#54 - Stablecoins and Cross-Border Payments

Breaking down cross-border payments and how stablecoins are well placed to solve the current problems with cross-border payments

Artwork by Mary Mogoi - Website

Hi all - This is the 54th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. 🚀

Paid Subscriptions - This is the last “free” deep dive, from next week all deep dives will go behind a paywall. I may publish one free one every now and then.

Sponsorships - Frontier Fintech is read by leaders and decision makers in Africa’s Fintech ecosystem. Leaders from companies such as Nedbank, Standard Bank, Wave, Flutterwave, Paystack and Absa Group read this newsletter every week. If you want to grow brand awareness or educate the market on your product, reach out to me for sponsorship at samora@frontierfintech.io.

An update to the article. Here’s an audio summary, I’m experimenting on AI creating podcast summaries of my newsletter articles.

Introduction

Earlier this year, the president of Kenya was in a village in the Rift Valley touring the region and speaking to residents. At a town called Taptengelei, he stopped to speak to the residents at a nearby tech hub. Given the high rates of youth unemployment, the government had rightfully noted that digital jobs, particularly remote work, were a promising avenue for at the very least making a dent on the high rates of unemployment. He told the residents that across the country young people like you are getting digital jobs. His exact words included the phrase “finya finya computer itoe dollar”. This loosely translates to “press the buttons on your computer and earn in dollars”. As a bantu speaker, I’m always fascinated by how we tend to add emphasis by repeating a word so the literal translation is “press press your computer so that it removes dollars”. Jokes aside, I found this interesting because on one hand you could argue that it’s a government clutching at straws and hoping that digital jobs will solve youth unemployment. However, if you go by the assumption that governments only deal with facts, then it is a realisation that digital jobs are the future and Kenyan youths are well advised to get on this trend.

The main point though is not about the “pressing the buttons” on the computer, it is rather about how those “dollars” will reach your pocket as an African. I’ve argued here before that fixing this problem and enabling Africans to earn and participate in the global economy is critical. Globally this is being manifested in the idea of creating a financial system that is native to the internet.

One innovation that is growing in scale is Stablecoins. Across the crypto world, I think stablecoins hold the biggest promise for enabling easy, efficient and low cost cross-border payments. Banks, Fintechs and Regulators in Africa would be well placed to pay attention to this trend.

This week’s article will be structured as follows;

Why do cross-border payments matter both now and in the future?

What are the current problems or constraints when it comes to Cross-border payments and why do they exist?

What are stablecoins?

Why are stablecoins well placed to play a key role in cross-border payments?

Some considerations in driving stablecoin adoption;

Only by understanding the current cross-border payment ecosystem can we understand the promise of Stablecoins.

Why do Cross-Border Payments Matter?

Cross-border payments are pretty self explanatory. I wrote about them some time back in this article. Simply these are payments that are made between counterparties that are in separate countries. Within Africa they include intra-African payments and payments to the rest of the world.

McKinsey puts global cross-border payment flows at around the US$ 150 trillion mark with total revenues of US$ 2.2 trillion as of 2022. Payments are additionally expected to grow by a CAGR of 7% between now and 2027. McKinsey doesn’t give figures for the volume of African Cross-border payments as these are bunched up together with numbers from Europe and the Middle East. Nonetheless, these figures can be fleshed out in the following manner;

Total Trade in Africa is around 4% of global trade, global trade stands at around US$ 32 trillion meaning that total African trade stands at around US$ 1.2 trillion;

Total Intra-African trade is estimated at US$ 192 billion, being 15% of total African trade. This is often significantly underestimated and could be higher given the level of informal trade that goes on;

Lastly, remittances in Africa stand at around US$ 100 billion which is broken down into US$ 19.4 billion sent intra-Africa and the rest from overseas;

For our purposes, the main figures that matter are; the volume of total remittances, total intra-African trade (including informal unreported trade) and potentially a chunk of the US$ 1.2 trillion figure representing a growing volume of SME trade as well as services sold by Africans into the world. A figure of around US$ 750 billion would emerge (this is purely an approximation). This is a large number and is expected to grow even higher. There are a number of factors driving this growth;

Remittances will grow driven by increased rates of “Japa” from the continent. Japa is the Nigerian term for migrating to a developed country;

Increasing rates of e-commerce across B2B and C2B cases globally.

Increased intra-African trade driven by population growth and better integration largely driven by better communication capabilities.

