#53 - Could Mobile Money be the Future of SME Banking

Why players like M-Pesa, MTN Momo, Airtel Money and Wave could be well positioned to succeed in Small Business Banking

Artwork by Mary Mogoi - Website

Hi all - This is the 53rd edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. 🚀

Introduction to Article

Small business banking or SME banking is a key focus area across the continent. Most banks have identified this as a focus area for growth and a number of large Fintechs not only in Africa but globally are building products to serve this segment. In Africa, players such as Moniepoint in Nigeria and Tyme Bank in South Africa are making inroads. Globally, Revolut and Nubank have both identified business banking as the next growth area after retail banking. This week I argue that Mobile Money (MoMo) players in Africa such as M-Pesa, MTN MoMo, Airtel Money and Tigo in their respective markets are well placed to win in this space. As Africa moves away from a manic focus on financial inclusion and towards a healthier focus on financial empowerment, SME banking will come clearer into focus not only from banks but also from policymakers and regulators. To understand why MoMo could be the solution to small business banking, it’s important to answer the following questions sequentially;

Which specific segment of SME banking should we focus on and why?

Why does this segment matter for now and in the future?

Why does it matter to offer banking services as opposed to the existing payment wallets?

Why hasn’t the market offered these services already at scale?

Why MoMo is well suited to win;

Things MoMo needs to exeecute to win

Defining the actual SME Segment

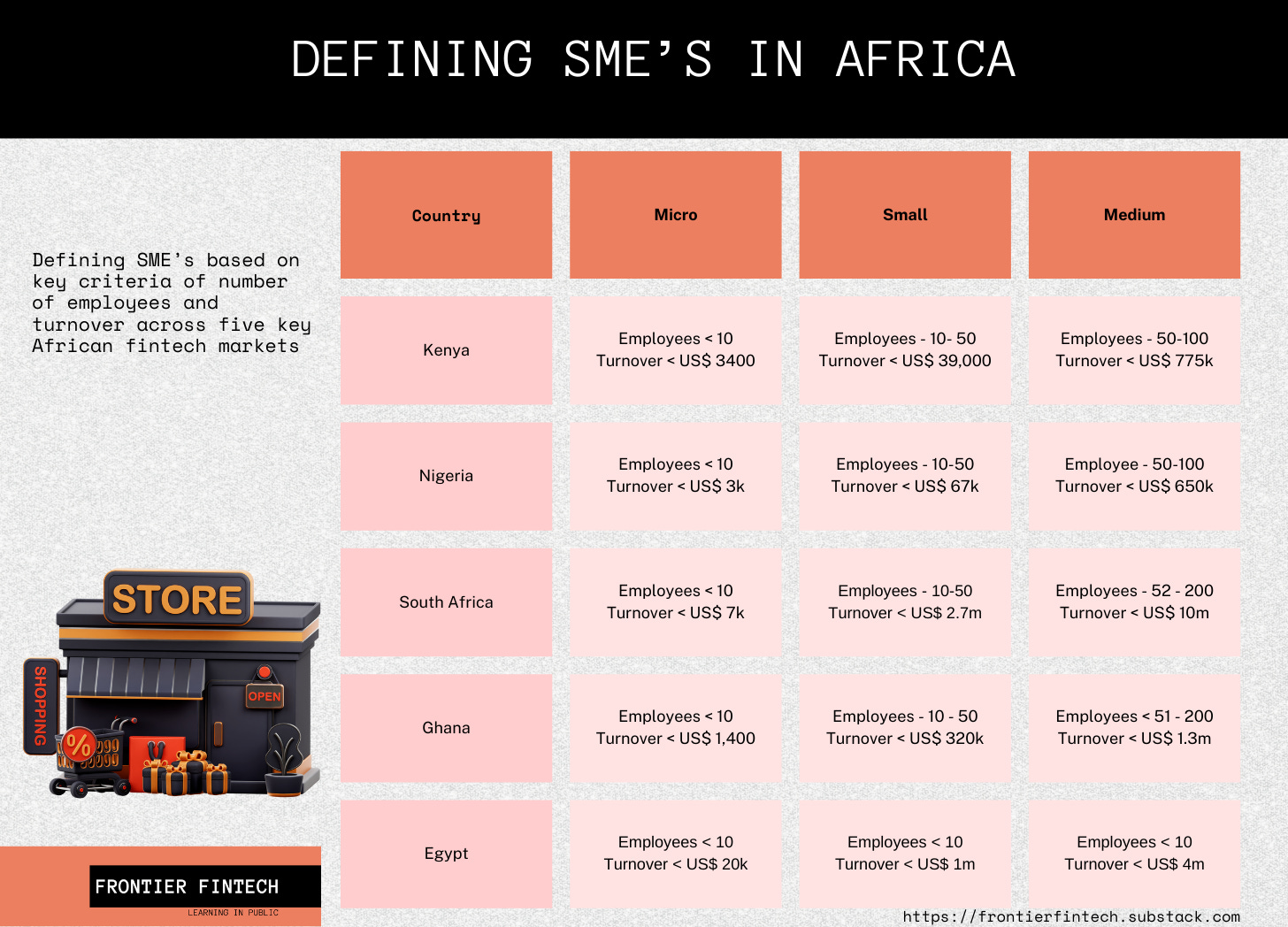

The exact definition of SME varies from country to country. What would be a large Corporate in Nigeria may be defined as a small family business in the US. This taxonomy is a function of the size of the economy. Nonetheless, a few criteria have over time been developed to clearly segment an SME. These include;

Number of Staff;

Annual Turnover;

Asset Base;

The table below gives an overview of how SMEs are classified across different countries. In as much as asset size is not featured, typically a rule of thumb is that asset size is double the turnover.

