#80 - How to Select a Fintech Market in Africa Part 2 - Rest of Africa

Looking beyond the Big 4 Markets of Nigeria, Egypt, Kenya and SA, how should investors and operators think about the Rest of Africa?

Illustrated by Mary Mogoi

Hi all - This is the 80th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

Reach out at samora@frontierfintech.io for sponsorships, partner pieces and advisory work. Spaces are becoming limited on my advisory hours. I help clients with market entry, market mapping, strategic insights, sounding board to founders and general advisory across Pan-African Fintech.

Sponsored by Triage

Built by Executives

In Africa’s financial services sector, niche expertise in areas like risk, credit, compliance, and technology can make or break a company’s performance. Navigating complex regulations and integrating new technologies demand leaders who understand the nuances of financial products, stakeholder expectations, and market realities. Without this depth of knowledge, even well-funded institutions risk costly missteps that unsettle investors, stall growth, and undermine customer trust.

Triage brings a mix of hands-on experience as operators in banking and financial services, and global experience working with some of the largest financial services businesses in the world. Our team has worked with senior leaders in over 35 countries across Africa supporting a range of growth and change strategies across a spectrum of clients, from early-stage ventures to scale ups, to digital transformations and turnarounds. This broad experience enables us to spot the difference between passing expertise and genuine capability, ensuring you engage leaders who truly understand what it takes to succeed in the quickly evolving world of financial services.

Introduction

I recently had coffee with someone I greatly respect in the Fintech industry and we were discussing international expansion. One of the things that came up is how Fintechs should look beyond the Big 4 markets of Egypt, Kenya, South Africa and Nigeria when expanding due to the complexity of these markets particularly when it comes to coming up against formidable competitors. In her view, it makes sense to look beyond these markets as it minimises expansion and M&A risks. Interestingly, just last week, one of my subscribers Jesse asked why I always focus on the Big 4 markets, to be honest I gave a very hand-wavey response about these being the biggest markets. I should definitely look beyond these markets.

To this end, I decided to revisit the “How to Select a Fintech Market” post, one of my most lucrative posts from an incremental revenue perspective. In this post, I looked at the five largest Fintech markets in Africa from a perspective of raised VC dollars; Nigeria, South Africa, Kenya, Egypt and Ghana. The idea was to look at different factors and come up with some insights as to why these markets differ when it comes to Fintech success and particularly why some Fintech models work in one market whilst failing in others. The insights from the article validated why Nigeria and Egypt are the largest Fintech opportunities in the continent. Using a multiplicative approach, we showed how these two markets stand out. One of the core factors was that both markets have taken a bank-led approach to Financial Inclusion leading to a massive gap in access that Fintechs have swooped in to solve.

Can we extend this analysis to the rest of Africa? The answer is yes, but it requires a different approach. In the previous analysis, that these markets were viable was already assumed and therefore we didn’t dwell on things like market size and talent. To make an extended analysis work, you can’t assume market viability. In this week’s article, I look at 6 countries from the rest of Africa. They are; Ethiopia, Uganda, Tanzania, Ivory Coast, Senegal and the Democratic Republic of Congo. We analyse them based on the core question of “does this country have the core elements necessary for Fintech success?”. The results validated what the market has already proven out which is that Francophone Africa is a sleeping giant from a Fintech perspective. That the Big 4 markets only account for 40% of Africa’s GDP but over 83% of funding is proof that some of these markets are ripe for growth.

Why does it Matter

According to data from Africa the Big Deal, Africa attracted US$ 2.2 billion worth of VC dollars. Of this, the big four countries of Kenya, Egypt, South Africa and Nigeria attracted over 80% of the total funding with Kenya leading the pack with US$ 638 million. Whilst these four countries dominate VC, they only represent 41% of the total GDP of the continent. In fact, Kenya tends to overshoot from a VC perspective as it accounts for less than 5% of the continents GDP whilst accounting for almost 25% of total VC funding raised. Simply, investors and companies may need to look beyond the big four for both investments and expansion.

