Fodder for Future Neobank Founders

Analysing successful Neobanks and distilling the lessons

In the past few years we have witnessed a surge in the launch of Neobanks or Challenger banks which are mainly digital native banks built for the 21st century. Brand names such as Revolut, Monzo, N26 and Starling Bank clearly come to mind and are synonymous with the term Challenger Bank. The space is new and growing and it’s worth taking a deeper look at what exactly is happening.

At the heart of the launch of digital banks are a number of technological and non-technological tailwinds that are driving these business models. From a technological perspective; advances in cloud computing, the maturing of the API economy, deeper smartphone penetration and significant improvements in broadband, artificial intelligence and general computing power. From a non-technological perspective, factors such as the Global Financial Crisis which caused a re-think in how we view and relate to banks, demographic factors such as the coming of age of Millenials and Gen-Z’s (my favourite generation) and shifting customer preferences towards more digital experiences.

The basic fundamentals thus all point towards an ever growing sector that will take more and more market share from incumbent banks. Despite all this, as with anything new and shiny, there will always be hype and euphoria. Like with many fundamental technologies, they are always overrated in the short-term and underrated in the long term. I decided to look at three different Neobanks and analyse if there are any common factors or criteria that lead to higher odds of success. The criteria I used to select these banks are;

Technology is at the heart of the business model - they are digitally native and have technology company economics;

They have a modern tech stack that enable scale at lower and lower marginal costs;

They are profitable;

They have bank-like balance sheets and profit and loss statements i.e. you can run comparable analysis to existing banks.

Using these four criteria which are not necessarily exhaustive, I settled on three challenger banks. The term challenger banks may actually put off the founders of these companies - they are ultimately banks, but riding on modern technology and built with first principles from the ground up. The three banks are;

Tinkoff Bank - Russia;

Oaknorth Bank - United Kingdom;

Webank - China;

With each bank, I’ll give a brief profile of the bank, origin story, markets served, balance sheet and income statement profile and brief discussion of the technology behind it. Again, a strong disclaimer that I’m not a techie and therefore my tech discussion is very rudimentary.

Tinkoff Bank;

Tinkoff Bank, formerly Tinkoff Credit Services was founded by Oleg Tinkov in 2006. Fresh off the sale of his Brewery business to Ab Inbev, Tinkov was looking for a new challenge. He admired the Capital One business in the USA which was based on issuing credit cards through direct mail. He hired the Boston Consulting Group to drill deeper on whether he could launch a branchless bank that sold credit cards through direct mail to Russians. At the time, despite having a population roughly half the size of the USA, the volume of credit cards in the US was almost 60x the volume of credit cards in Russia.

Mr. Tinkov then proceeded to build a team to execute this and hired Mr. Oliver Hughes who at the time was in charge of growing the Visa business in Russia. One of the quirks of the Russian market is that the Central Bank mandates all banks to have physical KYC verification of customers. Tinkoff thereby had to not only develop a system to issue and mail credit cards across the country, they also had to develop teams of people who had to do the physical verification of customers. This of course in addition to the core technology stack that they had to build to be a truly digital bank. In essence, Tinkoff Bank had to start its business by executing exceptionally difficult tasks. The target market was retail mass affluent Russians.

Summary of Business Model;

Tinkoff Bank is a SME and Retail bank offering financial services, credit, investments and insurance all under one roof. They offer a debit product called Tinkoff Black which acts as an entry way into higher margin products such as credit cards, lending and insurance. Credit cards account for over 75% of their gross revenue although this figure has fallen from 95% back in 2014. In the last five years, insurance premiums, SME account commissions and brokerage services have shown a CAGR of 87%, 174% and 75% respectively. A flywheel effect is in place where quality customer service leads to more customers which leads to better data and therefore better cross-selling which drives up revenues.

Key points I liked about Tinkoff;

Tinkoff has built its core technology from the ground up and outsources where necessary;

The bank has been able to build a financial supermarket of sorts with insurance, investment brokerage, debit cards, SME lending and consumer lending;

Tinkoff as 11 IT centres spread across Russia together with a virtual development centre;

Over ⅓ of Tinkoff customers have more than one product;

The bank has over 13% of the Russian credit card market and 8.1% of the retail lending market for loans with a tenor of less than 3 years - in both instances the second largest player behind state owned Sberbank;

Tinkoff go through a rigorous product approval process with each product having to show positive returns with a 30% hurdle rate;

Operating in a capital scarce market, the bank has had to be profitable from day one;

Tinkoff has spread into different financial verticals successfully and can be thought of as a mashup of Stripe, Square Capital, Metromile, Revolut and Robinhood;

Tinkoff has over 5 million MAU’s and over 2 million DAU’s;

