#84 - The Corporate Foundry—Beyond Pizza-Box Innovation (Free to Read)

Turning institutional heft into intrapreneurial firepower - Moving from feel-good ‘Innovation of the Week’ rituals to disciplined ventures that confront the institutional imperative.

Illustrated by Mary Mogoi

Hi all - This is the 84th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

Reach out at samora@frontierfintech.io to discuss sponsorships, content partnerships and advisory work. To find out more about working with Frontier Fintech, click the link below.

Introduction

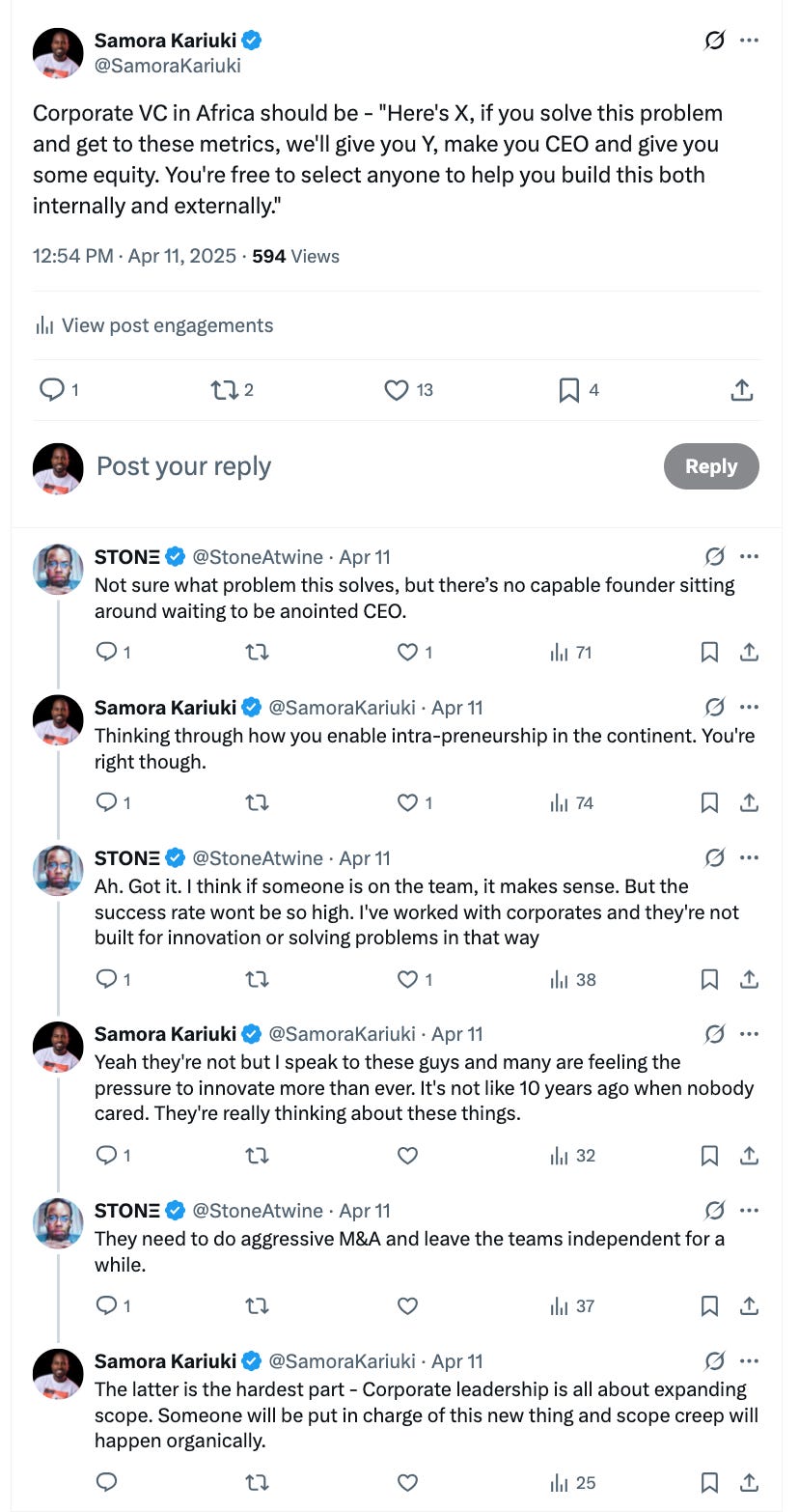

Some months back, I had an interesting X exchange with Stone Atwine. Stone is an OG in Pan-African Fintech, an experienced operator and also a thought leader in the broader entrepreneurial space. He is someone whose views I greatly respect. The exchange is below;

I was thinking aloud about how corporations can encourage internal innovation. Immediately, Stone made the point that no capable founders are sitting around waiting for things to happen. I then made the point that intra-preneurship or rather entrepreneurial efforts incubated within the bank may need such an approach. For Stone, his work with corporates had shown him that the success rates for such initiatives are extremely low and moreover, corporates are not built for innovation or solving problems in an entrepreneurial manner.