A new generation of Pan-African company is emerging. Whereas 20 years ago, it was the MTN’s and Vodacom’s that were expanding; now it’s the Flutterwave’s, Paystack’s, Wave’s and Moniepoint’s that are expanding beyond their home bases. It may be natural to think of expansion within the context of the big four countries i.e. if you’re in Nigeria, the next market should be either South Africa, Egypt or Kenya. Nonetheless, this may not necessarily be the smartest move. If you look at the big banks of the previous generation e.g. GT Bank, Equity and Access, in many cases started their expansion journeys by looking within the region. Only later, once they had perfected their M&A playbooks did they expand to other big four markets. One argument could be that you expand to a smaller market where the probability of success is much higher and repeat this until you have the success to warrant a riskier bet. Another argument could be that some of these big four markets could be overhyped from a return perspective.

For investors, a focus on the big four may come at the expense of interesting opportunities in the rest of the continent. VC is a very sentiment driven industry. At the early stage, there’s little if any fundamental analysis and rightly so because you’re taking a bet on an idea and founder. Nonetheless, at a macro level, what happens is that it represents the stereotypical beauty pageant example that Keynes gave.

Keynes brilliantly captured the essence of financial markets through his beauty contest analogy. In his 1936 work "The General Theory of Employment, Interest and Money," he compared investing to the newspaper contests of his day where readers chose the prettiest faces from a hundred photographs. The twist, Keynes observed, wasn't that participants selected based on personal aesthetic judgment, but rather anticipated which faces the average opinion would deem most beautiful. This creates a recursive psychological game where investors don't focus on a company's fundamental value but instead try to predict what other investors will think, and what those investors believe others will think, creating layers of speculation removed from economic reality. This self-referential dynamic may explain the over-indexing on a few African markets. Given that VC especially at the early stage represents this dynamic of guessing the average opinion of other investors, the non-big four markets may be ignored based on the correct but misplaced judgement that other investors will ignore these markets.

It therefore makes sense to highlight these markets and develop frameworks removed from hand-wavy logic that can give insight into how both operators and investors should pursue non-big four markets.

Approach

The Countries

To select countries for this series, I simply looked at two criteria; Is the country amongst Africa’s top 20 economies by GDP and does it have a history of start-ups and VC investment even if nascent? Are there any notable VC funded companies that have emerged from this country? Moreover, I focused on Sub-Saharan Africa.