Increased trade in services driven by global apps such as AirBnB, Upwork, Etsy and other gig platforms;

An increasing role for SMEs in global trade.

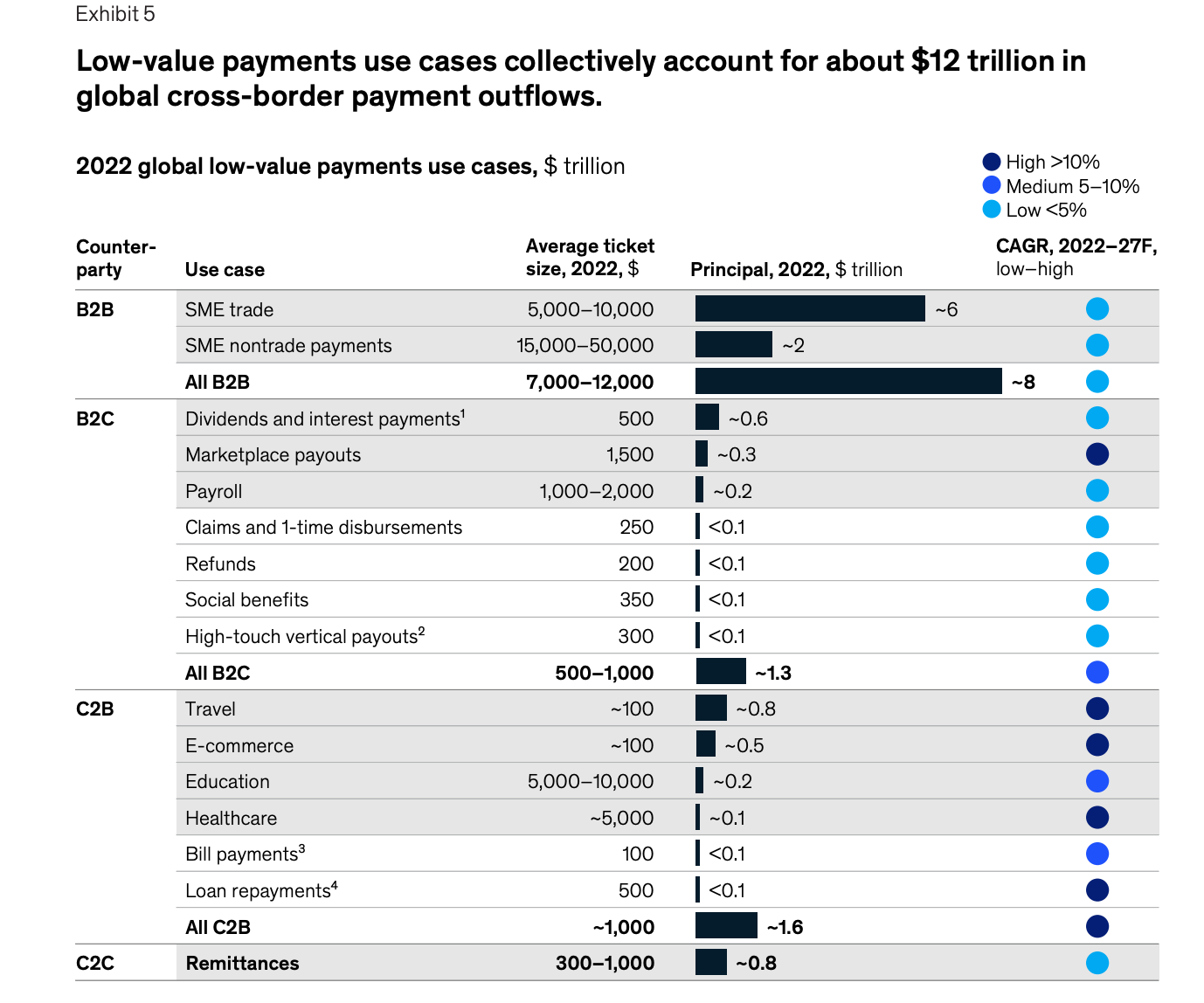

The table below from McKinsey does a good job at painting the global picture of “low-value payments” and their anticipated growth across different vectors.

Source: McKinsey

What are the Current Problems & why do they exist?