The CEO in the 2019 Annual report had this to say about Sustainability - “our business has never been more sustainable. Here I don’t mean statistics like responsible lending, CO2 emissions and the profile of our workforce Important though they are. I mean fundamental business sustainability” - This shows the kind of commercial rigour that runs through the bank;

In essence, Tinkoff has combined exceptional technology and execution, solid financial discipline and exceptional customer service to create a world class digital banking operation. As of fiscal 19, Tinkoff had operating profits of 600 million US$ and a balance sheet of 7.6 billion US$. The bank had an efficiency ratio of 48.9% and an ROE of 37.6%. As of September 2020, operating profits stood at 537 million US$- on trend to surpass 2019 figures despite being the year of the pandemic. Quite simply, Tinkoff is an amazing business from a commercial perspective.

OakNorth Bank

Oaknorth Bank is another fantastic digitally native bank. Oaknorth was started back in 2014 by Rishi Khosla and Joel Perlman. The two had been partners in a previous successful analytics business which had scaled to 3,000 staff over 11 or so years. They exited the business through a sale to Moody’s Corporation.

The key insight for them was that as entrepreneurs in a successful mid-size enterprise, they struggled to get non-collateralised lending despite being a very successful business. Banks simply did not take the time to understand their business and had a commoditised approach to SME’s. Banks did not find it useful from a cost to serve perspective to finance Small and Medium Sized Businesses given the smaller ticket sizes.

Banks had over time built lending models that were unfit for purpose and that clumped retail and SME clients together, despite having fundamentally different characteristics. A “computer says no” model as founder Rishi Khosla called it. This was fundamentally a data issue so the founders set out to build advanced data and credit models that enabled four key things;

Better insight into the customers credit risk;

Lower cost to serve from an originator perspective (Think Relationship Manager);

This lead to enhanced pricing thus marginal revenue per customer; &

Better loss ratios;

They set about to do this by hiring the best data scientists recruited from Palantir, Amazon and Google. The task set out was to build an advanced analytics system based on advanced machine learning and AI. This analytics engine sat on top of a Mambu core banking platform. The model unlike most credit models was forward looking thereby fitting well into the typical SME profile.

The basic commercial model was that Relationship Managers/RM’s could be significantly more productive if they had built for purpose technology platforms that enabled them to on-board customers, run detailed credit checks and initiate the origination of loans. On top of this, OakNorth would offer their credit modeling system to other banks as a service. As of early 2020, Oaknorth had originated over US$ 4 billion dollars as Oaknorth bank and over US$ 6 billion for other institutions. Thus the Oaknorth platform had initiated total credit facilities worth US$ 10 billion dollars. Oaknorth bank served middle market customers with a ticket size ranging from 500,000 pounds to 20 million pounds. Of the US$ 4 billion originated, only 5 RM’sand 3 credit people were required and .

The flywheel therefore is better lending decisions, lower cost to serve, improved efficiency and higher demand for their credit platform. The figures bear it out. From inception in 2014, the total balance sheet has grown by a CAGR of 131.7% to over 4 million US$. Total revenue has grown by a CAGR of 405.3% to 142 million US$ with net profits sitting at US$ 68 million. This from a loss position of 349,000 dollars in 2014. Oaknorth has a net profit margin of 47.9% and an efficiency score of 24%. The long-term projected efficiency score is around 16% with an ROE of 30-40%. Of note is that banks in Africa have efficiency scores that range from 50 - 70%.

Some things I like about Oaknorth;

Oaknorth has a willingness to consider multiple collateral types plus reducing credit approval cycle from 6 months to a matter of days;

80% of deal flow is driven from referrals thereby leading to a cost to serve of 1% of year 1 client revenues;

Oaknorth launched a mortgage product targeted at entrepreneurs with a non-standard income profile;

In USA, they're offering the model plus they have a team of originators both for banks and non-banks to offer a new asset class;

They have created a pandemic based system that analyses how a company will deal with coronavirus;

Khosla puts OakNorth’s success down to its principles, which he described, simply, as being in business to make money;

They seemed to have managed the pandemic very well and are on course to aggressively grow business;

Financially;

Total assets have grown by a CAGR of 132% from US$ 1.6 million dollars in 2014 to over US$ 3.8 billion in 2019;

Customer accounts have grown from US$ 15 million in 2014 to US$ 2.7 billion in 2019 - a CAGR of 267%

Loans and advances to customers have grown by a CAGR of 243% from US$ 20.4 million to US$ 2.8 billion;

Net profits stood at US$ 68 million in FY 2019 having grown from a loss position of US$ 349,000 in 2014;

Net profit margin stood at 48% in 2019 from -1490% in 2015. The cost to income excluding provisions stood at 24% in FY 2019 - management guidance puts this figure towards 16% in the long run;

Diagram 1: Oaknorth Bank Efficiency Margin and Net Margin

Diagram 2: Oaknorth Bank NIM and ROE

WeBank China

Webank is the ultimate pinnacle of technology driven banking. Their technical expertise makes everyone look amateurish. No, I’m serious. Webank is at the bleeding edge of technology and from a tech perspective seems to be miles ahead of everyone.