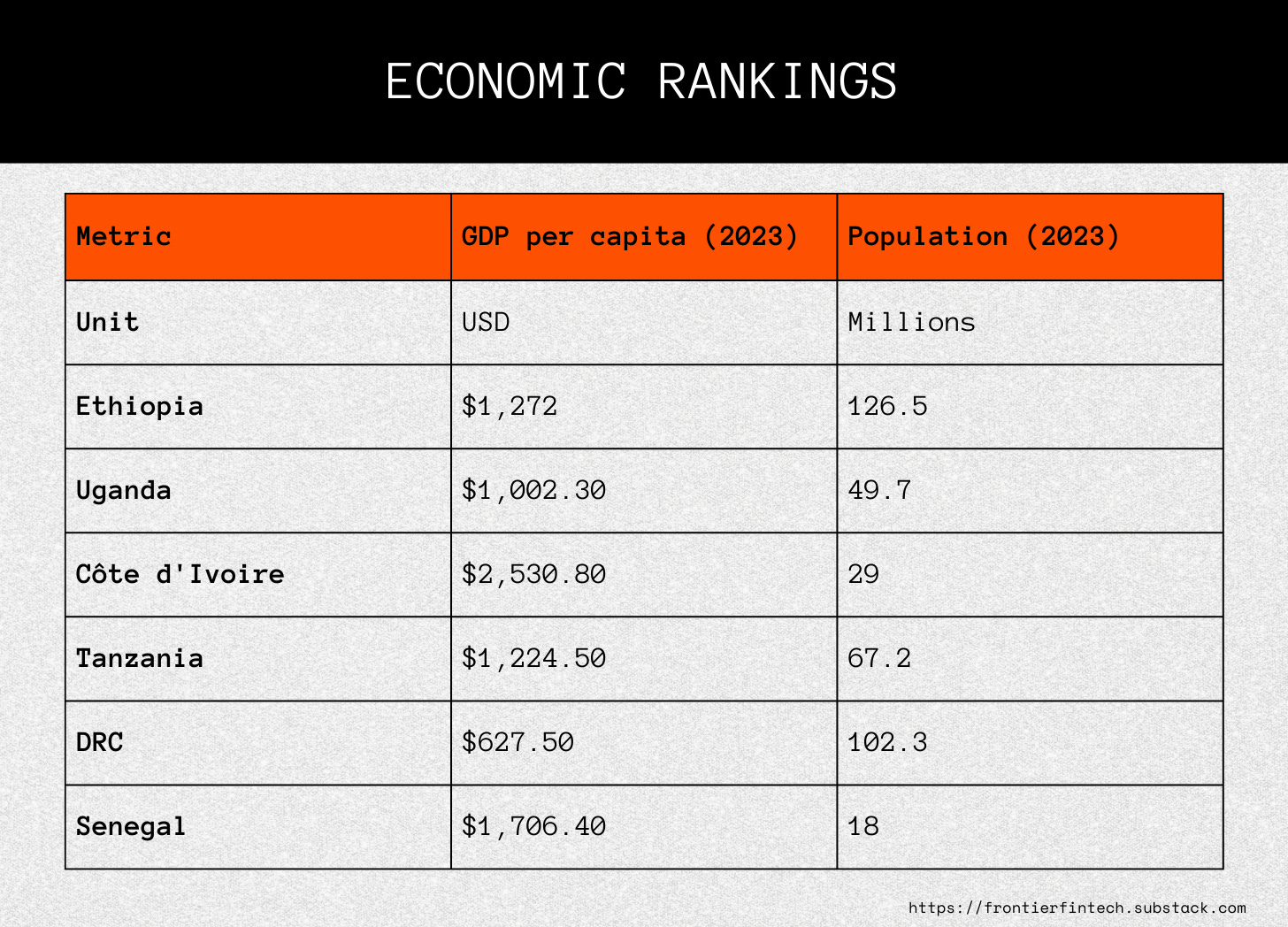

🇪🇹 Ethiopia - A landlocked country in the Horn of Africa with a GDP of US$ 120.9 billion, a population in excess of 125 million and a GDP per Capita of US$ 1,108. Ethiopia has been growing fast over the decades, experienced wobbles due to conflict and economic mismanagement and is now going through significant economic reforms that include opening up its capital markets and liberalising the exchange rate;

🇨🇮 Ivory Coast (Côte d'Ivoire) - A coastal country in West Africa with a GDP of US$ 94.5 billion, a population of around 32.9 million, and a GDP per Capita of US$ 2,900. Ivory Coast has been one of West Africa’s fastest-growing economies, benefiting from political stability, agricultural exports like cocoa, and increasing investments in infrastructure and energy;

🇸🇳 Senegal - A coastal country in West Africa with a GDP of US$ 35.7 billion, a population of around 19.2 million, and a GDP per Capita of US$ 1,911. Senegal has maintained strong and steady economic growth, underpinned by major investments in oil and gas projects, infrastructure development, and a relatively stable political environment.

🇹🇿 Tanzania - An East African country with a long Indian Ocean coastline, Tanzania has a GDP of US$ 85.5 billion, a population of over 67 million, and a GDP per Capita of US$ 1,270. The country has enjoyed consistent economic growth driven by mining, agriculture, and services, although challenges around business environment reforms and access to capital persist.

🇺🇬 Uganda - A landlocked country in East Africa with a GDP of US$ 62.9 billion, a population of about 48 million, and a GDP per Capita of US$ 1,300. Uganda’s economy has been growing steadily, supported by strong agriculture and service sectors, with future growth prospects boosted by oil discoveries and anticipated production.

🇨🇩 Democratic Republic of the Congo (DRC) - A vast Central African country with limited Atlantic coastline access, the DRC has a GDP of US$ 79.2 billion, a population exceeding 111 million, and a GDP per Capita of US$ 743. Despite being rich in natural resources, the DRC has historically faced political instability and underinvestment, though recent reforms aim to improve governance and attract foreign investment.

All these countries have robust economies, are attracting investments and have sizeable enough populations to support consumer Fintech. The idea is then to create a framework that enables someone to distinguish between them and filter out which are the top markets to invest or expand into.