Despite the growth and scale of the cross-border payments market and its obvious potential, it’s an area that’s riddled with problems that companies and organisations are always trying to solve. To understand the problems that exist within cross-border payments, one has to understand the history of payments and therefore the core elements of a payments system. I’ve written before about payments here, here and here. So long as humans have existed, the idea of paying for something has been constant. Payments at their core involve an exchange of payment instructions and a transfer of value.

Payments therefore are built on three core principles. Of course this is a simplification, but it’s useful for understanding the fundamentals which are important when innovating. Payments must have;

Customer layer - where customer interacts with payments system;

Infrastructure layer - where payment instructions are managed and communicated;

Settlements layer - Where actual money moves between accounts.

Some simple examples would suffice. See the table below;

There are four primary ways in which cross-border payments are currently done. It’s important to view these methods as regards the customer layer, infrastructure layer and settlements layer. Through this, it’s easier to develop an intuitive understanding of the existing challenges with cross border payments. They are;

Remittance Apps;

Traditional Swift Payments;

Card Based Payments;

Cash Based Payments;

Remittance Apps

Over the last 10 years, cross-border payment apps such as Wise, Nala and LemFi have emerged and grown significantly. The apps target C2C payments although they serve B2C markets where the business is the one remitting money to customers abroad. They can be broken down as following;

Customer Layer - Users particularly those sending money download an app and enter payment instructions. These are usually; the amount to be sent and the details of the intended recipient of the funds.

Infrastructure layer - Typically, these apps use API-driven payments infrastructure such as Stripe or Flutterwave. These entities have built API connections with different banks and mobile money platforms across the continent enabling payment instructions to be communicated.

Settlements Layer - Typically, these companies use pre-funded models to run their business. What this means is a company like Nala for instance would have to have money in their bank in Ghana. When the bank receives instructions through the infrastructure layer, they would remove money from the Company’s pre-funded account and send it to the beneficiary’s account.

These models have innovated in two key ways. They have innovated on the customer layer by making the process easier and more intuitive. In the case of Nala, they have also built an API based infrastructure layer for payments communication. Despite this, the following challenges still remain;

Infrastructure vulnerabilities - Even if you have the perfect API infrastructure, you’re still relying on your partner banks which may have significant down-time thereby dropping some payment instructions. When this happens, the customer experiences failed payments. A reliability problem emerges. Benjamin Fernandes has a great blog about this.

Settlement Vulnerabilities;

To scale needs more pre-funding. Where you don’t have the cash, you often rely on third party capital providers who service the remittance markets. These capital providers fund your account but the additional cost needs to be passed on to the customer;

If the settlement is not instant but rather batched i.e. you process a set number of transactions then settle with the bank later, you have to plug in exchange rate volatility thus taking the price higher. Simply, the currency could move against you therefore it makes sense to have an in-built buffer that we can pass on to the client;

These apps have indeed made it easier and more convenient to send money, nonetheless they face some inherent vulnerabilities which weaken their promise of safe, fast and cheap payments. Simply, innovating on top of the existing infrastructure doesn’t solve the fundamental issues although it improves the customer experience.

Traditional SWIFT Payments

Traditional SWIFT payments have been around for decades and are typically used for B2B, C2B and even C2C use cases. They’re used for trade or payments in which payment confirmation documents are required. With SWIFT, the process can be broken down as follows;

Customer Layer - Typically branch based or web-based depending on the bank you use. A customer will typically have to engage with their bank and give the necessary payment instructions.

Infrastructure - These use the existing SWIFT messaging platform. SWIFT has made improvements with SWIFT Gpi, nonetheless migration to this has not been uniform. You can therefore get messaging delays of up to a week;

Settlements - Settlements happen through a network of correspondent banks. For instance, sending money from Ghana to the UK would involve money leaving your account, being transferred to an intermediary bank account in London before being finally sent to the beneficiary’s account. This network of intermediary banks all take a cut of the payment thereby raising the costs.

Traditionally this has led to issues of costs, reliability and delays. The costs are due to the settlement issues. Reliability is due to the complex messaging layer where a payment message can get lost between the webs of intermediary banks and the delays are also due to the nature of counterparties. Moreover, given increased AML and compliance issues surrounding global sanctions, Africa and many other parts of the emerging world have seen a pull-back by global correspondent banks thereby making settlements impossible in some countries. SWIFT is especially useful for corporate transactions but becomes uneconomical for lower value transactions.

