The Digital Transformation Dilemma in Banks - Part 1

The current context in which banks are operating and the challenges that lie ahead.

All around us we read about the major challenges banks are facing amidst the rise of Fintechs. What is the future of banking and what role will banks play in the future? This is the first of a two part series that will analyse the existing banking environment in part 1 and chart the path that banks should take in part 2. Part 2 will be more of a thought experiment because I’m not clever enough to know what will happen to banks in 10 years. As always I prefer mental frameworks rather than broad predictions.

What I am trying to achieve in this article is to understand the context in which “disruption” is occurring in the African financial space, understand why banks operate the way they do as regards embracing technology, map out the threats that are facing banks and analyse some of the institutional issues that banks face.

Global Context

The Global Financial crisis of 2008 was a seminal moment in the growth of the current Fintech industry. The GFC gave rise to the following key themes that drive Fintech today;

Customers in the West, especially the younger millennial generation stopped trusting banks to do good. What were once seen as core trusted institutions within society were now seen as rogue actors which didn’t have the interests of the larger society at heart;

Increased regulatory scrutiny including a ratcheting up of capital requirements lowered Returns On Equity (ROEs) and made banks less attractive to the larger investor community;

The ensuing helicopter money policies carried out by the Federal Reserve as well as the ECB lowered long-term rates thus hobbling net interest margins, particularly in Europe;

Regulators forced banks to focus more on compliance than on business growth - coupled with legacy systems and processes - global big banks became slow moving monoliths with a poor customer value proposition and high costs.

These conditions, coupled with legacy IT infrastructure gave rise to the growth of the Fintech movement. Most of the current giants in the Fintech space were all born post GFC. Some examples are Stripe, Square, SoFi, MoneyLion, Monzo, Revolut and the likes. The founding themes mostly revolved around the ideas that; current financial services are poor, existing technology can enable us to offer a better value proposition and customers don’t trust banks to do a good job. Of course, quantitative easing and an investor base that wanted exposure to financials having been put off by the big bank returns offered almost perfect conditions for Fintechs to raise funds at increasing valuations.

This then is the global context in which the current Fintech moment needs to be viewed. Of course, the same context doesn’t apply necessarily to Africa. The GFC for sure had an impact on African banks, but the outcome was not as severe as in Western society. If anything, the most severe outcome was that smaller Tier 3 and 4 financial institutions lost their correspondent banking facilities due to stricter compliance standards.

The graphs below show bank Returns on Equity for the United Kingdom, Euro Area and the US banks with balance sheets of US$ 15b and greater.

Source: St Louis Fed - Federal Reserve Bank of St. Louis

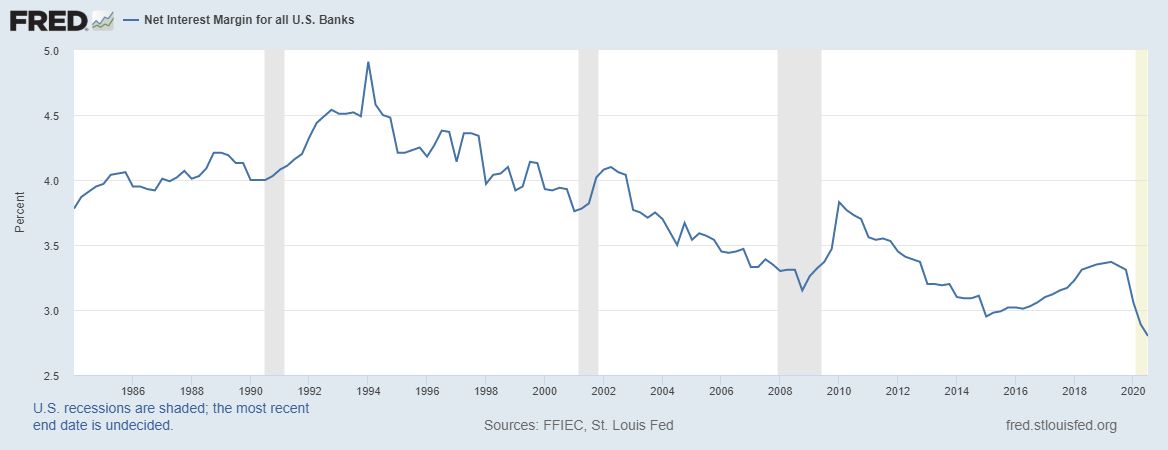

Levels of performance have varied between markets, nonetheless there are clear trends. ROE’s are now in their single digits in most markets particularly in Europe. In the USA, bank ROE’s have moved from the higher teens in the early part of the millennium to just about 10% in the last decade. What’s more, Net Interest Margins (NIMs) have collapsed across these markets. The graph below shows NIM’s for US banks which have dropped by almost half from the 90s.