The Ranking Mechanism

In our previous article, we used a simple analysis where we looked at FX Controls, Depth of Banking Infrastructure, Rate of Urbanisation and Mobile Money Penetration. This worked because other factors such as political stability and talent density were assumed. When it comes to other markets, it makes sense to be slightly more rigorous and look beyond basic infrastructure and market dynamics. I looked at these countries based on a number of criteria I will detail below. The idea was to normalise all these rankings from a scale of 1-5 and as always multiply the results to determine which is the best market. As we always argue, factors work in a multiplicative and not additive manner.

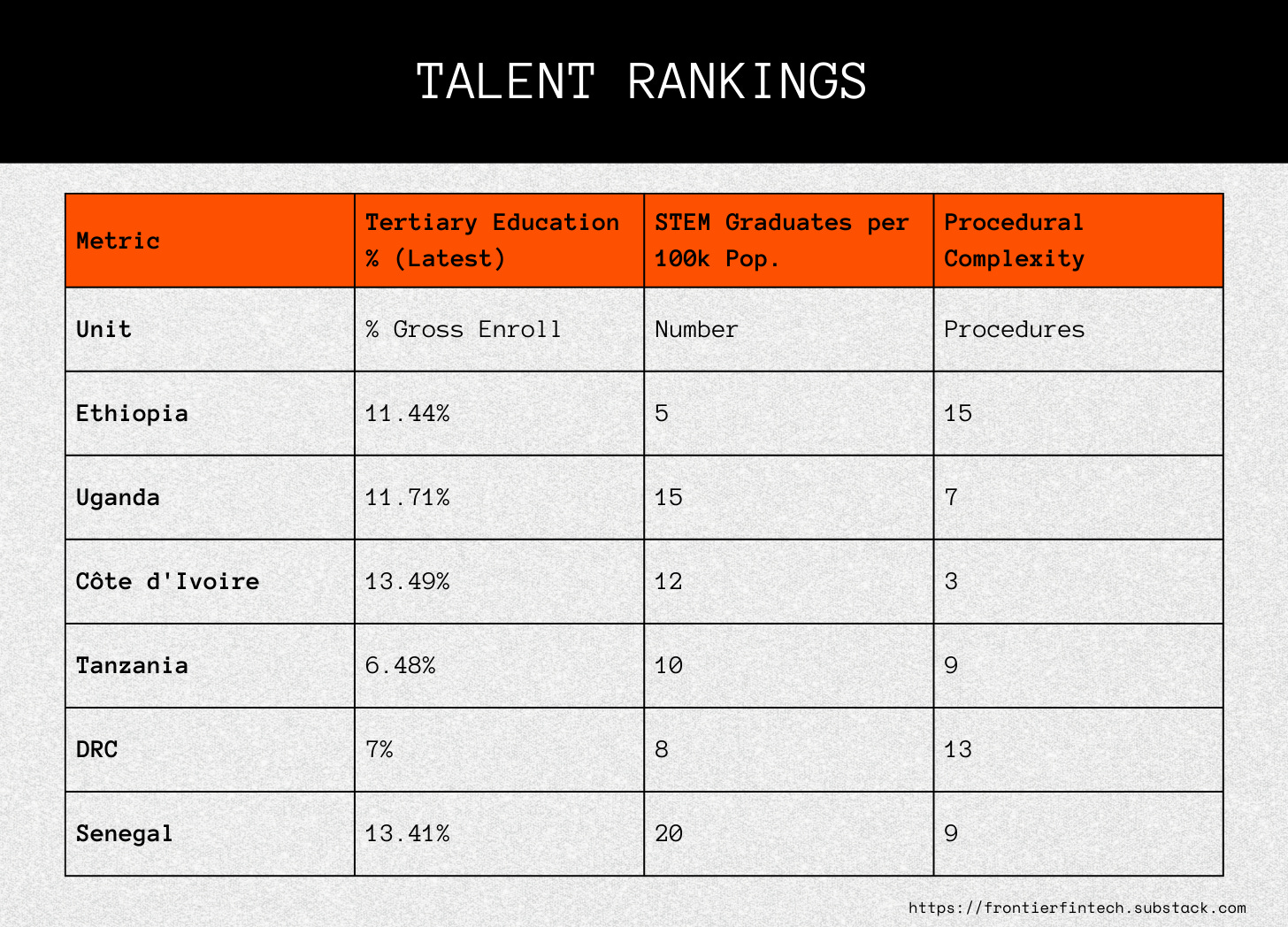

Talent

Our most important consideration is recruitment of the best people. The output of any company is the vector sum of the people within it. If we are able to attract the most talented people over time and our direction is correctly aligned, then OpenAI will prevail. - Elon Musk writing to Sam Altman and Greg Brockman in Dec 2015