WeBank, a company backed by Tencent was launched in December 2014 with a view of offering financial services to a large mass of under-banked and under-served clients in China. The big state banks like in many markets were focused on extremely low risk conventional bank customers. With the growth of e-commerce and trade in China, a class of SMEs and individuals with non-conventional income profiles was largely unbanked or under-banked. With its affiliation to Tencent and the on-going de-IOE (movement away from traditional American IT giants IBM, Oracle and Dell EMC which offer the tech stacks of most legacy banks) movement that was spreading in China, Webank built its technology from the ground up using open source principles.

One of the first products launched by Webank was “WeiLiDai”which was a digital lending platform that was distributed through Wechat and QQQ. Using advanced technology and rich credit models, 10 million lenders were on-boarded through WeiLiDai by October 2015, just 10 months after launch. The average borrowing amount was US$ 1,237 dollars with a repayment period of 52 days. Webank has gone on to add more products such as WeiYeDai, a small business loan and WeiCheDai an auto loan. Interestingly, over 64% of WeiYeDai borrowers were taking their first loan within the financial system.

Some key elements of WeBank’s technology;

WeBank is also the world's 1st bank to fully deploy its core banking systems on private cloud. It has constructed a 100% in-house designed distributed core banking system with self-owned intellectual properties, capable of handling high-volume, high-frequency transactions. WeBank's big data platform houses over 15 petabytes of data, with over 300 thousand batch jobs being processed daily;

WeBank runs on what they call ABCD technology - this stands for Artificial Intelligence, Blockchain, Cloud Computing and big Data;

Using these frameworks, Webank handles over 1 million customer enquiries per day with over 98% of these being handled by chatbot;

Webank’s e-KYC facial recognition systems have fulfilled over 640 million identity verification requests as of early 2020;

In 2019, Webank filed 632 patent applications - the highest amongst banks globally further strengthening its credentials as a major player in not just banking but technology;

WeBank believes in open principles - three elements of open platform, open innovation and open collaboration underpin their commercial strategy. They want to use their technology to empower other partners within their ecosystem

It truly is a technology company with a banking license.

How then does all this look financially?;

Operating income rose from US$ 34 million dollars in 2015 to US$ 2.3 billion in 2019 - a CAGR of 185%;

Pre-Tax profits rose from a loss of US$ 90 million in 2015 to a surplus of US$ 640 million in 2019;

Total assets rose from US$ 1.5 billion in 2015 to US$ 45 billion in 2019 - a CAGR of 135% - Even 1st year assets of 1.5 billion are really impressive. Some European challenger banks took 3-4 years to reach such an asset base;

Loans and advances to customers grew from US$ 597 million in 2015 to US$ 25 billion in 2019 representing a CAGR of 155%;

Deposits from customers grew by a CAGR of 535% from US$ 22.5 million in 2015 to US$ 36.6 billion in 2019;

Currently, Webank has a net profit margin of 26% and an ROE of 25% - all these metrics are trending higher;

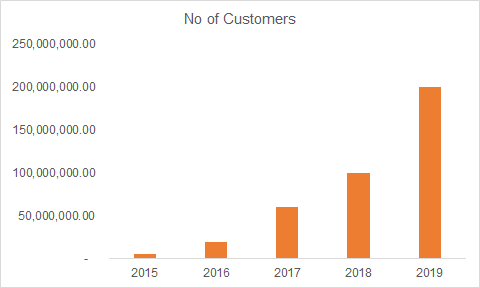

Total customers have grown from 4.6 million customers in 2015 to over 200 million customers in 2019;

It costs Webank 0.5 cents to serve a customer whereas current incumbents have cost to serve costs that are 20-60 times higher;

Diagram 3: Webank Return On Equity and Net Profit Margin

Diagram 4: Evolution of Customer Numbers;

I really cannot do justice to the scale and breadth of Webank’s technology. You could check out the following links - Link 1 - Link 2 - Link 3.

The Webank flywheel is quite similar to Tinkoff’s flywheel - world class technology - lower costs to serve - lower costs of credit - more customers - more cross sell opportunities.