Card Based Payments

Card based payments are used for C2B transactions mostly in the e-commerce space. They can be broken down as follows;

Customer Layer - Usually a web-based storefront or app where you’re asked to enter your card details. This is a standard process across the world;

Infrastructure Layer - Nowadays, this is API based system that involves a payments company such as Paypal, Stripe or Flutterwave exchanging payments communications directly with the Visa or Mastercard Network;

Settlements - These are done intra-bank once messages have been received by the relevant banks through the Visa network. Settlements can take 2-7 days due to compliance and other checks that are done by both the processing company and Visa.

Whereas card based payments have become the default for most online payments. Some challenges still exist;

Compliance checks often disadvantage beneficiaries in emerging markets as they are more likely to get payments flagged and thus funds blocked. African gig workers know a lot about this;

Usually exchange rates tend to be higher than what you’d get in the market;

There is an access issue as card penetration in emerging markets is usually not as high as in developed markets. This is particularly the case for East Africa where Mobile Money dominates;

Where cards do exist, FX issues typically throttle how much a user can spend on his card given the issuing bank doesn’t have the dollars to make payments;

Cash Based Payments

You’d be surprised at the number and volume of cash based payments used for regional trade. Prior to getting to the specifics, an example would suffice. Whilst at Sote, we had a client who traded Soya beans within the region. How this client would operate was that they would need to buy say 1,000 tonnes of Soya from Uganda for delivery to Nairobi. The cost was say US$ 200,000. Nonetheless, the payments needed to be made in Ugandan Shillings to traders in a specific town called Gulu. What this lady would then do is she’d change Kenyan Shillings to Dollars and send dollars to a Ugandan bank account. She’d then access this cash in Kampala and through money changers (due to the better FX rate), convert this into UGX. Once she had the UGX, she’d then go physically to the ground to pay traders in Gulu for Soya. This would be a regular occurrence for her business and in fact, is the primary way in which a lot of cross-border soft commodity trade is done. The transaction can be broken down as;

Customer Layer - Multi-modal by interacting with multiple banks and money changers;

Infrastructure layer - bank payment systems, physical by direct interaction with a money changer and by bus given that for a chunk of the transaction, she was actually in a bus with cash;

Settlements layer - multiple touch points - bank to bank settlements and in-person cash settlements;

Of course the challenges here are very clear;

Costs of transacting;

Security of losing money;

Risk of fraud by money changers - this can happen;

With the above breakdown, it’s clear to see that the main challenges with cross-border payments are;

Costs - Often a percentage fee due to multiple touch points be it Swift, card or through a cross-border platform such as Thunes, Flutterwave or Terrapay;

High exchange rates;

Delays - particularly for Swift and card payments;

Reliability - for Swift and modern app based payments;

These issues are intractable in nature. There’s only so much you can innovate on top of these systems. They are a continuation of the Dee Hock, electronic value exchange but are not yet truly native to the internet. Remember, the drivers for growth can largely be summarised as being internet driven, be it e-commerce, creator pay-outs or increasing SME trade. The challenge can then be summarised as simply the need for payments to mirror the ease and ubiquity of our current digital experiences.

The table below from the Economist shows that despite tech progress, the cost of making remittances is still high.

Enter Stablecoins;

Stablecoins are a type of cryptocurrency designed to maintain a stable value by being pegged to a reserve asset, typically a fiat currency like the U.S. dollar. They combine the benefits of cryptocurrencies—such as fast, borderless transactions—with the price stability of traditional money, making them useful for payments and trading. There are three types of stablecoins;

Stablecoins that are backed by Fiat - These are stablecoins whose value is pegged directly to cash in a bank or other liquid assets such as T-bills.

Algorithmic stablecoins - These are stablecoins whose value is maintained through an algorithm simply incentivising users to maintain a peg. In my view these are not worth a discussion because the idea of algorithmic incentives fails to understand the basics of finance. In a liquidity crisis, there is no market clearing price. The collapse of TerraUSD is a perfect example;

Stablecoins backed by other Cryptocurrencies - These are backed by a basket of cryptocurrencies and includes the likes of DAI and sUSD.