People are often the most important component of a VC funded company. Getting the right people through the door, incentivising them and importantly being able to get rid of under-performers is a critical aspect of building a successful business. In tech, most founders often the repeat the well-worn wisdom of hiring slow and firing fast as being critical to success. The Collison brothers have applied this meticulously in building Stripe. Nonetheless, this approach is based on two assumptions;

The talent in the market actually exists to hire from - an implicit assumption in Western VC and Start-up culture but not necessarily true in all parts of the continent;

That you can fire people quickly - true in San Francisco, not necessarily true in many markets in Africa

Analysing talent therefore requires one to gage talent density and importantly the ease of firing people. To do this, we looked at the following metrics;

The number of STEM graduates per 100,000 people - available from the International Labour Organisation;

Tertiary Enrolment rates - what percentage of students enrol to high school from primary school - surprisingly low in many African countries;

Dismissal Complexity - How easy is it to dismiss an underperformer? From my experience, what matters is not what is written in the laws but how the law is actually practiced. This is usually a factor of how many procedures it takes to dismiss someone and how complex those procedures are. In some countries for instance, an external party must adjudicate on whether that dismissal is valid from a performance perspective. In some other countries, a labour tribunal must be involved. I looked at different data bases such as the DLA-Piper Global Employment Guide and ILO databases to determine this. The ranking gives points based on;

How easy are the procedural requirements - the higher the points the more complex the procedural requirements;

Is third party notification necessary?

Is third party approval necessary?

Is mis-performance considered valid grounds for dismissal?

Do priority rules apply i.e. preference for firing based on seniority?

Are there any additional obligations necessary for dismissal e.g. redeployment, retraining or excessive compensation?

Out of this, a total ranking was designed.

The ranking for talent then looks at a composite score based on the number of stem graduates, tertiary enrolment rates and dismissal complexity. For instance, a country could have the highest enrolment rates, highest stem graduates and easiest dismissal complexity ranking ahead of its peers. That would give it a 5/5 for each ranking and an average ranking of 5 i.e. 15 points based off of 5 points per ranking divided by three criteria. This means that this country has both talent and favourable labour laws. The multiplication only happens once the final composite score has been achieved. If a country has talent but unfavourable labour laws, it would be penalised. The overall metrics are below. Senegal, Ivory Coast and Uganda do well from a talent perspective. Ethiopia is held back by the complexity of firing people similarly to DRC.

Economy

This is simple and straightforward, a country needs to have a high GDP per Capita and a sizeable population. If a country has a high GDP per capita and low population, it may represent over-indexing based on an extractive industry or a tourism dependent economy. For instance, Seychelles and Equatorial Guinea consistently rank amongst the top countries in GDP per capita but wouldn’t necessarily be considered as standout candidates for Fintech FDI. In this ranking, we rank each country by its GDP per Capita and Population separately, normalize these rankings and then average them out. For instance, a country that has the highest GDP per capita amongst its peer group will get a 5 and the country with the highest population will also get a 5. The average of the two will then be the economic ranking - this ensures that the two metrics are evened out. The overall rankings are below.

Ivory Coast has the highest GDP Per Capita but its population is one of the lowest in the group. The same applies to Senegal. Ethiopia and DRC have the largest populations but the latter has the lowest GDP per capita minimising its rankings.

Economic Structure

Almost all empires were created by force, but none can be sustained by it. Universal rule, to last, needs to translate force into obligation. Otherwise, the energies of the rulers will be exhausted in maintaining their dominance at the expense of their ability to shape the future, which is the ultimate task of statesmanship. Empires persist if repression gives way to consensus - Henry Kissinger

It’s great to have a large economy and an even larger population, but these factors may mask deeper structural issues. All African countries have poor rule of law with differences only varying in the degree of lawlessness. Moreover, all countries have balance of payments issues affecting repatriation of capital and even the capture of that capital. In my experience, what I’ve found really matters on the ground from a rule of law perspective is whether a country is a post-conflict society or not. Why this matters is because conflict does something to a nation’s psyche both in terms of what kind of people rule you and whether you believe in the justice of the courts and the justice of the jungle. Both elements, who rules you and your type of justice system varies.