Higher capital requirements and lower returns from lending have been made worse by increasing costs. Efficiency ratios are on average 63% in Europe and just under 60% in North America. This compared to a global average of just over 50% and just below 40% on average in Asia.

Source: Ernst & Young

The African Context

In Africa, the context is quite stark. I have analysed three major markets as is usual in this newsletter, Nigeria, South Africa and Kenya and randomly selected some key banks in each market. 2019 numbers were used to control for Covid-19’s impact on banks given varying responses to the virus. The graphs below tell the picture. In terms of ROE, the major banks in these countries all have healthy ROE’s of 20%+. In South Africa, their ROE’s are impacted by their diverse business structures. For instance, FNB Bank in South Africa had an ROE of 42% with the other business units such as Rand Merchant Bank and Aldermore lowering total group ROEs. Net Interest Margins in these markets are very attractive and thus a balance sheet play is profitable, unlike in Europe.

Additionally, the businesses particularly in South Africa are well diversified with non-funded income accounting for 50% of total revenues in South Africa and around 30% in Nigeria and Kenya. All these banks have developed digital products for their customers which have reduced branch footfall and increased the ratio of digital transactions to total transactions. In Kenya, KCB and Equity both have over 90% of total transactions occurring within their digital channels. Using Google Play app ratings for their core mobile app propositions, South African banks have the best apps with an average rating of 4.33 whilst Nigeria follows with 3.85 and Kenya lags with an average of 3.43.

Source: Respective Bank Annual Reports 2019

All this is to say that African banks have fared well commercially in the post GFC era and have successfully managed to develop digital propositions. Some interesting examples are the M-Shwari and Fuliza developed in partnership with NCBA and Safaricom in Kenya.

Additionally, African Fintechs have been complimentary to banks rather than existential threats. The likes of Paystack, Flutterwave, Nomanini in South Africa, MFS and others all add value to banks and partner with banks.

False Security

All that said, looking forward, banks will need to navigate two major issues. The first one is a generational shift in the client bases and the second one is the technological change, currently captured in the misnomer that is called “Digital Transformation”.

Dr. James Mwangi, the legendary CEO of Equity Bank Group best captures the context. It is a sign of his visionary leadership that he could articulate the challenges the bank is facing in such a crisp manner when he was talking of the brand transformation that Equity bank executed in 2019.

...We took note of the fact that our external context is changing rapidly given two key factors, technology and demographics. For several decades, the banking sector’s business model had been relatively unchanged hinged on brick and mortar branches and client facing services. This has changed radically in the last few years with technology enabled channels becoming the main means by which clients interact with financial products and services… This wide generational spectrum presents challenges and opportunities in terms of delivering relevant products and preferences of channels. While our legacy customers prefer to use branches and engage directly with the bank through people facing functions, the younger generation is interested in convenient channels that empower them to conduct their own affairs anywhere anytime. Today we are engaged with a large and growing demographic that wants to consume banking in a different way and views financial services not from a utilitarian perspective but from an experiential and value perspective.

Essentially, the tricky situation African banks face is to delicately manage the existing demographic that is responsible for the large part of bank financial performance whilst navigating a transition into a 21st century financial services provider to cater for the gen-z and millennial opportunity. It is critical to understand this, the current branch-based business model is profitable and has legs to run even further, nonetheless banks are cognisant that in the long-term, change is essential. How do you balance existing profitability whilst preparing for an uncertain future?

To make things even harder is a general misconception of what banks “need to do”. Bank annual reports are littered with terms such as “digital transformation”, “digital channels”, “products”. In a period of such rapid change and “disruption”, it is important to have the following mental framework that Jeff Bezos and Warren Buffett apply. Below is a quote from Jeff Bezos.

“I very frequently get the question: 'What's going to change in the next 10 years?' And that is a very interesting question; it's a very common one. I almost never get the question: 'What's not going to change in the next 10 years?' And I submit to you that that second question is actually the more important of the two -- because you can build a business strategy around the things that are stable in time. ... In our retail business, we know that customers want low prices, and I know that's going to be true 10 years from now. They want fast delivery; they want vast selection. It's impossible to imagine a future 10 years from now where a customer comes up and says, 'Jeff I love Amazon; I just wish the prices were a little higher,' [or] 'I love Amazon; I just wish you'd deliver a little more slowly.' Impossible. And so the effort we put into those things, spinning those things up, we know the energy we put into it today will still be paying off dividends for our customers 10 years from now. When you have something that you know is true, even over the long term, you can afford to put a lot of energy into it.”

Rather than try and predict what the future holds, what is more useful is to start with what is not going to change. This on the other hand is predicated on being a customer first organisation and asking what will customers still expect from their financial service providers in 10 years? I take it they will still expect low cost financing, safe custody of their money, intuitive payment experiences and suitable and affordable financial services. If you have worked in a bank before, you would know that customers are often the last things on our minds. Often what other banks are doing is of primary importance.