We will focus primarily on Fiat-backed stablecoins and it would be useful to give a more practical explanation. For a primer on Crypto and Defi, read here and here. However, understanding stablecoins requires an understanding of their relevant infrastructure starting from the core and going outward. There are five key elements to understand. They are;

Blockchain Networks - The blockchain network is the underlying technology that facilitates the issuance, transfer, and tracking of stablecoins. The blockchain provides a decentralised ledger where stablecoin transactions are recorded transparently. Simply, the blockchain is the database where all transactions are recorded. Some examples are Bitcoin Network, Ethereum, Tron and Solana. Solana has come to the fore of Stablecoin usage given that unlike other Networks such as Bitcoin and Ethereum, Solana has high throughput (65,000 TPS, higher than Visa) whilst being super low cost (around 1 cents per transaction). Visa gives a good breakdown on why Solana is so useful for Stablecoins here. The key responsibility for Bitcoin networks centres around transaction validation and the execution of smart contracts;

Stablecoin Issuer - The issuer is the entity that creates and issues the stablecoin. The issuer is responsible for maintaining the peg of the stablecoin to the underlying asset (e.g., U.S. dollar, euro) and ensuring that each stablecoin in circulation is backed by equivalent reserves. Some examples include Tether (USDT), Circle (USDC) and Paxos (USDP). The key functions for stablecoin issuers are;

Reserve Management - Ensuring that it’s always holding fiat assets that correspond to the value of the stablecoin circulating;

Regulatory Compliance - The issuer must comply with regulations, including anti-money laundering (AML) and know-your-customer (KYC) rules, to ensure the stablecoin's legal and financial integrity.

Redemption: The issuer provides redemption services, allowing users to exchange their stablecoins back into fiat currency;

Custodian - This is self explanatory. This is a licensed bank that holds all the money or assets that are issued by the Stablecoin issuer. Their work is simply custody, auditing and ensuring transparency;

Wallet Providers - Wallet providers offer wallets that enable users to store, send, receive, and manage their stablecoins. Wallets can be software-based, hardware-based, or integrated into mobile applications. Examples include the likes of Yellow Card, Coinbase, Sling and Metamask.

Exchanges - Cryptocurrency exchanges facilitate the buying, selling, and trading of stablecoins. They act as intermediaries between fiat currency and stablecoins or between stablecoins and other cryptocurrencies. Examples include Binance, Coinbase and Kraken. Simply they provide on-ramps and off-ramps into crypto as well as ensuring liquidity.

I’ve always argued that if you understand mobile money, then you understand stablecoins. Mobile Money works on the same principles as stablecoins and e-money is a stablecoin. That’s why the benefits of stablecoins such as faster transactions are the same benefits for mobile money. The table below makes it more practical.

The difference is that stablecoins are composable where each player has a role. Mobile Money is full stack where Safaricom controls the entire ecosystem. It’s a bit like the difference between Apple and Android ecosystems.

An example would suffice, Sling Money for instance is enabling fast and cheap cross-border payments that run on stablecoin infrastructure. They rely on the below infrastructure;

Blockchain Network - Solana due to it’s high transaction throughput and low costs of less than a cent for a transaction;

Issuer - Paxos due to it being highly regulated and fully backed by cash;

Custodian - Paxos Trust Company;

Wallet Provider - Sling Money builds the wallet;

Exchange - I don’t know which exchanges they use as they haven’t disclosed this;

Sling Money doesn’t charge fees on P2P transfers but makes some commission when converting crypto to fiat or vice versa. They intend to make additional revenue from debit cards and other features down the line.

In the business space, companies like Cedar Money and Nilos are looking to deploy crypto infrastructure, particularly Stablecoins to enable B2B payments particularly for trade. Remember, unlike other technologies such as SWIFT and Visa, Stablecoins are built 100% on internet native technology such as the blockchain network. Where they integrate with the traditional world is only at the custodial level where money is at rest and therefore, reliability and throughput does not feature. Due to this, the benefits for stablecoins become clear. They enable;

Instant Settlements;

Low Cost;

Increasing throughput through Solana;

24/7 accessibility &;

International Reach;

Given they’re integrated to Crypto Exchanges, they have access to liquidity. Note that it’s reported that Binance in Nigeria handled close to US$ 26 billion in one year;

This has led to total stablecoins in circulation being worth around US$ 170 billion with monthly volumes of around US$ 460 billion being traded.

