#66 - Agentic AI - The missing link to the next wave of financial service provision

Why a re-think of software architecture from traditional back-ends to Agentic AI could be the key to unlocking the next wave of growth in Digital Financial Services

Illustrated by Mary Mogoi - Website

Hi all - This is the 66th edition of Frontier Fintech and the first of 2025. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

Reach out at samora@frontierfintech.io for sponsorships, partner pieces and advisory work. I help clients think through markets, products, positioning and strategy across Pan-African Fintech.

Sponsored by Skaleet

Co-Existing with Legacy Systems for Minimal Risk

Banks need to intricately manage the dance between stability and innovation. If you don’t innovate, you run the risk of being irrelevant to an ever demanding and changing client base. Skaleet positions itself as an agile companion to existing core systems, allowing banks to innovate without the need to overhaul legacy platforms. Skaleet’s API-first and modular approach means banks can layer new digital propositions on top of their established systems. By enabling banks to launch new digital products independently, Skaleet addresses the hesitations surrounding a full core migration and provides a faster, less risky way to meet evolving customer needs.

The flexibility Skaleet offers lets banks leverage their existing infrastructure while deploying new services that respond to modern banking demands. This strategy keeps the core stable while freeing banks to develop and test customer-focused digital propositions tailored to various demographics.

Contact Brice for Partnerships and Beatrice for Sales;

Introduction

You can see the computer age everywhere except in the productivity stats - Robert Solow;

In 1987 one of the most famous economists Robert Solow made this quip. He was referring to the then “hype” around computers and how the intended productivity benefits that would accompany computing were nowhere to be seen in the official statistics. A number of commentators then latched on to this statement to show that probably the computer age lacked substance. Over 37 years later, another famous economist Mario Draghi made a different statement. Lamenting that Europe was falling behind the rest of their developed peers, he put the blame squarely on technology. Europe was not innovating and adopting modern technologies like China and USA and in fact, almost all the delta between Europe and USA’s growth rates were down to factor productivity driven by technology. Many years later, you could see computing everywhere in the productivity stats.

In the long-term, technology is the biggest driver of productivity and thus sustainable economic growth. Nonetheless it’s never linear. I’ve been thinking about this and AI - specifically how AI will drive productivity in the financial services sector. In this regard, it has to be a step change from where we are now to whatever it will look like in the future. The big question is how AI as a General Purpose Technology will affect the financial services sector. Satya Nadella gave a clue in a recent interview in the B2G podcast early in December 2024. In the discussion, he mentions how AI will change Software and this to me was a missing link in my thinking about AI and financial services.

This article explores how General Purpose Technologies (GPTs) diffuse throughout the economy, why AI is the next GPT, and how Satya Nadella’s perspective on AI-driven software development applies to banking. We’ll see why merely layering AI onto existing workflows is insufficient and how a “first principles” approach (like Henry Ford’s assembly line) is needed to unlock AI’s full potential.

General Purpose Technologies, Electricity and Henry Ford

If AI is to have the massive impact that is being predicted, then it needs to be a General Purpose Technology just like electricity, the internet and microprocessors. A general purpose technology is one that has the ability to drastically alter society. Usually, there are four criteria used to analyse whether a piece of technology is a General Purpose Technology. They are;

Pervasiveness - Are they used widely across the economy and across industries?

Improvement - Do they have the potential for continuous improvement, becoming better and cheaper over time?

Innovation enablers - Can they facilitate the development of new products, processes and industries?

Complementarity - Do they work well together with other technologies, creating synergistic effects?

When you look at these criteria, it’s obvious that AI will be a General Purpose Technology if it’s not already. It's already pervasive given that we’re seeing utilisation across all industries from media and content creation to logistics and manufacturing. The Scaling Law is becoming an empirical law just like Moore’s law with doubling happening every 6 months thus showing aggressive and consistent improvement. The launch of products like ChatGPT and Replit show that AI is enabling innovation and it's clear that AI requires other core technologies such as microprocessors, the internet and electricity. In fact, it requires significant improvements in all three for its continued scaling.

Despite this, like Solow’s quip, we may be seeing AI everywhere apart from the GDP figures. To understand why and what needs to happen, one has to look at how previous General Purpose Technologies diffused through the economy. The best example is the impact of electricity on manufacturing and factory design.