The truth is that outside tech incumbents such as Google or Microsoft, this is largely true. Even for the likes of Google or Microsoft, one can argue that a large chunk of their recent success stems from commercialising innovations through M&A or leveraging their existing strengths in distribution and commercialisation. The reason I made that X post in the first place was that I’d often see an internal tension in CEOs and leaders from corporates. Most people who make it to CEO are smart people and are clear in why innovation matters and how entrepreneurial efforts can aid their businesses. Nonetheless there's a massive chasm between insights and execution. My time at a mini-corporate I later came to realise gave me a distorted view of how corporates actually work. Finbank was a three man team between myself, the CEO and the Chairman. We’d make decisions over dinner and rubber stamp them at a board meeting. This combination of speed, trust and creative tension enabled us to do quite a lot within a short space of time.

Unfortunately, most corporates don’t work in such a lean fashion. They’re too big and too cumbersome. Nonetheless, they still face the competitive pressures that technology is causing and they have to think through how they can leverage their scale and capital to foster intrapreneurship. In this week’s article, I discuss why Intrapreneurship matters, Ping-An as the gold standard for intrapreneurship in financial services, why it’s so hard and what leaders should consider in their intrapreneurial efforts. Ultimately, the article validates Stone’s point of view which is informed from an intelligent conclusion. The intelligent conclusion is that Stone at core understands what it takes to get it right and understands that the incentives involved make it impossible for Corporates to execute.

Why Does Intrapreneurship Matter?

Last week I wrote about the role that African family wealth can play in not only incubating but scaling Fintech ventures. The underlying logic behind this article was that the intersection between Finance and Technology will continue to blur. Financial services traditionally has been one of the world's most profitable industries and one of the largest, it also has the largest surface area for technology based enhancements. How then, can we accelerate this intersection? Like family wealth, incumbents have capital and data, two critical elements to success.

I remember attending an investor briefing for Equity Group led by Dr. James Mwangi. In this session, he expertly detailed how the bank’s credit performance particularly at the SME and retail level was significantly affected by individual health outcomes. Sickness either leads to a high financial burden on the family or loss of work, this adversely affects people’s ability to repay their loans. He then went on to show how this insight is leading their efforts in not only insurance but also through their network of clinics across the country. This was a story of how a bank through seeding new businesses led by a new crop of leaders was solving problems that were adjacent to the core business. In essence, incumbents have access to primary data and particularly unique insights that can be leveraged to create new entities that are commercially viable. Equity is not only driving intrapreneurship but actively building ecosystems.

As Steve Jobs said, the best thinkers are doers. In essence, entrepreneurial inspiration often happens when the entrepreneur in question has sufficient exposure to the problem. In a broader context, intrapreneurship also matters for the following structural reasons;

Technology is changing the world, this much is true. Who would have imagined 5 years ago that Google’s search business would ever be under threat. Now, their search market share dropped below 90% for the first time in a decade. In an interview, Satya Nadella said that their wish with Open AI was to make the 800 pound Gorilla that is Google to come out and dance. They’ve achieved this objective. This matters because now every business model is in question. I’ve always argued that when things are changing so rapidly, the most important thing to do is to learn and experiment as quickly as possible. Intrapreneurship therefore becomes a long-term hedge against being disrupted.

Like in the family office example from last week, the core insight is that Africa, unlike China and the USA, is a capital constrained society. Incumbents therefore have the advantage of having not only capital but coordinated capital that can unlock long-term outcomes. This capital moreover not only comes with relationships with ecosystem players but also with regulators.

I spoke to Eric Muriuki, the CEO of Loop DFS about intrapreneurship and he shared a critical insight. For commercial success, alignment often matters more than speed. Because African incumbents already command large pools of patient capital, securing early alignment across boards, regulators and business heads turns that capital from a passive moat into an active launch-pad for new ventures.