Key Lessons;

As a post script - all the above banks seem to have done well in 2020 despite the corona virus. Arguably, their digital nativity could be the reason for their resilience and success in 2020. From the analysis, the key conclusions for me when it comes to building a successful neobank are;

Start with a clear target market in mind which can lead to sustainable profitability from this segment alone - Tinkoff with underserved credit cards, Oaknorth with SMB’s and WeBank with underbanked Chinese. This is a basic part of business that has somehow gotten overlooked in the growth at all costs start-up mentality world that we live in. Equity Bank in Kenya targeted underbanked - Amadeo Giannini, founder of Bank of America had the same approach;

Build the technology from first principles rather than adapting any conventional practices. Tinkoff and Webank built their core platforms from scratch. Oaknorth focused on the credit model whilst utilising Mambu for their core banking;

Following on from no. 2 above, the technology approach is not one of a tech arms race towards the most advanced and complex tech stacks, rather the efficient use of available technology platforms to deliver your product to customers. Oaknorth focus on the lending platform whilst running on Mambu;

The technology play thereby leads to tech valuations rather than balance sheet business valuations - Critical in this is how you collect and grow your data to serve the business in the long run. Tesla is collecting 10x the volume of data on autonomous driving than all its competitors. This data advantage will lead to winner take all economics for Tesla in the automotive industry. Key question for neobanks is whether you will have data advantages in the long-term.

Build proprietary tech that can be sold on to other institutions - Tinkoff have their smart courier systems amongst others, Oaknorth have their credit model, Webank have their big data and analytics;

Adopt the attitude that you are primarily a tech company offering financial services. Tech companies are constantly updating their products and user experience. I shudder when I hear some bank managers call the IT department a “cost centre”.

Have a direct relationship with the customer and offer an exceptional experience that leads to referrals - referrals drive lower cost of acquisition over time;

Adding on to this line of thinking - the customer relationship should lead to cross-selling opportunities thereby increasing the customer long-term value. The long-term LTV/CAC ratio thus keeps getting better. A third of Tinkoff customers have more than one product;

Have a very solid commercial focus - one thing that is clear with Tinkoff, Oaknorth and Webank is their focus on profitability from day one. The commercial rigour underpinning these three organisations is a far cry from the scale at all costs mentality that we’ve witnessed with some other neobanks. Ultimately, banking is a serious business that requires customer trust - in the absence of VC money, some neobanks could face modern-day bank runs once it is clear that they cannot make profit;

Own the balance sheet - you need deposits. The ability to lend from deposits is the ultimate super-power in banking. Lending from capital requires specific hurdle rates that constrain your pricing power and make your business model extremely sensitive to credit risk. I think Neobanks that have a banking license will outperform those that “rent a charter”;

Despite all this, one of the major factors that we need to consider in Africa is the depth of our tech talent. Are we really part of the real technical innovation that is occurring at the bleeding edge of technology or do we know how to apply existing protocols to our situations? It will be difficult to execute at the level of a Webank given the disparity in technical expertise. To see this in action, the H-Index which is a proxy of the depth and quality of academic research in a specific field, shows that only South Africa is in the top 50 globally when it comes to computer science research. USA, China and other European countries dominate the top 10. How then can we build great tech when there is very little tech research going on in our countries?

Other Neobanks I like;

SoFi - Started off with student loans and now is expanding its product suite. Through acquisition of Galileo, it will also offer tech as a service thereby diversifying its revenue base;

Judo Bank - SME bank based in Australia - not yet profitable but showing impressive growth metrics;

Starling Bank - Yet to show sustained profitability but has already broken even. It is well managed and I like the CEO’s Anne Boden’s story

Nubank - Brazilian neobank that has significantly improved account onboarding thus growing to over 20 million customers - yet to achieve sustainable profitability but pace of growth and unit economics are remarkable;

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@gmail.com;

Follow on twitter @ https://twitter.com/SamoraKariuki

That's very true and an accurate observation. There is a threat that well financed start ups will have access to the best talent. Nonetheless on the bright side is that nowadays in the current ecosystem you can focus on your small niche and utilise best of breed third party software to support your business. In the example of Oak North, their mission was to build world class credit decisioning software and it made sense to get the best data scientists. For another neobank, maybe their focus will be on customer engagement and thus they need to build software for customer engagement and rely on third party software for their other services. Essentially nowadays the model seems to be that you should only build the software that is adding value to your business model rather than building everything from scratch.

Great post! Like you, I’m no techie, but I’m intrigued by the interactions between suggestions (2) build tech. from first principles; (3) rely on existing technology; and (5) build proprietary tech. for sale to other institutions.

What distinguishes companies that can (and want to) build the tech. from scratch from those that buy proprietary tech. produced elsewhere?

For example, you mention OakNorth recruiting from some of the world’s leading tech. Does innovation in this sector (e.g., “going to first principles”) typically require the highest levels of expertise? I worry that this may only be viable for the larger incumbents in traditional sectors or for well-financed start-ups.