Late in the 19th century when electricity was invented, factories were designed around steam engines. Steam engines drove machinery through a maze of belts and pulleys. This setup not only limited where machines could be placed but also made factories noisy, inefficient, and prone to frequent breakdowns. With the introduction of electricity, entrepreneurs initially applied electrical power through dynamos onto the existing factory design i.e. they replaced the central steam engine with a dynamo. Barely any productivity improvements materialised and in fact, most entrepreneurs as of the early 20th century preferred the tried and tested steam engine.

Productivity growth driven by electricity needed a rethink of the entire factory design. To unlock this, entrepreneurs realised that electricity enabled power to be distributed in a precise manner to wherever it was needed within the factory. Machines could now be powered individually, freeing factories from the constraints of centralized power systems. This newfound flexibility allowed manufacturers to redesign factory layouts to optimize workflow, reduce wasted space, and enhance worker productivity. Furthermore, electric lighting enabled round-the-clock production, accelerating output. By unlocking efficiency and adaptability, electricity paved the way for modern mass production, reshaping industries and laying the groundwork for the rapid economic growth of the 20th century.

Ford’s Highland Park Plant

Ford Workers at a Moving Assembly Line at Highland Park

Both Images Sourced from The Collector

The greatest example of this was Henry Ford and the assembly line. With this insight, Henry Ford built a factory around an assembly plant where workers were distributed along a conveyor belt powered by electricity. With such a layout, workers could focus on extremely specific tasks. Moreover given that power was more reliable and there was good lighting then workers could work around a shift system enabling 24 hour production. These innovations in both factory design and production management enabled mass assembly of cars making the car a mass market product rather than an elite product. The surplus enabled by this productivity shift enabled Ford to give his workers a US$ 5 per hour wage, unheard of in the early 20th century. Henry Ford Stated “We believe in making 25,000 men prosperous and contented rather than follow the plan of making a few slave drivers in our establishment multi-millionaires.” Taylorism and other management innovations from the 20th century stemmed from Henry Ford’s early works.

For AI to drive similar productivity gains, we must redesign financial workflows rather than simply layering AI on top of outdated systems. Only then will we see transformative results.

Satya Nadella - AI Replacing Business Logic

Just before Christmas Satya Nadella sat for an interview with Bill Gurley and Brad Gerstner on their BG2 podcast. It was a wide ranging interview covering a number of topics within AI from agents to scaling laws to Microsoft’s relationship with OpenAI. Satya is one of the foremost thinkers in the world of technology and someone I respect a lot having read his autobiography “Hit Refresh”. I had written about AI before, covering what AI is and why it's expected to continue scaling, what that means for banks and in a discussion with Kamal, how players in the digital banking space should navigate AI. This discussion with Satya unlocked a few things for me and gave me clarity. Simply, like Henry Ford and electricity, Satya proposed a completely new way of working.

Source: B2G Podcast - To be Specific start from the 46th minute

In the interview, Bill Gurley asks;

I have a question about the CoPilot approach and I guess Mark Benioff's been kind of obnoxiously critical on this front and called it Clippy 2 or whatever. Do you worry that someone might think kind of first principles AI from ground up and that some of the infrastructure saying an Excel spreadsheet isn't necessary to know if you did a AI first product and the same thing, by the way could be said about the CRM, right?There's a bunch of, of fields and tasks that that may be able to be obfuscated for the user.

Bill is asking whether Microsoft’s strategy of building an AI powered assistant (CoPilot) on top of Microsoft 365 is necessary. The idea behind this is that if an entrepreneur builds AI from first principles then the whole idea of multiple fields on a CRM or the intense logic within Excel would be unnecessary. Satya responds by saying;

Yeah, I mean it's a very, very, very important question. The SaaS applications or biz apps. So let me just speak of our own Dynamics thing, right? The approach, at least we are taking is I think the notion that business applications exist, that's probably where they'll all collapse, right? In the agent era. Because if you think about it, right? They are essentially CRUD databases with a bunch of business logic. The business logic is all going to these agents and these agents are going to be multi repo CRUD, right? So they're not going to discriminate between what the backend is. They're gonna update multiple databases and all the logic will be in the AI tier, so to speak. And once the AI tier becomes the place where all the logic is, then people will start replacing the backends, right?... in fact, it's interesting as we speak, I think we are seeing pretty high rates of wins on Dynamics backends and the agent use. And we are going to go pretty aggressively and try and collapse it all right? Whether it's in customer service, whether it is in, you know, by the way, the other fascinating thing that's you are increasing is just not CRM, but even our, what we call finance and operations.