Globally, the best model of Intrapreneurship comes from Ping An Group in China. Below we’ll analyse what they’ve been able to achieve and glean some insights from their journey. We’ll also look at a few other examples of Intrapreneurship.

Ping-An - The Ultimate Intrapreneurship Play

Ping An’s pivot from legacy insurer to technology ecosystem

Ping An opened in 1988 in the dusty port district of Shekou, Shenzhen. Founder Peter Ma Mingzhe, then a young manager at China Merchants, persuaded his bosses to back the country’s first joint-stock insurer. For a quarter-century the group grew by the textbook; selling life, motor and savings policies and reinvesting premiums. This continued until the Founder saw market share slipping to digital giants that offered payments and credit in a single tap. For context, Ping-An had been a pioneer on many fronts. In 1994, they welcomed JP Morgan and Goldman Sachs to their cap-table becoming the first financial services company in China to have foreign shareholders.

In 2013 Ma told his board the firm risked becoming “pipes beneath other people’s super-apps”. The growth of Alibaba and Tencent represented the threat, Ping-An had to be a technology company at core and Peter Ma realised that central to this was to have the tech talent and the technical infrastructure, particularly having your own cloud based architecture. He hired MIT-trained Jessica Tan as co-CEO, ring-fenced a US $1 billion cloud budget and instructed every division to launch data-centric ventures that would pull customers back to the group each day. Ping An now spends at least one per cent of annual revenue (10% of profit) on R&D, employs twenty-four thousand engineers and runs seven research institutes.

Under Ma and Tan’s vision, Ping An adopted a “Finance + Technology” and “Finance + Ecosystem” strategy, aiming to serve customers’ broad lifestyle needs (healthcare, housing, autos, etc.) beyond traditional insurance. This meant building or acquiring businesses in five key ecosystems; financial services, healthcare, automotive, real estate, and smart city services. These were all linked by technology and data. Ping An explicitly set a goal in 2008 to transform from a financial institution into a technology company, and aligned its mission accordingly.

The flagship intrapreneurial stories that followed; OneConnect, Lufax, Ping An Good Doctor and Autohome explain why the group’s market value quadrupled between 2013 and 2020 and why more than 74 million users now hold products from more than one Ping An business.

OneConnect - The internal toolkit that became China’s default fintech plumber

OneConnect began as a toolkit that repackaged the cloud, AI and blockchain code Ping An had built for its own operations into plug-and-play services that external banks and insurers can rent, from e-KYC and smart risk engines to full core-bank platforms. Early critics saw it as little more than captive revenue, and the numbers lent weight to that view because Ping An still generated 56 percent of OneConnect’s turnover in the third quarter of 2023 . Management insists the mix is shifting; by the third quarter of 2024 business from overseas clients accounted for 23 percent of revenue, seven points higher than a year earlier.

OneConnect Booth - Source

Lockdowns during Covid closed branches and forced lenders to move customer onboarding online, and demand for OneConnect’s facial-recognition KYC and remote-lending portals surged. Tan Bin Ru, who heads the Southeast Asia business, called the period a “hyper acceleration of digital adoption” among banks that had been sitting on the fence . By mid-2020 the platform was embedded with every major national bank in China, 99 percent of city commercial banks and 53 percent of insurers.

As of the third quarter of 2024 it also served 192 financial institutions in more than twenty overseas markets, including the top three ASEAN regional banks and two of the world’s ten largest insurers; it has backed digital-bank licence bids in Singapore, Malaysia and the Philippines and, with the Brazilian firm Pismo, rolled out a bank-in-a-box stack known as OneCosmo. OneConnect listed on the New York Stock Exchange in 2019 at a valuation of about US$ 7 billion after SoftBank’s Vision Fund had injected 650 million dollars, bringing external scrutiny and signalling Ping An’s readiness to share upside with outside investors .

Lufax - from peer-to-peer lender to regulated wealth hub

Lufax began life in 2011 as an online marketplace that matched small borrowers shut out of the state-bank system with retail savers hunting for yield, using Ping An’s data and risk models to price credit in near real time. By 2018 the platform had amassed more than forty million users and ridden China’s peer-to-peer lending boom to the top of the global fintech league tables, yet it faced extinction when regulators cracked down on the sector. Because Lufax sat at arm’s length with its own board chaired by American banker Gregory Gibb, it pivoted quickly, winding down the P2P book, securing consumer-finance licences and repositioning itself as a regulated wealth-and-SME-lending hub.

