#83 - It's a Family Affair - Generational Wealth Meets Fintech

Positioning African family capital as a structural enabler of fintech growth, why it matters, playbooks and global case studies.

Illustrated by Mary Mogoi

Hi all - This is the 83rd edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

Reach out at samora@frontierfintech.io to discuss sponsorships, content partnerships and advisory work. To find out more about Partner Content, click the link below.

Introduction

Two years ago, the rivalry between two of Nigeria’s largest conglomerates, led by two of Africa’s richest men was laid bare in a series of explosive editorials. It started when Dangote in a 7-page editorial accused BUA group led by Abdul Samad Rabiu of a number of economic crimes. The Dangote editorial is hard to come by but the gist of the allegations can be found here. Thereafter, the BUA group published its own editorial responding to Dangote. It was a throwback to 90s hip-hop diss tracks. The editorials were fascinating because they revealed in my own view, what it takes to be an African billionaire. BUA made some interesting observations, I cant validate the accuracy of these claims, I just found them interesting;

In the mid 90s, the BUA group wanted to set up a Sugar Factory, they approached the late Usman Dantata, an uncle of Aliko Dangote to lease a 4.5 hectare waterfront property on which they’d build their factory. According to BUA, Aliko Dangote waited until the contractors were on site before he approached then President Obasanjo to revoke the land. Not only was the land revoked, the lease was handed over to Dangote, the late Dantata lost the land entirely. Interestingly, it took time for Bua to find another property, in this case a piece of land that their late father Isyaku Rabiu donated to them. The story was that he saw the pain that Abdul Samad Rabiu was going through and gave them the land.

Over a decade later, they came across another issue. BUA was one of the few companies granted a license to build a cement plant. They decided on a floating terminal as a stop-gap measure as they built out an entire factory. After facing resistance from unknown forces to dock the floating terminal in Lagos, they decided to move it to a terminal they already owned at Port Hartcourt. Even with this, they faced intensive pushback and it only took the intervention of the late President Yar Adua who directed the Minister of Transport to intervene in BUA’s favour;

The cement drama didn’t end there. A certain Orwell Brown, a Comptroller General, launched a sudden strike attempting to deport BUA’s entire expatriate crew. The crew were rounded up and even put on an Emirates flight to Asia, all on a Friday evening when the government was effectively off for the weekend. Again, it took the intervention of Tanimi Yakubu, the then Chief Economic Advisor to the president to intervene. The crew got off the plane and were driven back to their quarters.

Abdul Samad Rabiu on the left and Aliko Dangote on the right - Source The Cable

He continued to list a number of alleged malpractices including the hiring of thugs to sow chaos at BUA’s factories. Whilst all this is intriguing, a few factors caught my eye about the reality of doing business in Africa. In fact, I remember sharing this with my former colleague Felix and telling him to strap up for the ride if the business was to scale to where we wanted it to. Some facts popped up;

Despite the “beef” between the two families, Rabiu could still strike a deal with Usman Dantata to lease land showing a weird cooperation amongst Africa’s elites. The question then becomes whether Dangote would cause his uncle to lose land or whether this was orchestrated internally, showing the level of skullduggery required to be Africa’s richest;

Rabiu despite his troubles still had his fathers land to fall back on showing the depth of inter-generational economic resilience needed to make it to billionaire level in some instances. You need strong familial ties;

In all their troubles, Rabiu and the BUA group not only had access to networks, but they knew how to use these networks. He could intervene directly at the presidential level in the case of his floating terminal and his call with the late President Yar Adua. He also knew that in the instance of having his expat staff bundled into a plane, the Economic Advisor Yakubu was the right person to call.

In all this, family wealth and business plays a key role in African Business. Orwell Brown, the Comptroller general, was in fact married to a key executive at Dangote. Moreover, both BUA and Dangote are effectively massive family businesses, as are many others in the continent.

The power of networks is something that Bill Gates alluded to in a conversation with Dangote that was posted on YouTube. In the conversation, Bill said this;

I'd be showing Aliko my charts about hey Sokoto has a pretty low vaccination rate, you know and Kano needs to do this and in Aliko he really knows people he has relationships he's willing to reach out to people. So he'd say let's call the governor you know, we'll talk about this and sure enough we've got the governor of Sokoto on the phone. We're talking about this and so this ability to reach out to draw on the broad relationships that Aliko’s developed. I'm pretty shy about calling people. I just want to mail them my facts but in fact what's come out of that is that Aliko and I do video conference calls with six of the governors in the northern states where twice a year we look at vaccine coverage. You know, is the supply chain working? or the workers showing up? or the health care posts in the right locations and it's a big challenge but really drawing on Aliko’s communication skills and the fact that he's not afraid to call anyone everybody wants to talk to him.

I’m sure some of you are wondering, what does this have to do with Fintech in Africa? The core point is that Fintech businesses need to take that next leap into becoming economic giants and there are lessons to be learned from the existing giants. Importantly, how can we leverage the wealth, networks and influence that existing large family networks have in incubating large Fintech businesses. This is something that occupies my mind a lot. In this article, we’ll go through some of the fundamental issues that VC funding has in Africa despite some of the positives, why Fintechs matter for African family businesses, the scale of wealth in Africa and some of the structural factors that will make it grow, the challenges of marrying family wealth to Fintech innovation and how some of these challenges can be dealt with, some playbooks for how we can make this work and some global examples of Fintechs that have thrived based on leveraging family wealth and networks.