It’s useful to break down what he’s saying into simple English. Business applications today, like CRM or ERP systems, are essentially sophisticated databases with layers of business logic and workflows. These layers of business logic perform CRUD operations where they either Create, Read, Update or Delete information in the database. Satya Nadella envisions a shift where this business logic will move from these individual systems to a centralized AI layer, referred to as the "AI tier." In this model, AI agents will handle operations across multiple systems seamlessly, performing tasks such as updating customer records, managing financial data, or automating workflows without being tied to a specific backend. This approach reduces the need for rigid, siloed applications, as the AI agents integrate data and processes across different platforms.

As the AI tier becomes the hub for business logic, the underlying backend systems will become interchangeable. Companies will no longer feel locked into specific software like Salesforce or Dynamics, as the AI layer will enable a smooth transition between systems. Customers will only interact with the front end and won’t care what’s happening in the back as long as they’re getting results that matter to them.

Technology will move from systems that contain business logic with access to a few databases to AI agents where the logic is embedded that can interact with multiple databases. For instance, instead of having to update all client records on salesforce, your AI agent can check for information in calls, transcripts, emails, and a host of other data repositories.

This is akin to the factory redesign that enabled electricity to significantly impact production. The question is “What does this mean for banking systems?”

How do Banking Systems actually work;

To understand what this means for the banking and finance system, it may be useful to go back into history. Around 30 years ago, bank technology centred around client-server architecture where desktops that resided in the bank’s premises were connected to back-end servers. The core functions of these systems were basic operations such as balance checking and posting transactions. Making changes to the system was cumbersome and required ripping apart back end code or installing specific software in each workstation. The advent of the 2000s saw this same architecture expanded towards other platforms such as the internet and mobile. In Africa this was enabled by Enterprise Service Bus (ESB) systems that acted as a connector between the monolithic back ends and the new transaction platforms. This was driven by players such as Fintech Group, Cellulant and Craft Silicon. This era was largely driven by digital transaction enablement. There was little to no thought given to customer experience or customer journeys. A number of African banks touted digitisation of their transactions as strong credentials for being digital leaders. In fact, this digital transaction enablement was a strong wedge that allowed players like GT Bank, Access Bank and Equity gain market share.

As the Fintech era emerged in the 2010s, players like Backbase and other Digital Banking Platforms realised that tweaks could be made to the overall banking architecture to enable a better user experience. Whereas the earlier generation of systems was monolithic i.e. all the business logic is tightly packed with the Database, newer generations would change this by decoupling business logic and the core database. New thinking emerged that differentiated between systems of engagement and systems of record.

