: Goldman Sachs “A culture of innovation” presentation January 2020;

Goldman can then have best in-class capabilities around different elements such as due diligence, analytics and equities research and analysis.

Additionally, Goldman could enter into new markets such as consumer because it didn’t have a legacy consumer business. It therefore didn’t have any revenue lines to cannibalise nor legacy tech to deal with. The thinking was that modern technology enabled them to offer a fully digital consumer offering whereas in the past, they’d have to build out a branch network.

This video has a good discussion of the overall strategic thinking at the firm;

Main wins

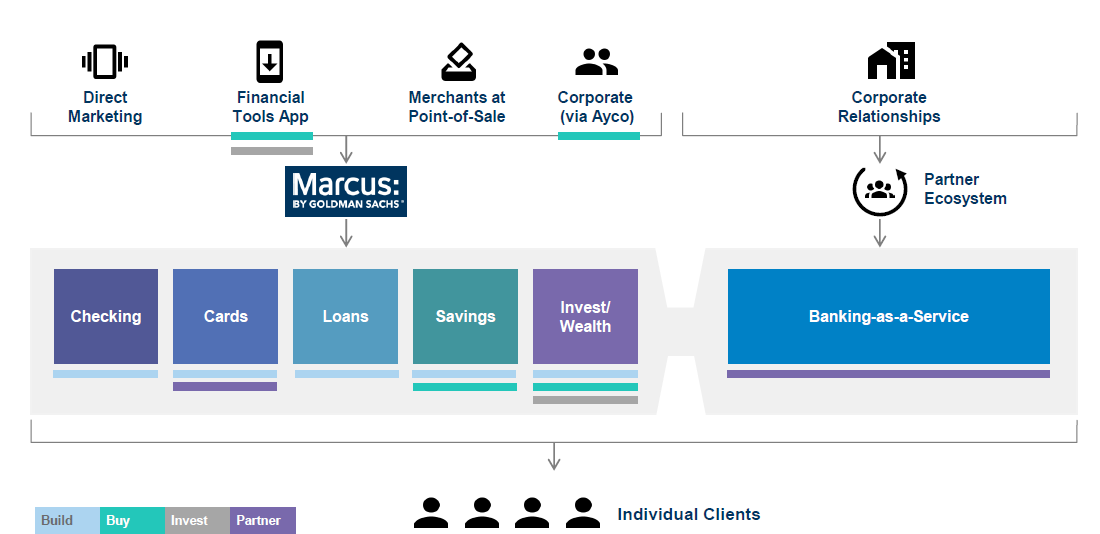

Marcus

Marcus named after the founder Marcus Goldman is the firm’s consumer banking and wealth proposition. An app based consumer product that offers;

Cards - in partnership with Apple;

A range of Exchange Traded Funds (ETF’s) and investment products from Goldman’s extensive product catalogue;

Soon a checkings account in partnership with Marqeta;

Watch this

and listen to this for a deeper insight into Marcus.

Marcus reflects perfectly the strategic thinking regarding how Goldman views technology. The focus is on where Goldman needs to invest its technology development efforts and where should it buy, partner or invest. Marcus is profitable, with revenues of US$ 1.2 billion in 2020 and a rating of 4.9 on the app-store. The graphic below shows how Marcus was built;

Source: Goldman Sachs “A culture of innovation” presentation January 2020;

Banking as a Service Proposition

Last year Goldman launched it’s BaaS proposition where it offers its capabilities via APIs to its clients globally. The BaaS proposition focuses largely on Transaction and Treasury capabilities and targets e-commerce platforms, fintechs and other players seeking to offer banking capabilities to their clients. One of the main wins with the BaaS proposition was the partnership with Stripe in which Goldman offers its capabilities to Stripe’s customers. Stripe Treasury offers via API, interest earning accounts, access to payment pipes such as ACH and card issuing capabilities. Goldman also has a partnership with Amazon to offer credit lines to retailers on the Amazon platform.

The two diagrams show the re-platforming efforts in principle. Moving from manual/voice and paper based interactions with their stakeholders to API driven communication whilst at the same time converting their stack from a monolithic offering to a more service oriented offering.

Source: Goldman Sachs “A culture of innovation” presentation January 2020;

Goldman’s Marquee Platform

Marquee is Goldman’s proprietary digital securities platform. Marquee offers access to trading and proprietary insights to Goldman’s customers as well as internal staff. Through a product called Zephyr offered on top of Marquee, Goldman’s bankers can walk through investment and financing scenarios with their clients without having to work insane hours on their decks.

Goldman’s client proposition has evolved with the addition of consumer banking, digital wealth, credit cards, BaaS and Transaction banking adding to the revenue mix. The consumer division enables Goldman to further reduce their capital costs, the CFO mentioned that each time the consumer division’s balance sheet grows by US$ 10 billion, the bank wide cost of capital reduces by US$ 80m.