Banks are thus having to face a technological challenge with the wrong mental frameworks about how technology is impacting banking. The current thinking around “products” and “digital transformation” is wrong. The thinking should be centred on what a customer expects as regards his financial well-being.

A picture of a steam-engine powered factory.

This is akin to what happened to factories with the invention of electricity. Factories in the early 20th century were powered by steam engines which through a central shaft powered the entire factory often powering adjacent buildings. The centralised steam engine had to be switched on to power even the smallest function such as a hammer.

The invention of electricity did not have the immediate impact on productivity because factory designers still designed factories around a centralised power source. Only with a younger generation of new managers did productivity improve. Managers realised that they could design a factory around a workbench with each station having an individual power supply. Electricity enabled power to be delivered to exactly where it was needed. This then enabled an explosion in productivity growth that was responsible for much of the wealth generated in the 20th century. The digital transformation narrative is similar to this, bank managers are currently focused on how to deliver their existing products through digital channels. They should nonetheless be asking themselves; using existing technology, how can we better offer financial services to customers. Google did not set out to digitally transform advertising and Netflix did not set out to digitally transform the video rental market. It is in principle a framing issue.

Additional Challenges that Banks Face;

In addition to the demographic challenges and the wrong mental models for understanding technology, banks have existing issues that are not often talked about when it comes to competing in a modern tech-first world.

Mis-alignment of managerial incentives - Most of the modern tech companies have an owner operator managerial culture where incentive alignment is well designed. Banks on the other hand due to their societal function often tend to have custodial managers i.e. career professionals on a contract basis and often with little to no equity in the bank. This then creates incentives where the biggest concerns for management are.

Not rocking the boat or doing anything that brings about career risk - steady as she goes mentality;

A focus on keeping up with the competition so as to not be “left behind” professionally;

Always having plausible deniability when it comes to making big decisions thus a proliferation of vendors and consultants who will always take the fall if decisions go wrong;

Note though that these are some of the most capable and talented managers in the world, just with the wrong incentive structure. It is no surprise that Equity Bank has been a leader in the utilisation of technology to advance its business.

Most banks have well designed executive/graduate trainee programs where young people fresh out of college with gleaming CVs are recruited. These programs offer a fast track to management for these bright young people. Nonetheless given that banks haven’t changed for decades, these trainee programs are often akin to an indoctrination into a priesthood with the main message being “this is how things are done here”. Career progression is thus based on how much of a “Bank A man/woman” you are. Thinking outside the box is thus career risk.

Given that banks haven’t changed in many years, career growth is based on sales and marketing capabilities i.e. who can bring the most business. Product thinking is relegated to the margins, you then have a situation where the top leaders are sales guys. In my experience, a great salesman often doesn’t think too much about a product. Great sales guys love the thrill of the sale and are often not concerned about product features. If these form the core of the executive leadership, you have a situation where nobody at the top is talking about the “product”. The video above by Steve Jobs best captures this.

The institutional imperative, best defined in Warren Buffett’s 1990 Berkshire Hathaway letter to shareholders ties points 1 and 2 above together. With an Executive management focused on career risk and survival with a supporting cast also focused on career risk and survival, the institutional imperative manifests itself in vanity transformation projects which are supported by management regardless of their real merit. If they fail, a “transformation” leader is fired and the consultants and vendors lose a client while the world moves on;

Being a bank man/woman has an additional pernicious impact on decision making. Most of the successful tech companies are built upon data and the clever manipulation of data to offer better products and services. The founding principle is that “we don’t know” thus let’s use data. Bankers on the other hand are supposed to have a magic sauce and intuition built on years of experience and know how on what works and what doesn’t. Bankers therefore are reluctant to apply big-data and analytics because “what will happen to me then?”

A siloed organisational structure with each department launching new products to drive its divisional P&L. Additionally, product sales thinking dominates the discussion thus banks fail to look at the integrated customer experience. An analogy is how Apple disrupted the music industry with the Iphone and Itunes. Sony had a very powerful hardware division with a track record of being a pioneer in portable music with the Walkman and Discman. Sony also had the largest catalogue of music with the Sony entertainment division. Nonetheless these two divisions didn’t speak to each other and Apple cleverly reconfigured how music is delivered with both hardware and the music catalogue.

This excludes technical issues such as core banking systems and technical debt. African banks thus face significant challenges in the coming decade, despite having successfully navigated the last 10 years post GFC. Considerable thought should focus on how to maintain profitability in the near to long term from existing business whilst preparing capabilities around technology, managerial incentives and organisational structure that will enable banks to tackle the challenges ahead.

The next article will look at how some banks are responding to these threats, using three global bank examples. Strategies will vary based on how a variety of factors.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@gmail.com;