Source: Forrester Research

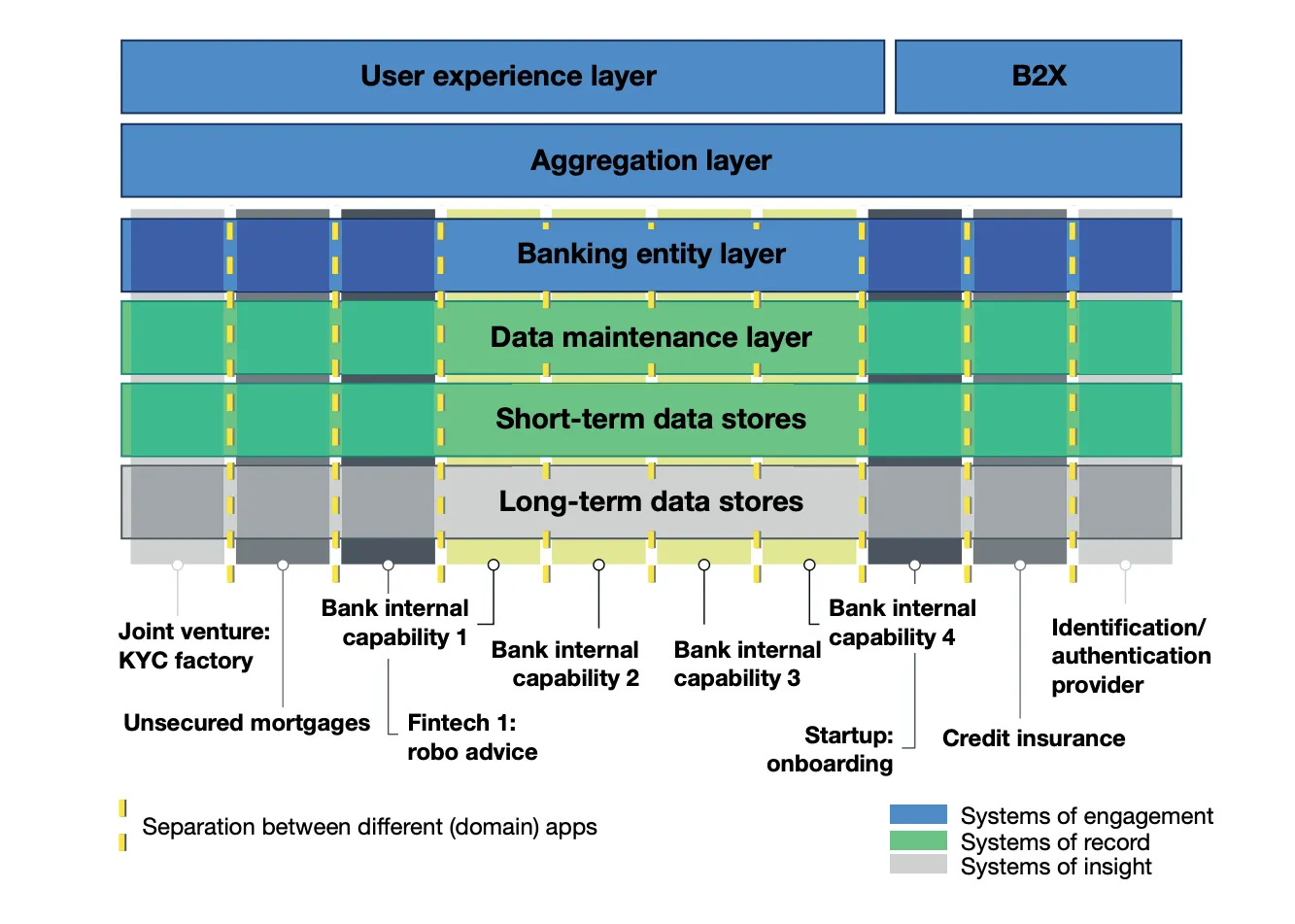

The diagram above from Forrester Research shows this decoupling. The Digital Banking revolution of the last 10 years has largely been about separating the business logic from the Core Banking System and simultaneously moving towards a service oriented architecture in which each capability can be contained within APIs. The growth of cloud computing, the emergence of APIs and the subsequent enablement of micro-services all drove this “revolution”. Most banks are still within this journey and the ideal architecture has been the one below from a presentation given by Backbase.

Source: Backbase

What Backbase and their peers within the industry propose within this diagram is that business logic is stored within an “engagement platform” that they build. This engagement platform can then have connectors to other services such as card systems, payments systems such as Nibss, M-Pesa etc, the core banking platform and any other third party platform. Through this, the idea is to create unique workflows in the engagement platform and leave every other system to be a system of record.

Most “modern and sleek” banking apps are built using such architecture. The outcome is;

Sleeker user experience vis a vis 10 years ago but still pre-determined;

A continued focus on transaction enablement;

A model in which most people transact digitally but still require branches for more complex discussions such as mortgages, loans, trade finance and complex customer service;

The best way to think about how banking currently works is deterministic vs non-deterministic workflows. Deterministic workflows where there are constrained outcomes e.g. move US$ 500 from account A to account B or accrue 1% interest each month have been digitised. Non-deterministic workflows where there are random outcomes have remained analog or delivered through customer service agents.