DBS Bank Singapore

History

DBS Bank is one of the largest banks in Asia with a presence in most countries in SouthEast Asia. DBS Bank was started in 1968 to take over the role of the Economic Development Board (EDB) that was tasked with financing industry in the new economy that was Singapore. The bank was formed as a public company with investments from the Government of Singapore, other commercial banks, insurance companies and private investors.

It currently has presence in over 18 markets including India, Indonesia, Taiwan, Malaysia, China and Hong Kong and is a truly Pan-Asian entity. DBS is currently known for having executed one of the best bank transformation projects in the world. If you consider that it has roots in being a government ‘policy’ bank, this is even more remarkable. It offers the full suite of commercial banking services including;

Retail Banking;

Corporate and Investment Banking;

Treasury and Money Markets;

Trade services;

Strategic Context

Piyush Gupta joined DBS Bank in 2009 after a 27 year career at Citi. His vision was to create the “Asian Bank of Choice” using “Asian Relationships, Asian insights, Asian innovation, Asian connectivity and Asian service”. At the time, the mega-trends in Asia included a growing population, increased wealth, higher rates of urbanisation and the emergence of a tech-savvy, digital populace.

However, DBS did not have the physical reach of some of its competitors in Asia such as Maybank and OCBC Bank. Additionally, a failed attempt at acquiring Bank Danamon of Indonesia which had 9,000 branches in 2013 led the board and leadership to rethink their strategy. The CEO had this to say about the failed acquisition;

“After Danamon… it became quite apparent that everything we’d been doing on digital was still not enough and actually the penny sort of dropped that if we really scaled this up… over the next couple of years, it might actually allow us to do in a different way what we’d been seeking to do with an acquisition”

In summary, the main push for the digitisation drive was;

Vibrant tech scene in Asia including the likes of Alibaba, Tencent and Lazada. These were an existential threat to their business;

A few failed deals in branch expansion that made the CEO relook at their distribution strategy;

Stagnant or declining metrics such as ROE, growth etc;

Key Strategic Initiatives

Overall Drivers

DBS adopted the following principles which then bled into their technology and operations structure, organisational culture and design as well as key business initiatives. They decided that in order to succeed, their business model had to be underpinned by five key capabilities;

Acquire - Create the capabilities to digitally acquire customers through technology improvements as well as partnerships - ultimately drive lower acquisition costs;

Transact - Eliminate paper and create instant fulfilment - all transactions should be fully digital;

Engage - Drive sticky customer behaviours through content and embedding themselves into the customer journey - the CEO rightly argued that customers don’t care about banking, they just want to be able to book their holidays, buy a car and buy a home - it was important for DBS bank to be invisible;

A re-engineering of its ecosystems from pipes to platforms. The idea behind this is that banking was traditionally a pipeline (think silo) from bank to customer. The big tech companies were platforms with multi-channel and product capabilities delivered intuitively to customers;

Data - Be insights driven;

Additionally, the bank wanted to create a 26,000 person start-up by changing the entire organisational structure and culture. The key organisational principles were centred around 5 themes;

Being obsessed about the customer;

Being data-driven;

Encouraging staff to take risks and experiment;

Being Agile - including having agile development

Be a learning organisation;

Technology;

From a technology perspective, the following were the key initiatives;

Bringing the technology team in-house from 85% outsourcing to 85% in-sourcing. To be a tech company, they needed to have in-house tech. Technology infrastructure was successfully insourced into a 1,000 strong development centre in Hyderabad, India.

DBS designed a Digital Transformation Wheel;

Automate everything - including full test automation;

Developing high performing agile teams - embracing agile methodology;

Organise for success - reorganising infrastructure engineering to be more service oriented;

Shift from project to platform - shifting from individual projects that need approval or sub-committee reviews to give the freedom to a group of people who jointly operate and manage key technology platforms;

DBS leadership also reorganised technology into platforms. These were categorised into four platforms -

Business platforms - front facing;

Enterprise-support platforms - finance, HR and core banking;

Enterprise-shared platforms - customer data, customer servicing, AI, chatbots and API development;

Enabling platforms - cybersecurity, access management and architecture;

The head of innovation Bidyut Dumra had the following interesting quote;

“Up until now we have been running DBS as a business with technology supporting the business. The mandate for tech was that the business had a vision and an agenda, and tech would be supporting that vision and agenda. But as we entered the digital era, there was a stark realisation that from a customer perspective, as far as they're concerned, we're one organisation. So what we've decided is we will fuse the DNA of the business and IT into what we call platforms, with the same groups of people being responsible for envisioning, designing, building and deploying tech to customers. Instead of funding projects, we fund the platform. We look at what outcomes the platform can give and set it free. With that, we can really start to practice agile at scale”

This insight basically summarises the thinking that defined the whole IT restructure.