Private investors had already validated the idea by injecting US $1.2 billion in 2016, and the October 2020 New York IPO, which raised US $2.4 billion at a US $33 billion valuation, brought even tighter public-market scrutiny while keeping Ping An the majority owner.

Ping An Good Doctor - Healthcare as the new front door to finance

Ping An Good Doctor was launched in 2014 to solve China’s chronic shortage of convenient primary care by blending an AI symptom-checker with a 24-hour panel of physicians and drug-delivery logistics. Rapid word of mouth and the smartphone boom pushed registered users to 228 million by 2018, with daily consultations topping half a million; the Covid lockdowns then lifted the base past 400 million as tele-medicine became a necessity.

A Ping-An Good Doctor Vending Machine in 2018 - Source

The app raised US $1.1 billion in its 2018 Hong Kong listing, funding offline clinic partnerships, chronic-disease programmes and a health-insurance marketplace that loops users back into Ping An’s core. After nearly a decade of investment subsidies Good Doctor recorded its first full-year net profit in 2024, helped by a 17 percent rise in enterprise and integrated-finance revenue that showed cross-sell synergies were finally paying off.

Autohome - Data flywheel for auto loans and insurance

Autohome, China’s most-visited online car marketplace, entered the Ping An orbit through acquisition rather than incubation: the group bought Telstra’s 47 percent stake for US $1.6 billion in 2016 and kept the company public to preserve founder agility. Under Ping An’s wing Autohome integrated AI price engines, livestream vehicle launches and dealer leads with instant loan pre-approvals from Ping An Bank and same-screen motor-insurance quotes from Ping An P&C.

The portal averaged 77.5 million daily active mobile users in December 2024, up 14 percent year-on-year, converting car research sessions directly into credit-card issuance, auto loans and policy sales that feed the wider ecosystem’s revenue flywheel.

Lessons from Ping-An

Ping-An is arguably the most successful example of Intrapreneurship in Financial services. You’d be hard pressed to find an example of a finance company that has not only transformed its core business but generated so much market value from its internal intrapreneurship efforts. Its critical to understand what some of the core drivers of this success. I list and explain some key ones below;

Leadership - It all starts with leadership. Peter Ma not only had the foresight to understand that technology was changing the world, he also had the boldness to act on it. Satya Nadella often talks about having a complete thought in the context of incumbents scaling technology. What this means is that if you think that A is true, then map out all the consequences of A being true and act on the most logical outcomes if A is true. Simply, if technology companies like Alibaba and Tencent were going to move insurers and banks into back-office plumbing, then either you become back office insurance companies or you build Tencent-like capabilities that speak directly to the consumer. If this is true, then you have to make the radical decisions to onboard talent, build your infrastructure and commit to this goal. What happens in a lot of cases is incomplete thought. Your logical conclusion is accurate but the steps that you take next are driven by sub-optimal accommodations. This is often driven by either fear or a lack of alignment. The latter occurs when you cannot get full buy in from shareholders, a situation that hampers innovation in most incumbent banks. The core of your shareholders are concerned with risk and dividends making disruption unpalatable. It’s perhaps why long-tenured CEOs like James Mwangi of Equity, Abubakar Suleiman of Sterling Bank (Been in Sterling bank since 2003) and previously Isaac Awuondo at CBA achieved success in this regard.

Financial Structure - Tied to the idea of a complete thought, Ping-An structured its intrapreneurial efforts based on the three concepts of incentivising managers, having patience and institutionalising market discipline. What this meant was that;

Ping-An invested billions in their internal efforts without any immediate pressure for results;

In as much as it was patient, it also had a “fail-fast” approach with executives quickly pulling the plug on ventures that weren’t making sense;

It incentivised managers by giving equity-upside through stock options given that eventually these intrapreneurial efforts would be spun-off to create stand-alone entities like One Connect.

To tie everything together, Ping An leveraged external capital such as Softbank investing in OneConnect to not only create market discipline but also tap into additional capital rather than use its own exclusively.

Talent - Ma Mingzhe understood that the great technology companies in China were not just about infrastructure but about people. Tech companies are fundamentally about talent, there’s simply no other point of leverage than talent. Ping An recruited global talent to run these new ventures and the central insurance business. Not only that, Ping An went further by ensuring that leaders could move freely between entities to exchange learnings and provide leadership.