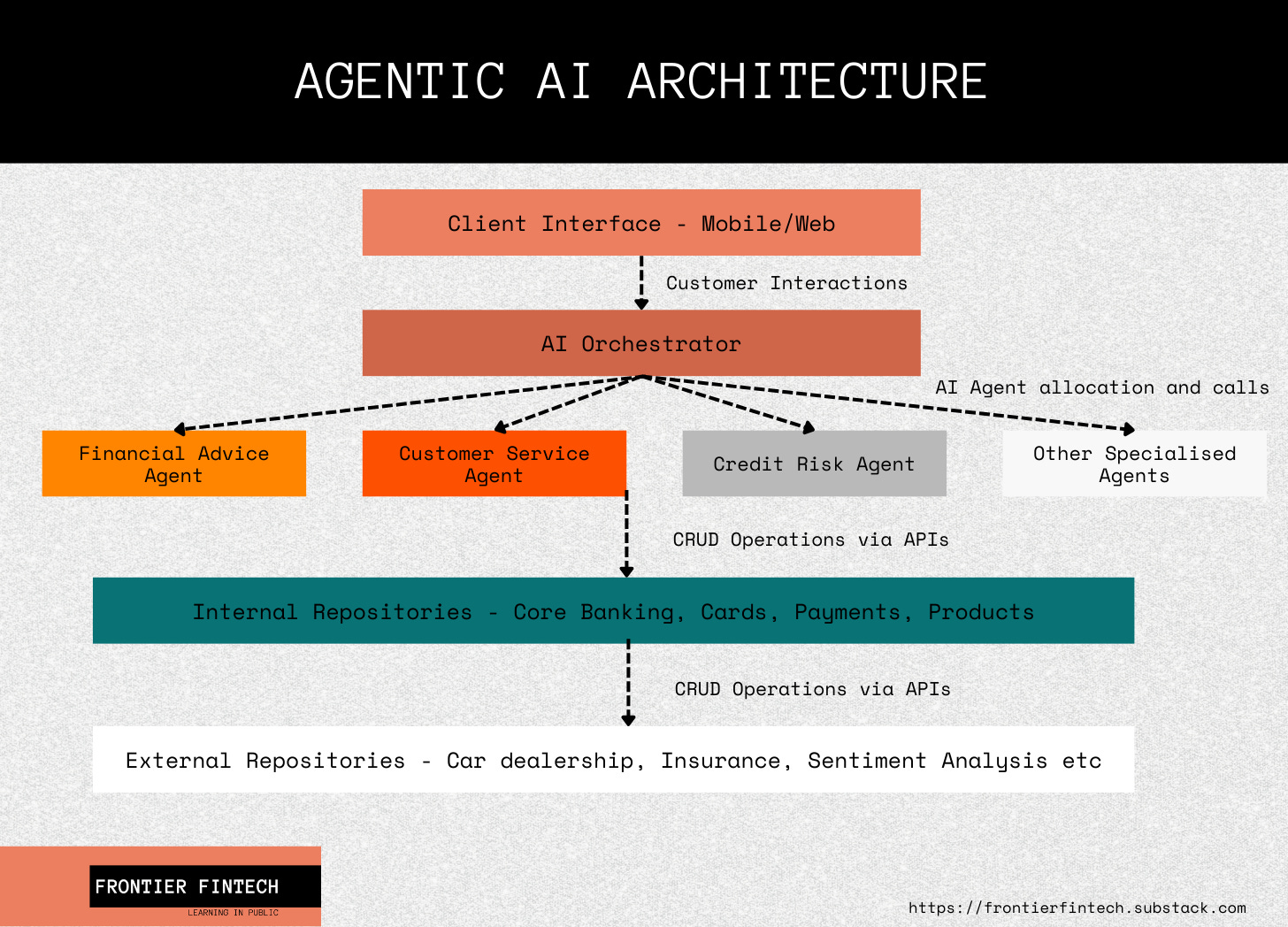

In the new agentic AI era, what Satya is saying is that the entire “engagement” layer would be replaced by AI agents. We’d move from a system of engagement built through custom workflows to AI agents orchestrating everything. They’d still connect to specific databases via APIs but now the idea is that they can interact with multiple repositories of data. The diagram below would be a good estimation of what future banking architecture would look like.

An example would suffice. Say a customer wants to purchase a car within 12 months, this is what would happen;

1. Customer Intent Capture

User Action: The customer opens the banking app (web or mobile) and says or types, “I want to buy a car next year.”

Conversational AI/Chat Agent: The user’s message is sent to a conversational AI component, which recognizes the intent: “Car Purchase Planning.”

2. AI Orchestrator Triggers Relevant Agents

Orchestrator Identifies Required AI Agents:

Financial Health/Planning Agent: To analyze saving/investment options, check existing account balances, forecast savings potential.

Credit/Risk Agent: To determine whether the user might also consider financing (e.g., auto loan) and estimate a possible loan pre-qualification.