Organisational Structure and Culture

From a cultural and organisational structure perspective, the following initiatives were undertaken;

Communication - GANDALF - DBS came up with the acronym GANDALF meaning Google, Amazon, Netflix DBS, Apple, Linkedin and Facebook. Essentially, everyone had to see themselves as competing and operating like the successful Silicon Valley companies. This was an organisation-wide change. The CTO said “We weren't going to create this little starter innovation unit as an aside that was to disrupt the bank, which you've seen many organisations do. The whole bank was coming with us, and therefore we thought of ourselves as a 26,000 person start-up.”

An innovation group was established to foster cultural change. Innovation management team fostered agile practices and organised human centred design task-forces. There was also a start-up partnership team that interacted and developed the network with the fintech community;

Organisational and departmental KPI’s were adjusted to reflect the digitisation drive. If it’s not measured it’s not done.

Restructuring teams - traditionally business units were separate from technology and operational units with each having their own KPI. Within the new structure, teams were built based on specific products e.g. digital card issuance with both the business and tech leads having similar KPI’s. This was an insight gleaned from how Silicon Valley firms are run, a CEO and CTO dynamic;

From a learning perspective - everyone was allowed to engage in digital training including learning concepts like agile development, AI and machine learning and general app development. There was a project called “Maker” in which anyone from the bank could take a one week program and build a product from the ground up.

Of course, not everyone was on-board, the CIO David Gledgehill had this to say about the mindset change journey;

“Mindset change is a journey. Not everybody's going to get on board at the same time. Some people are going to outright reject it. We describe it as teaching cats and dogs to swim. You put the dogs in the water and they happily all react and have fun. Put the cats in, not so much. Some cats just look miserable and some fight back.”

I like this interview with Mr. Piyush Gupta

Main Wins;

DBS launched Digibank in India - a purely digital bank product that rode on the existing Aadhar biometric system to enable identification. This was later rolled out in Indonesia, a market in which they failed with an acquisition back in 2013. Digibank has over 2m customers and is adding around 100,000 per month in India.

DBS has launched marketplaces for cars, property , travel and electricity thus delivering on its idea of being embedded in the day to day lives of its clients. In a previous post on Open Banking in Kenya, I talked about the strategic need for banks to go up-stream.

The digitisation of existing customers has led to improved financial outcomes for the bank. The bank created metrics for defining their digital and traditional customers. Digital customers had a 27% ROE compared to an ROE of 19% for traditional customers. Additionally, digital customers generated twice the net profit vis-a-vis digital customers;

The bank has won “World’s Best Bank” for three years in a row from 2017 to 2019;

The stock market has rewarded DBS when compared to its peers;

Key Take Outs

Different banks have had different approaches. Standard Chartered which operates largely in the same markets as DBS has launched SC Ventures which is an entity tasked with investing in new fintechs, driving intrapreneurship within the bank, changing the culture and accelerating existing product initiatives. BBVA Bank has taken an almost similar approach focusing on acquisitions of fintechs to drive its tech strategy.

The Royal Bank of Canada has adopted an almost similar strategy to DBS Bank with a focus on re-platforming the entire banking offering. There a number of strategies that banks have adopted broadly categorised as; new offerings, partnerships, acquisitions and re-platformings. Here is a good summary of what banks have been upto;

My key learnings are;

It seems that customer-centricity ultimately is the critical ingredient - you should work from the customer back up to the technology rather than the other way round;

The technology discussion is more and more becoming one of orchestrating and composing technology for your business needs - shifting away from becoming a tech factory - it can be argued that in the long-term, technology will be a commodity just like how cement is just a commodity in the construction industry;

Culture and organisational incentives are super important and are arguably the most critical in any transformation project;

When analysing technology, it seems that understanding what part of the tech stack is offering most commercial value is the main super-power. It could be the data, the middle-layer or the API layer depending on what business you’re doing;

It seems also that thinking of your business in terms of your capabilities is key. Goldman has capabilities in FICC, transaction banking, wealth, analytics and trading. It has then focused on the API-fication of these capabilities to offer them as a service;

A number of African banks are facing or about to face the dreaded Core Banking System upgrade that occurs every 5-7 years. The thinking should be around asking less and less of your CBS i.e. just using the ledgers and the product engines whilst orchestrating everything elsewhere.

Ultimately there’s no one-size fits all approach and everyone will have to make decisions within their specific contexts. It will be an interesting ride for sure.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@gmail.com;

Is the decrease in the cost of capital from the expansion in the consumer business driven by its higher profitability, which reduces the need for additional capital raises? Or is it that the capital requirements for the consumer business are lighter?