Macro view of the Drivers of the Neobank Opportunity in Africa

Zooming out to look at the Macro picture in South Africa, Nigeria and Kenya and the impact on Neobanks

This week’s post is a follow up of last week’s discussion about Neobanks. In last week’s post, the discussion centred on three successful global Neobanks and the common threads that drive their success. These common threads were;

Start with a clear target market in mind which can lead to sustainable profitability from this segment alone - In my view the most important criteria;

Build the technology from first principles rather than adapting any conventional practices;

Following on from no. 2 above, the technology approach is not one of a tech arms race towards the most advanced and complex tech stacks, rather the efficient use of available technology platforms to deliver your product to customers. The technology play thereby leads to tech valuations rather than balance sheet business valuations;

Have a direct relationship with the customer and offer an exceptional experience that leads to referrals - referrals drive lower cost of acquisition over time - Create a flywheel;

Have a very solid commercial focus - commercial rigour should underpin all the decisions you make;

Own the balance sheet - you need deposits. The ability to lend from deposits is the ultimate super-power in banking.

Of course, the target market and opportunities were based on macro factors such as good interest margins in Russia and an underserved credit card market.

The focus then turns to Africa and the different opportunities that arise within the Neobank space. I will focus on three countries only, Nigeria, South Africa and Kenya. The respective economic powerhouses of West, Southern and East Africa. The three countries accounted for 53% of venture capital invested in Africa in 2019. Of course this is not to throw shade at other significant countries such as Tanzania, Ghana, Uganda and the likes. It just makes the analysis easier.

I’m a strong believer that the financial industry and the nature of banking franchises are driven by the macro-economic factors, big picture factors present in the markets in which they operate. A bank that was formed in one market is designed to take advantage of the business opportunities and challenges present in that market. Other existing macro factors can then supercharge this model. An example is the Post-Election Violence and the impact on M-Pesa.

This model then becomes difficult to export to other markets. The same analysis will extend to Neobanks. Therefore analysing the neobank opportunity has to start at a macro, big picture level. Thereafter one can look at the opportunities that will present themselves locally. I will just look at general economic issues and then analyse the existing infrastructure.

General Economy

South Africa, Nigeria and Kenya are the biggest economies respectively in Southern Africa, West Africa and Kenya. When analysing the general economy, what I think matters are three core elements;

Nature of production i.e. what are the factors contributing to overall GDP;

Exchange rate environment - how the currency is managed;

Overall macro stability represented by the average inflation and interest rate levels;

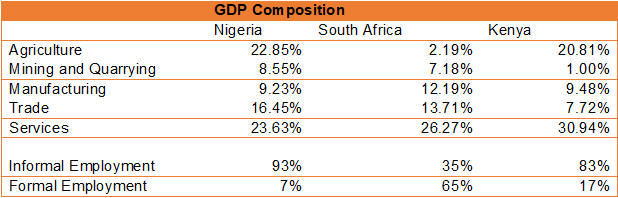

GDP Composition

Source: Respective country Statistical Bureaus and International Labour Organisation

The three economies are all diversified without any single industry being dominant. South Africa and Nigeria are commodity based economies with minerals in South Africa and Oil in Nigeria being key economic drivers. Agriculture accounts for around 20% of output in both Kenya and Nigeria with export crops like tea, coffee and horticultural crops playing significant roles in Kenya and Cassava, palm oil and yams dominating in Nigeria. The dominance of Agriculture, particularly small holder friendly crop production leads to the dominance of informal sector employment. Informal employment is 93% in Nigeria and 83% in Kenya. It’s important to highlight this in more detail. The formal/informal dichotomy plays a key role in the nature of banking services delivered to these markets. Additionally, the nature of crop production i.e. organised small-holder also has an impact on the markets served.

Services have been growing in both Nigeria and Kenya, particularly the ICT sector, finance, real estate and other professional services. In South Africa, the finance and real estate sectors are advanced with much higher financial inclusion rates for both banking and insurance.

Source: Little Red Book on Financial Inclusion 2018 Edition

Financial inclusion is significantly lower in Nigeria as compared to South Africa and Kenya. In South Africa, the higher level of formal employment leads to a higher percentage of people with bank accounts and higher utilisation of borrowing as well as debit card utilisation. In South Africa, consumer credit accounts for 44% of total lending in the economy, in Kenya this ratio is 28% whilst it’s only 8.4% in Nigeria. This goes to show that banks in Nigeria have been designed around lending to corporates customers in the manufacturing and oil and gas sectors. In Kenya and South Africa, banks have been designed to cater to both mass market and corporates. In Nigeria, a bank can probably make 100m$ just by issuing LC’s to Dangote Group, why then bother with the hustle of retail lending?

Exchange Rate Environment

South Africa, Nigeria and Kenya all have free floating exchange rates where demand and supply determines the exchange rate at any given time. Nonetheless, the strictness of capital controls varies between the countries. South Africa is much more strict than say Kenya when it comes to managing capital outflows whereas the Nigerian Central Bank is much more active in determining the exchange rate in Nigeria. This is often done through sales of FX by the Central Bank of Nigeria. One can argue that the three countries have varying levels of a managed floating currency.