Personalized Recommendation Agent: To provide suggestions tailored to the user’s spending and saving patterns.

Data Collection:

Retrieves current account data, monthly income, typical expenses from internal data repositories.

Optionally, fetches external data (e.g., average car prices, car loan interest rates, insurance quotes) from partner APIs.

3. Financial Health/Planning Analysis

Financial Health/Planning Agent checks:

Current Savings: Sums up the user’s savings and checking balances.

Spending Patterns: Evaluates monthly expenses, discretionary vs. essential spending.

Timeline: 12-month horizon to hit a car purchase goal.

Projection:

Based on historical spending patterns, the agent calculates how much the user can comfortably set aside each month to reach a target down payment (or entire purchase amount) in one year.

Recommendation:

Suggests a monthly savings plan (e.g., “Set aside $400/month” to afford a $5,000 down payment in 12 months).

May also propose an auto-savings feature to automatically transfer a set amount from the user’s checking to a high-yield savings account.

4. Credit/Risk Agent Assessment

Credit Inquiry:

The AI agent checks internal/external credit bureau data (with user’s consent) to gauge creditworthiness.

Calculates potential interest rates, loan terms, or credit lines if the user opts for financing.

Loan Pre-Qualification:

Suggests a pre-qualified auto loan amount and estimated monthly payment.

Outlines interest rate ranges, loan terms (36/48/60 months, etc.).

5. Aggregate & Present Options

AI Orchestrator:

Consolidates the savings plan from the Financial Planning Agent and potential loan options from the Credit/Risk Agent.

Enriches these options with additional data—like typical car insurance rates, estimated registration fees, or even local dealership promotions if integrated with external partners.

User Interface Response:

Presents a dashboard or chat response with:

Saving Option: “If you save $X/month, you’ll have $Y in 12 months for a down payment.”

Loan Option: “You qualify for an auto loan of up to $Z at an estimated X% APR.”

Combination: Possibly a mix of personal savings plus partial financing.

6. User Decision & Further Actions

User Chooses a Path:

If they pick a savings-only plan, the system sets up monthly transfers to a dedicated savings account.

If they prefer financing, the app can start a loan pre-approval process immediately.

Or they might do both: begin saving while also keeping a loan offer on file for later.

Follow-Up Triggers:

The AI Orchestrator can schedule notifications or reminders each month to ensure the plan stays on track.

Periodic checks (e.g., every quarter) to see if the user’s income/expenses have changed and adjust savings or loan recommendations accordingly.

7. Continuous Learning & Updates

AI Feedback Loop:

Agents continuously monitor the user’s actual saving progress, spending behavior, and credit updates.

If the user’s income increases or expenses drop, the AI might recommend increasing the monthly savings amount or re-checking better loan rates.

Personalized Engagement:

The system might suggest car-buying tips, partnership discounts, or even location-based deals (e.g., a local dealership offering a loyalty rate).

With this new approach, customers can get the best of both worlds. Deterministic workflows such as saving US$ 400 per month which is essentially setting up a standing order to a savings account can proceed as normal. Nonetheless non-deterministic workflows such as thinking through whether it’s better to save for a car or get financing can be done by AI agents.

Financial inclusion over the last 20 years has been driven by previous General Purpose Technologies such as Electricity, Computers and Microprocessors converging to enable cheaper distribution of basic financial services. The winners have been players like M-Pesa and others that drove the wave of digital transaction enablement. We’re reaching the ceiling of financial inclusion and therefore the next wave of financial services innovation should focus on financial health and empowerment which is a non-deterministic endeavour. The barriers to world class customer service and financial advice to the mass market is cost. It’s too expensive to provide a world class relationship manager to a client whose income is less than US$ 2 per day. Agentic AI could solve this problem. Could the winners in the next 20 years be those that utilise AI and specifically Agentic AI to drive these outcomes? If so, then the architecture needs to be what is represented in the diagram above.

Such a transition would unlock significant value in the financial services system. Currently in Africa, there’s a dichotomy as previously described where “lower value” clients are being pushed towards digital channels for basic “deterministic” self-service. Higher value clients are being served through a mix of high touch client service and digital channels. Banks are still investing in branches so as to build relationships whilst providing more advisory-like (non-deterministic) services. The challenge with this though is often both talent and incentives. At branch levels there’s often limited knowledge of the entire bank’s products and services and banks still rely on “specialists” in head office particularly for things like trade. Moreover, as we’ve discussed in a previous article, bank staff are incentivised to sell products and maximise revenue and not necessarily to help clients.