Ecosystem - Ma’s team refused to settle for a slicker insurance app; they set out to own the customer’s whole day. If Alibaba could sit at the center of commerce and Tencent at the center of social life, Ping An wanted to be the operating system for money, health and mobility. That logic reframed every product meeting: the question stopped being “How do we sell another policy?” and became “How do we solve the next problem our user will face after closing this app?”. The answer was to stitch together finance, tele-medicine, auto buying, real-estate tools and smart-city services into a single sign-on universe. Free doctor chats and car-price engines acted as magnets, dropping acquisition cost and generating the high-frequency data streams that make risk models smarter and cross-sell easier. Because value now flowed in every direction; insurance boosted Good Doctor usage, Autohome fed loan demand and each new node increased the network’s pull. Incumbent banks that stop at digitizing a savings account never enter this flywheel; they stay trapped in a product silo competing on rates while platforms like Ping An compete on time and relevance. In short, the battlefield has shifted from single-industry share to ecosystem share, and the players who ignore that shift will wake up renting space in someone else’s customer journey. This is the core idea behind becoming an ecosystem player and is tied to the idea of having a complete thought in business.

Other factors include;

Working together with regulators from the inception of their products;

Investing heavily in tech infrastructure;

Organisational structure and autonomy with each effort having its own P&L and in most cases, procurement systems. The latter is often a massive latent barrier to the speed that such internal efforts need;

Other Examples of Intrapreneurship

Yape CEO Raimundo Morales - Source

Peru’s Yape shows how a fee-free mobile wallet, launched in 2016 for the country’s unbanked, could scale to 17 million users and two million merchants by 2024 once Banco de Crédito rewired 4 000 staff into agile squads and accepted short-term fee cannibalisation.

Kenya’s M-Pesa, born in 2007 as a two-person SMS pilot, now moves 20 billion transactions a year, nearly 60 percent of national GDP thanks to an agent network, a single “send-money-home” use case, and regulators willing to let telecom innovators run ahead of banks.

South Africa’s First National Bank turned its workforce into a venture pipeline with an internal idea market that has rewarded staff with R54.5 million and produced eWallet and other products via 48-hour CodeFest hackathons.

Outside finance, Sony’s PlayStation emerged when CEO Norio Ohga protected engineer Ken Kutaragi’s skunk-works console, which within four years generated 40 percent of Sony’s profits, while 3M’s Post-it Note grew from Spencer Silver’s “failed” adhesive and six years of patient sampling before becoming a billion-dollar office staple; proof that executive sponsorship, ring-fenced autonomy and tolerance for trial can turn fringe ideas into core businesses.

Why is it So Difficult to Pull-Off?

My most surprising discovery: the overwhelming importance in business of an unseen force that we might call "the institutional imperative." In business school, I was given no hint of the imperative's existence and I did not intuitively understand it when I entered the business world. I thought then that decent, intelligent, and experienced managers would automatically make rational business decisions. But I learned over time that isn't so. Instead, rationality frequently wilts when the institutional imperative comes into play.

For example: (1) As if governed by Newton's First Law of Motion, an institution will resist any change in its current direction; (2) Just as work expands to fill available time, corporate projects or acquisitions will materialize to soak up available funds; (3) Any business craving of the leader, however foolish, will be quickly supported by detailed rate-of-return and strategic studies prepared by his troops; and (4) The behavior of peer companies, whether they are expanding, acquiring, setting executive compensation or whatever, will be mindlessly imitated.

Institutional dynamics, not venality or stupidity, set businesses on these courses, which are too often misguided. After making some expensive mistakes because I ignored the power of the imperative, I have tried to organize and manage Berkshire in ways that minimize its influence. Furthermore, Charlie and I have attempted to concentrate our investments in companies that appear alert to the problem.

This quote from Warren Buffett in his 1989 annual letter to shareholders is imprinted in my brain. After over a decade in leadership roles, I’ve come to appreciate it even more. It’s the foundational reason why a lot of things that make sense don’t get done in large organisations. Importantly, it explains why money is often wasted on white elephant projects and why innovation seems so difficult for such organisations. This institutional imperative often leads to the following issues;

Scope Creep and the Managerial Imperative - Just like corporate projects will materialise to soak up available funds, managers will increase scope to expand managerial relevance. Charlie Munger has often said that people often underestimate how far a simple idea can go. Unfortunately, corporate managers have the imperative to maximise scope and minimise focus not only for themselves but for the projects they undertake. A simple send money app will be converted into a complex behemoth of a project because this in the manager’s psychology justifies the high salary, high project budget and therefore increases the sunk-cost fallacy. In turn, the manager feels that his job is more secure. At a broader level, this makes intrapreneurship impossible. Success at the start requires a small team that is hyper-focused on one thing. Jeff Bezos enforced this at Amazon by having pizza-size teams. Start small and limit scope.