The exchange rate policies also have to be seen in line with the nature of imports and exports. Kenya and South Africa are oil importers whilst Nigeria largely imports food and refined petroleum with a relatively less developed primary manufacturing base, albeit growing significantly.

Nonetheless, in recent years, due to the wild fluctuations in oil prices, Nigeria has had significant issues with the exchange rate markets leading to a situation where there are multiple exchange rates. The black market rate which in most countries is the real exchange rate trades at a premium of 20-30% of the Investors and Exporters rate. Such differentials in exchange rates are pretty nefarious in my experience. They act essentially as a wealth transfer from the poor to the rich given that imported inflation is felt more by those who have access to the black market rate.

Furthermore, the official rates are only accessible by the powerful and connected. Imagine waking up, having access to US$ 10m and immediately being able to make US$ 3.0 million the same day by trading it in the black market. This arbitrage is very prevalent in many countries with dual exchange rates. This is why Bitcoin adoption in Nigeria has been so aggressive. The duality of rates and the controls on who gets the IE rate does not sit well with the younger generation who have grown up in a permissionless internet world. They will build their own solutions on top of cryptocurrency Regulator or not.

Monetary Environment

Source: World Bank Data

When it comes to overall macroeconomic stability, South Africa leads the pack whilst Kenya and Nigeria have similar levels of stability. Overall inflation and lending rates are lower in South Africa and have been in single digits for the better part of this millennium. The Kenyan lending rates have on average been lower than those in Nigeria whilst inflation has also been lower apart from a short period at the start of the last decade. The relative stability levels are driven by factors like food and energy inflation.

Lending rates in Kenya were freely set by the market until an interest rate cap law was introduced in 2015. This was later repealed but it is still de facto present through “stringent monitoring” by the Central Bank of Kenya as well as strange monetary policy. Nonetheless all this goes to show that these three markets can all support healthy Net Interest Margins from a lending operation. In South Africa, NIM’s hover around 4-5% whilst those in Nigeria and Kenya are often double digits ranging from 10-15%. The recent financial results from Carbon (here and here)show this, the bank was profitable despite having such high rates of credit loss.

General Infrastructure

Identity Infrastructure

When analysing Identity infrastructure, the two core considerations would be; how many births are registered via birth certificate and how many adults have a national identity document. This is a proxy of the depth of the administrative system as well as the reliability of ID for KYC.Fringe considerations within the financial space can include the percentage of adults with credit bureau coverage.

Source: World Bank State of Identification Systems Report 2017

South Africa and Kenya have more robust identification systems. Only 38% of births are recorded in Nigeria according to the World Bank. When it comes to national ID, only 6% of Nigerians have ID. This was as of 2017, since then Nigeria has launched a new digital identification system. In Kenya, your ID enables you to open bank accounts, purchase insurance products as well savings and investment products. The same applies to South Africa.

As regards credit bureau information, over 60% of adults in South Africa have credit bureau coverage with only roughly 16% in Nigeria and 40% in Kenya.

Nigeria has a significant infrastructure deficit when it comes to identification which is core for banking. KYC has never been more important in the banking space and without robust identification mechanisms, scaling a banking product becomes difficult. Of course a number of Fintechs are coming into this space such as Evolve Credit and Smile Identity.

The identity deficit in Nigeria leads to a situation in which banks ask for multiple pieces of information such as a utility bill, a letter of recommendation and multiple forms of identification. The on-boarding process in Kenya has become much smoother since the turn of the millennium where often an ID and picture suffice.

Bank Network

As regards to bank networks, South Africa has the widest reach with 10 bank branches per 100,000 people compared to 5 and 4.3 in Kenya and Nigeria respectively. As regards to ATM coverage, South Africa leads again with 66 ATMs per 100,000 people compared to 16.9 in Nigeria and 9.2 in Kenya respectively. In Kenya, the network is augmented by over 90,000 bank agents and over 230,000 mobile money agents. In Nigeria, the agent network has been experiencing explosive growth with the number of agents growing by 516% in 2019. Total agents stand at over 236,940 as of December 2019 from 38,416 in 2018. The agent growth in Nigeria is supported by the Shared Agent Network Expansion Facilities (SANEF). The target number of agents for 2020 was 500,000 agents.

Payments System;

Payments system are typically divided into two layers - higher value payments and lower value payments. For Higher value payments, most payments systems are quite similar. There is usually the presence of an Automated Clearing House (ACH) that manages cheque payments and Electronic Funds Transfers (EFT). Another standard element usually is a Real Time Gross Settlement (RTGS) system. Layered on top of all this is the international SWIFT system for international payments as well as many regional payment systems.

At the lower end is where there is usually a high degree of variability due to different levels of infrastructure development. In South Africa, card payments are dominant and account for the bulk of retail payments. In Kenya, lower value payments are mostly done on M-Pesa as the de-facto payments layer of Kenya.