When it comes to who rules you, my view is that post conflict societies are often ruled by ex-military generals and not civilians. In the military, conflict is often dealt with through violence and moreover, command and control are the languages of the military. What this means is that post conflict societies tend to have warring elites rather than elites who work through consensus. This affects the commercial climate because in a situation of consensus driven elites, there’s a shared belief in protecting wealth rather than destroying it. Additionally commercial competition is seen as a war of attrition and ends up in wealth destruction.

When it comes to the capital account, the idea like last time is that the stricter the capital account, the bigger the Fintech opportunity when it comes to B2B payments and remittances.

Ethiopia, Ivory Coast and DRC are all post-conflict or even currently in conflict. The metric was whether there has been major conflict in the last 40 years and Uganda qualifies due to the war in the North with the LRA. Also, the country is largely run by ex-generals though arguably more polished than their peers across the continent.

Trade Openness

Trade openness simply reflects how much the country trades with the rest of the world and ideally with the region. From a Fintech perspective, the idea is the more it trades, the bigger is the payments and cross-border opportunity. However, one needs to be careful with this metric. Countries like DRC are very trade oriented but its mostly extractives. Usually trade openness is measured as the sum of exports and imports to GDP. In DRC’s case, it’s 91% which is one of the highest in the continent. To counter this, we added a metric that counters the extractive industry. This is the Natural Resource Rents as a percentage of GDP, the higher this is the more the country depends on natural resources. Rents are usually calculated as the difference between the price a commodity is sold and the cost of producing it. In this case, this is a penalising metric in that the higher it is, the lower the normalised score.

Combining these means that a country will do well if it trades a lot and it receives little in natural resource rents. In the case of the DRC, it scores high on volume of trade but is penalised by the natural resource rents. This also applies to Uganda. Senegal is a standout in that it trades a lot and receives little in natural resource rents. Though this may change with the gas discoveries. From the table, Ethiopia barely trades with the rest of the world but also doesn’t have an extractive industry. Nonetheless, it’s clear that Senegal is a standout performer followed by Ivory Coast.

Digital Infrastructure

Fintech relies on digital infrastructure like we’ve seen in Nigeria, India, Brazil and the UK. Basics such as smartphone penetration and 4G network coverage are important factors in the growth of Fintech. Whilst all these factors will improve over time therefore reducing their significance to the broader analysis, they still matter. Senegal is a standout country, data from GSMA shows that it has 48% smartphone penetration coupled with a 68% 4G network coverage. Whilst its a relatively smaller country to the others, it’s still an impressive feat. Ivory Coast is also a standout performer in terms of both smartphone access and 4G network coverage. DRC as would be expected struggles given the size of the population and the relatively lower GDP per capita.

Mobile Money

My view on MoMo is always that it’s the native way of doing financial inclusion in Africa. Therefore the more advanced a country is from a MoMo perspective, the lower is the opportunity for consumer Fintech. This was the core argument of the last article about markets in Africa. This was validated by the success of consumer Fintechs in Nigeria, Egypt and South Africa and their inability to scale in Kenya and Ghana. From the table below, Tanzania and Uganda lead with Tanzania in particular witnessing a boom over the last four years with total MoMo uses skyrocketing to 66m from 30m in 2020. Uganda is also a leader in MoMo with Airtel and MTN Money being key players.

Ethiopia is seeing incredible growth with M-Pesa and Telebirr by Ethio Telecom both being formidable players. I expect it to be a major MoMo market in the coming years. Ivory Coast and Senegal are also significant players, growing fast with the interesting aspect of having Wave, a non-Telco amongst the leaders in MoMo. DRC is growing but this number is hampered by the sheer complexity of the country.

Overall Results

Overall Rankings

The overall results are below. I’m sharing the table just in case you may want to do the analysis by yourself

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.