What are some useful use cases;

Due to these features, a number of banks are looking to launch stablecoins and regulators across the world are hurrying to issue adequate regulation for Stablecoins. Banks such as JP Morgan, Revolut, Standard Chartered Bank, Hokkoku Bank and ZA Bank are all participating in the stablecoin economy through either launching, facilitating or experimenting with stablecoins. Some use cases could include;

Banks could facilitate cross-border payments through stablecoins. This would be especially useful for instance if a regional African bank like Access Bank launched a stablecoin that enabled cross-border payments. There would need to be a central treasury and some sort of inter-subsidiary settlement mechanism. However, the customer would be able to send money from say South Africa to Ghana instantly. The transactions would be South African Rand to Ghanaian Cedis but done through Stablecoins. The lady trading in Uganda could have used Stablecoins to settle directly with her traders in Gulu.

Fintechs could focus on the following opportunities;

Cross-border Trade e.g. SME trade between Zambia and India with stablecoin settlement mechanisms. The hard work here is to onboard SMEs and build trust with them. The settlements and payment mechanisms should be your bread and butter;

P2P payments - The likes of Yellow Card are already doing this within the continent. How they scale is a function of customer acquisition. The hard work just like in building SME trade payments is on onboarding and building trust;

Payment Service Providers such as Flutterwave could issue their own Stablecoin for cross-border payments enabling new check-out and remittance use cases. Globally Paypal is doing this. One of the benefits would be integrating to global gig work platforms to enable payments to workers;

There’s value in building rails or enterprise infrastructure that enables access to stablecoins. Again, this could be an opportunity for the likes of Paystack, Flutterwave or others to build. Simply, creating the capabilities that would enable banks, companies and fintechs to transact in stablecoins. Simply enterprise wallet infrastructure. This would involve abstracting the exchanges and networks and presenting an easy, intuitive workflow that would enable Loop DFS in Kenya for instance to launch stablecoin wallets and payment capabilities;

Regional MoMo players such as Vodacom M-Pesa and Wave can issue their own stablecoins to enable easier cross-border payments. This would involve moving away from intermediaries such as Onafriq and Visa and doing it yourself. The problem is currently being solved informally so there’s already proof of concept.

What are Some Challenges

Within the continent, regulators are not fully onboard. Whereas globally, regulations such as Markets in Crypto Assets (MiCA) are coming up to enable stablecoin regulation, the journey within the continent is less straightforward. The main thing to get right is to ensure that stablecoins are backed by cash sitting in a bank and regulators in Africa have experience in this through MoMo. You could go further and insist that the cash is 100% held in reserve but the principle is that cash and not assets such as T-bills and bonds sit with a well regulated bank.

However, in Africa, the challenge of currency management would come in. Regulators would worry that stablecoins would accelerate dollarisation. However, this can be managed by how you regulate pay-outs and especially how local payments are done. The main challenge would be that it would be difficult to control the exchange rates that are being used by crypto exchanges. Additionally, it would take away a lot of FX volumes from banks making monetary policy harder to execute. This requires a forward thinking Central Bank to navigate.

From an adoption side, the biggest problem I’ve found is that crypto companies use crypto language to sell their services. Customer pitches usually include terms such as “We use stablecoins and crypto exchanges to ensure blah blah blah”. This is a non-starter, customers don’t care and what they want is simple fast transfers. A more useful pitch would be that “we can pay your supplier in minutes” and back this with an actual demo. Moreover, companies need to build solid go to market capabilities to drive trust and adoption. Some examples would be;

Engage with the freight forwarding industry to map trade flows i.e. which businesses are making payments and to which countries. Logistics companies have this data;

Have a very strong promise - You could for instance say that if your payment doesn’t arrive to your supplier in x minutes, we’ll refund you double the amount sent - AirBnB had a guarantee program for their hosts to drive adoption;

Invest significantly in market education particularly seminars and conferences with industry associations. For example, car importer associations or Avocado export associations.

Develop the right language to engage bank partners and regulators across the continent. It’s important to move away from looking like Crypto Bros to looking like serious people who know what they’re doing. Language will play an important role in this.

Stablecoins could be the solution to finally enable dollars to come out of the computer across Africa. This will take thoughtful building and interactions with regulators nonetheless if the fundamental problem is one of enabling digital opportunities to deal with unemployment, then African governments need to come to the table.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora@frontierfintech.io

You make valid points. Although given that people can currently get stablecoins using crypto exchanges then you'll just have a situation where trade and transactions are happening in the blockchain without any visibility by the government.

Insightful piece as always. With regards to educating the market, are there companies you've seen who did this excellently?