Agentic AI would solve this. For instance, if an SME client wants to import Maize from a neighbouring country, the agents would work to analyse the maize market, understand the risks in the transaction, analyse logistics and customs data to map out the import process and local maize consumption data. This would then lead to a well structured transaction memo with the right loan type and tenor being proposed. The end result is that the bank can structure way more transactions as opposed to relying on standard products such as term loans and overdrafts where a structured transaction would suffice. This at scale could go a long way to driving better loan outcomes for clients.

Implications & Considerations

New technology gives new entrants a wedge into the market. 30 years ago, the combination of relational databases and client-server core banking systems enabled banks like Capital One, Equity Bank and Access to scale. The opportunity in AI is financial enablement through Agentic AI. Incumbents will eventually catch up but any new AI native player has an advantage. Globally we’ve seen players like Revolut launching a number of AI driven applications and this could be their wedge towards taking on the larger players in the market.

The question is what are some of the implications of replacing the engagement layer with Agentic AI. It’s useful to approach this through logic;

If AI agents are working through APIs to handle workflows, then it's important that the banking systems are micro-service oriented, cloud native and scalable. This should advantage neo-core providers and could be the thing that unlocks value for players such as Thought Machine, 10x Banking, Skaleet and others;

If the bank is mostly providing a repository of data and rules around the client and their finances whilst the AI accesses multiple other repositories, then client journeys could be accessed from any app and not the bank app. This means that players like Alphabet could build a “life” app on top of Gemini and its agent system with connectors to different repositories. This life app will then relegate the bank to a store of value and we may no longer need bank apps;

If enablement of digital transactions led to a decoupling of transaction enablement from banks through bank agents and mobile money, non-deterministic workflows could in the future move away from banks. What this means is that a company could orchestrate agents to give world class financial advice and deal structuring 10x better than a bank can through data and technology. This company could then expose these “financial agents” to a client or a tech ecosystem and charge for it. Bank Agents could therefore do more than just enabling transactions and start performing some of the higher value services;

If the value is in agents, then internally for banks the value will move away from “bankers” to data scientists and AI engineers who are good at creating and training AI agents. Banks will increase their ranks of tech staff and reduce traditional roles, a shift that has already happened with the last generation of transaction enablement;

Banking will become hyper-personalised;

Cost structures could change over time. There will be less staff and more funds invested in tech and high skilled staff. This will lead to lower cost to income ratios than currently exist and ideally better operating leverage for those that adopt Agentic AI;

If everything is being orchestrated through APIs, then there will be a sharper focus on Open Banking and Open Finance in general. Whereas open banking has not been as valuable as expected, with agentic AI we could see a lot more account switching given its AI agents managing the process;

On the same point, businesses will have to expose their services through APIs and we’ll get deeper into the API economy. Whereas previously digital presence meant having a website, now it will mean having internal agents accessible by APIs. This will apply to travel companies, retailers, hotels and many more;

If AI capabilities are a key ingredient in this Agentic AI then big tech could have a way back into providing financial services at scale;

Some considerations for this Agentic future;

Players in the ecosystem will have to think through model explainability. A key plank of financial service regulations is that you have to be able to explain every decision you make. In an Agentic world, the idea would be that each agent's actions are logged and an explanation generated;

Regulators need to come to grips with AI and AI agents so as to be able to develop new regulations for this future.

Consideration will need to be given to cyber-security. A bad actor can take over an agent or a swarm of agents to inject malicious instructions to the system.

Conclusion

The idea of replacing digital banking systems with Agentic AI seems to me the most promising approach towards unlocking value in the financial system through AI. It seems to be the AI native way of doing things rather than surrounding existing architectures with generative AI systems.

Nonetheless, one cannot see this as a panacea in the financial services industry. Africa’s economy struggles from productivity at a very basic level. Globally, developed countries have gone through both an agricultural revolution and an industrial revolution. The AI revolution is being layered on top of a modern economy. Most African countries, if not all, have yet to undergo an agricultural revolution with most farming practices not being much different to those practiced over 100 years ago. This is a factor of land use and poor governance. The AI revolution can only do so much in the face of such obstacles and therefore we need to temper our expectations around what AI can do for the economy.