In Nigeria, there has been an impressive growth of the NIBSS Instant payment service which managed over 2 billion transactions in 2020, almost doubling 2019 volumes and processed transactions worth over 415 billion dollars or roughly 94% of GDP. Cash also plays a key role in all these economies, despite it’s advanced infrastructure, cash still accounts for over 72% of lower value payments in South Africa.

The NIBSS Instant Payment service looks the friendliest to Fintechs as it enables real time account to account payments. Fintechs and PSPs can integrate to this service to process payments. In Kenya, M-Pesa has done a great job to develop such a wide and reliable infrastructure. Nonetheless, it’s hard to innovate on top of a private business that offers P2P and C2B as its core product offering. There is a real need to develop a NIBSS like service in Kenya.

In terms of the payments system, Nigeria seems to be doing better than Kenya and South Africa albeit both have 5 year roadmaps to modernise their systems.

Putting it all Together;

The Neobank and general fintech space will be defined by the problem space. From an overall macro and infrastructure perspective, Nigeria seems to have a bigger problem set and therefore bigger opportunity space. This has been evident in the rise and rise of infrastructure players in the Nigerian Fintech ecosystem.

Players such as Paystack, Flutterwave, Wallets Africa, Evolve Credit, Onepipe, Okra and Mono are leading in this regard. The underlying infrastructure has then given players such as Kuda and Carbon an opportunity to operate. These two are targeting the consumer space which from the preceding analysis has been under-served from a credit perspective as well as the overall ease of client onboarding. Carbon for instance has already scaled to over 2.2 million customer accounts which by number of customer accounts would make it the 5th largest bank in Kenya. The retail neobank opportunity in Nigeria is real. I am very bullish about the growth prospects here, one key mental model to better understand why is the funnel framework. Modern companies will win by demand aggregation rather than supply i.e. the best customer experience will win since the internet is the great equaliser when it comes to distribution.

Nonetheless, some of these businesses will not travel easily. Banking will be very much a local play and success in one market may not necessarily mean success in another. For the big banks, regional expansion has worked well within defined spheres of influence. West African banks have succeeded in West Africa but struggled in East Africa. East African ones have not even ventured past DRC.

It seems Nigeria is where the action will be in the medium term given that there is a modern instant payments system that can scale as well as a problem space that drives an opportunity for innovative players to attack. Additionally with the FX challenges previously discussed, cryptocurrency presents a clear solution for international payments and trade. Players such as Bundle and Bitsika are leading in this space. Nigeria is the third highest country in the world in terms of Bitcoin trading volumes. Recent developments by the regulator could however adversely affect the crypto players.

The Kenyan and South African neobank space will be a bit tougher to crack due to the presence of a relatively well advanced banking system. Additionally, the presence of M-Pesa complicates matters in Kenya. Savings and Credit Cooperatives are a key plank of the financial sector in Kenya as well. Clients don’t walk around thinking, “I need to bank with a neobank”, most want to either buy a house, save money or pay for their education. These problems have existing working solutions in Kenya and South Africa.

The plays here will have to be longer-term in nature and in the case of Kenya, a lower value instant payment system that can onboard Fintechs and other PSP’s will be a necessary and vital ingredient. In South Africa, players such as Tyme Bank, Discovery Bank and Bettr Finance are leading the space. These are largely offerings targeted at the Millenial and Gen Z demographics who want digital experience. Based on the user experience, there is a longer-term advantage that will accrue to these players

. In Kenya, Carbon is launching in the market. There is a player called Umba which is also targeting to be a digital bank. There are as well offerings from incumbents such as the Vooma app by KCB. The jury is still out on all these just because M-Pesa is King and rightly so.

One has to note that Nigeria already has a well advanced open banking initiative as well as the NIBSS Instant Payment service. They have the required ingredients to incubate successful neobanks. Their 2012 “vision 2020” payment system strategy has turned out quite well.

In the interim, one of the major opportunities I see in Kenya is converting a tier3/4 bank into a banking infrastructure provider. Essentially, sit in the background and offer your license and infrastructure to enable fintechs to build on top. Providus Bank of Nigeria has done this with remarkable success and is offering its infrastructure to some of the major players in Nigeria. The business model would basically be to use Fintechs to generate liabilities and commissions for cards, payments and FX whilst having a very low-risk vanilla corporate lending business. This would generate NIM’s of 10% whilst your staff costs would be negligible.

In 10 or so years the banking sector in Africa will look very different from today. Players such as Carbon and Kuda could become consumer banking giants in West Africa. It will be a very interesting ride.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@gmail.com;

As a post-script, over the weekend it seems that Providus bank stopped providing virtual accounts to it’s Fintech partners. This very shortly after the CBN banned Crypto. It seems the Empire strikes back.

There are various opportunities across the financial value chain in Nigeria; KYC, deposit, credit... It's nice to see products come up and take their space in various part of the chain.

Nice one!