VCs in Africa

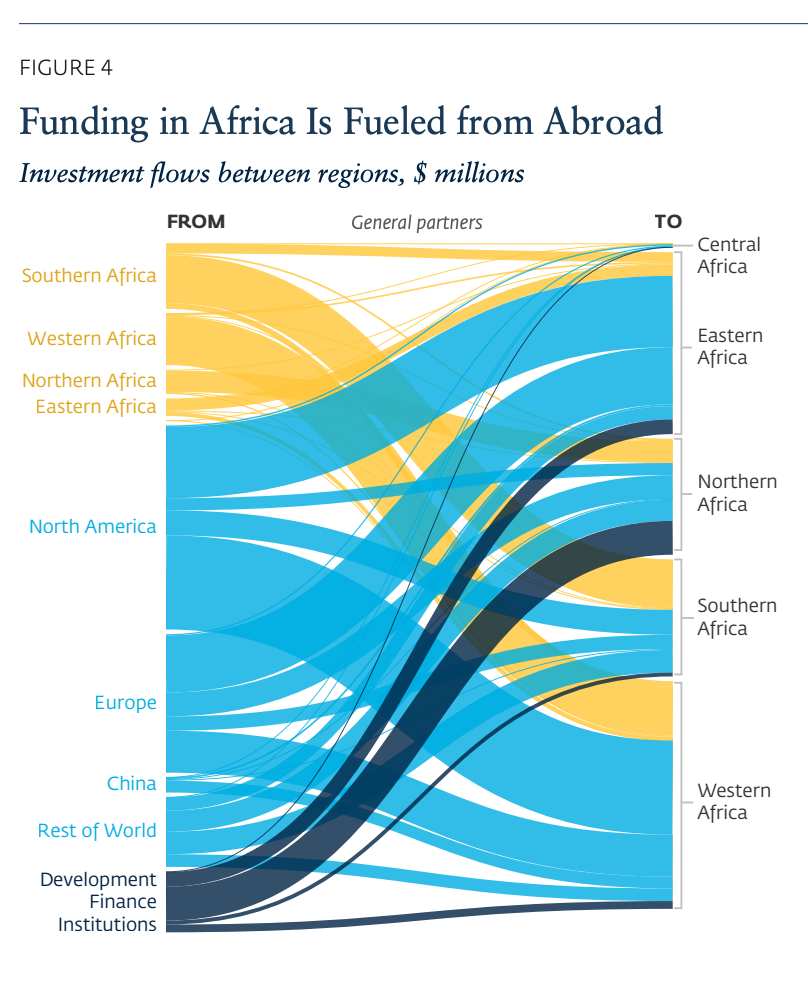

IFC in an exceptional report about Fintech funding in Africa produced the diagram above. It shows where the money into African tech comes from and how it flows. It’s clear that the lion's share of African funding comes from the rest of the world with North America and Europe playing a massive role. There are slight regional variations. In Southern Africa and West Africa in particular, local capital plays a larger role in funding start-ups. In East Africa, the local capital plays a much smaller role. It potentially speaks to why West Africa and South Africa have outsized contribution to the unicorn outcomes in the continent.

Whilst it's easy to bash VC in Africa, I think it has a role to play in at the very least catalysing the ecosystem. Simply, some founders would have never dared to dream had western VC capital not found its way into the continent. It has catalysed the ecosystem and created valid outcomes such as enabling the likes of Flutterwave to even exist in the first place. Nonetheless, it does have some challenges;

A lot of western VC by design doesn’t come with the kind of connections and on-ground support that they have in SF. You then have VCs that have local partners but global money, again, whilst this is better than nothing, a number of these partners don’t have the gravitas to make the Central Bank governor spend the afternoon with a founder. Simply, a lot of capital doesn’t come with any extra help often making founders flounder in a world where connections matter more than capital. I’ve witnessed this first-hand.

The VC model is built for quick growth, a scale at all costs model based on short-fund cycles that last between 5-7 years. In Fintech, this manifests in funding business models that promise quick scale. This explains the over-indexing on payments companies, crypto and now stable-coin powered cross-border payments. Unfortunately, a lot of these business models promise scale but often they don’t come with sustainable and differentiated economics. In my view you can draw a line between this and the lack of IPOs. VCs comfort themselves with the idea of secondaries, but if an IPO is the true acid test, then the idea of secondaries is at worst an extension of the greater fool theory.

Fickle Capital - During the 2023 down-turn, not only did the volume of capital flowing into fall by 46%, the number of active investors was slashed by over a half. If you compare this to traditional industry such as banks, the largest banks in Africa are African and are not going anywhere despite the vicissitudes that Africa throws at you. Ultimately, the key component of compound growth is consistency. As Warren Buffett reminds us “anything multiplied by zero is zero”. Such downturns really kill momentum.

The outcome of all these is that founders building business models that require patient capital or are solving hard facts don’t get the funding that’s needed. It creates a situation where like lemmings, founders are chasing the same problem. Clearly an unsustainable long-term dynamic.

Yes, But Why Should African Families Care?

Whilst all this is true, the question then becomes why high net-worth African families should care. Besides, they are running profitable operations and can benefit from growth through either Pan-African expansion like Dangote in Ethiopia and Zambia. Such moves fit within their circles of competencies and benefit from their existing heritage of execution across either industrial businesses, traditional finance like banks or wholesale and retail trade. Why would you bother with Fintech? I think the points below give a good grounding;

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.