Innovation Theatre - Given that intrapreneurship is structurally difficult due to the above, large incumbents retreat into innovation theatre through hackathons and mis-guided accelerators to signal innovation without any of the structural factors that enable true success.

Jealousy and Bureaucracy - Often people use their intellectual selves to understand phenomena and fail to see the role of our more basic instincts. For instance, imagine how a HR Head who earns say US$ 15,000 at a large bank would feel signing off on a comp package that would see a 25 year old kid “who could be my son” potentially earn a life-changing sum? All sorts of excuses would be given into why we can’t adopt such a recruitment strategy using terms like “staff harmony” and “what our existing policy says”. Don’t underestimate this institutional imperative. Additionally, imagine how a procurement director would feel if this new team could work externally of the company’s procurement policy? “What if people learn that you can actually save costs and reduce wastage if there were proper incentives as opposed to my byzantine procurement system?”

Outside of the institutional imperative, the following forces also hinder Intrapreneurship;

Linear vs Non-Linear Thinking - In Africa and many parts of the world, corporate execs have been trained to think of wealth in a linear manner i.e. focus on increasing salary over time and grow wealth through saving and investing that salary. This has worked for a long time particularly for the Baby Boomer and part of the Gen X generation. For someone who thinks of wealth in such a linear fashion, the idea of risking this progression for a low probability shot of 100x your salary doesn’t make sense. The people who understand wealth as a non-linear endeavour may have left their jobs already.

Entrepreneurship Today - In today’s world, the barriers to entrepreneurship particularly in Fintech are not as high as they were a generation ago. Today, entrepreneurs benefit from the following;

With less than US$ 1,000, you can incorporate a Delaware C-Corp and start raising money immediately;

Africa now receives billions of dollars annually in start-up funding meaning that the capital exists to support a determined founder;

AI is making access to knowledge and intelligence ubiquitous. A founder can have agents at the very beginning that help with legal documentation, product research and coding support.

Paradoxically, the cheaper it becomes to launch an independent start-up, the less of an edge a corporate venture gains from its in-house capital and infrastructure. So falling external barriers make intrapreneurship relatively less attractive even as entrepreneurship overall gets easier.

The forces that work to either block or bastardise intrapreneurial efforts are often very powerful. No wonder Warren Buffett noted that “rationality frequently wilts when the institutional imperative comes into play”.

What Can Leaders Do?

The lessons are all imbued in both the Ping-An story and the challenges with the institutional imperative. It’s all about understanding this imperative and working against it. It’s easier said than done nonetheless. Whilst I can’t say that this is what leaders should do, I think what’s more important is, what are the core considerations when it comes to Intrapreneurship?

Talent matters - optimise for getting the right talent on board and that means;

Expanding the type of talent that you get into the company and enabling different types of people to thrive;

Having cross-functional leadership execs that don’t have rigid roles but rather can move freely across projects to support teams;

There’s nothing like over-communicating - especially to shareholders. Banco de Credito Peru (BCP) shared data about Yape to external investors even when Yape was losing money. This not only drove further buy-in from investors it also created external discipline that can often be a great counterweight to internal delusion;

I like the idea of bringing in external capital to enable market based discipline. This means that internal efforts should have separate P&Ls and be able to raise funds externally;

CEO’s and Chairmen should focus on having complete thoughts and have the courage to follow through

What’s clear is that Intrapreneurship is extremely difficult. BCG in a report showed that over 70% of digital transformation projects fail. Once you understand the complexity of successful Intrapreneurship, it becomes clear why Stone was clear in his skepticism of intrapreneurship. Too much has to go right in an environment in which the institutional imperative is exceedingly strong.

Nonetheless, as we argued last week, Car and General is generating significant revenues from Watu Credit. Moreover, Moniepoint and OmniRetail are now generating revenues that would make the likes of Seplatts and Flour Mills of Nigeria take notice. A lot of success in Finance is being achieved outside of incumbent institutions and now more than ever, leaders need to think about sowing the seeds for such entrepreneurial success internally.