The definitions in the table above are rather broad and are insufficient not only for market segmentation but even for making a useful analysis about how to solve a specific problem. Safaricom in a report done together with Financial Sector Deepening (FSD Kenya) did a brilliant job in creating more useful archetypes that can support segmentation. Safaricom’s study gives 5 SME archetypes segmented amongst a number of criteria such as age of business, age of owner, size of the business and a number of other key criteria. They came up with 5 archetypes;

Emerging Businesses;

Developing;

Maturing;

Established; &

High Potential (HiPot).

The table below gives a better distinction and the full report can be found here.

What’s clear is that access to finance and use of technology is lowest amongst emerging and developing SME segments.

I will focus on the emerging and developing segments given that as a group they represent almost 50% of all SMEs surveyed but potentially a much higher percentage of the total population. I will call this group Emerging SMEs but this includes the Developing Segment as well. This rhymes with a report done by Moniepoint which is definitely worth a read. In Nigeria, almost 60% of total businesses are owned by founders who are less than 34 years old. Additionally, 47% of small businesses in Nigeria have been in existence for between 2-5 years.

In terms of business activity, Emerging SMEs are mostly engaged in wholesale and retail trade, food and drinks, fashion, beauty, IT services and other professional services. A number of them engage in social commerce using platforms such as Whatsapp, Instagram and Facebook to market their products and services. Many however are your typical informal retailer. Lastly, there is a very low level of formal business incorporation with only 21% of SMEs in Kenya being formally registered. This low level of incorporation repeats itself across the continent apart from more mature markets such as South Africa where registration rates range between 60 and 70%.

Defining the Problem

We can then define the Emerging SME segment in the following manner;

Owned by Millenial and Gen-Z founders who are 35 years and below;

Have been in existence for less than 5 years;

Have low levels of business incorporation;

Are smaller than more established businesses i.e. turnover of less than US$ 100k per annum;

Have low levels of financial inclusion in terms of;

Access to loans from the commercial banking sector;

Access to insurance;

Access to business tooling;

The major challenge faced by these emerging businesses is a lack of access to useful financial services. We have done a decent job so far in enabling access to basic financial inclusion through the provision of payment wallets or POS machines to enable collections. This has been led by merchant payment services provided by Mobile Money players as well as POS systems in Nigeria and South Africa. Despite this, these businesses report low access to products such as loans and insurance. If you were to define the concept of financial vulnerability or its counterpart, financial stability, that is defined by access to affordable credit, insurance and business tooling, then emerging SMEs would score high on vulnerability and low on stability.

Overall, this leads to a SME finance gap that in general is reported as being worth US$ 19 billion in Kenya according to the Safaricom report. In the continent, this has been reported as US$ 330 billion by IFC with US$ 70 billion being the formal SME finance gap i.e. formally registered business.

Why does this Emerging SME Segment matter

The next question is why does this segment matter for anyone? If you were running a business banking division, chairing a bank, investing in a start-up or running a start-up, why should you pay attention to this group of businesses. In all likelihood, given the 80-20 rule, this group is likely to generate less in gross turnover than large corporations or more established SMEs as a group. Why then should you bother with such a motley crew of unregistered businesses? There are a number of practical and long-term issues at play.

Demographics

The African demographic story has been told multiple times. The numbers are pretty well known, including the fact that over 60% of the population is below 25 years of age with another 15% being between 25 and 35. Over three quarters of the African population is below 35. It’s more than likely that our demographics will end up being a demographic disaster as opposed to a demographic dividend given the level of governance across the continent. Therefore one has to be careful about quoting African demographics and making rosy predictions about how similar societies have benefited from similar demographic structures. Nonetheless, what’s clear is that the rate of business formation in the next 10 years will be very high. Over 50% of business owners in Nigeria reported unemployment as being the biggest driver of business formation. When you couple this with the demographic structure, it’s clear that a significant number of businesses will be formed in the coming years.

Of course, unemployed people opening business due to lack of economic prospects seems a lot like the blind leading the blind. However, there are a number of other factors that could mean that we could have a jobless but yet striving commercial landscape.

Changing Face of Production

I’ve written about this in the past here about the changing nature of production and distribution. The industrial revolution brought about standardisation and economies of scale as key concepts that defined business formation and structuring. 50 years ago, the costs of gathering information, marketing your product, coordinating with suppliers and many other business functions were relatively high. This led to scale as a competitive advantage as you could spread these costs across a wider commercial surface area. With the advent of the internet and other products such as social media, these costs, essentially the costs of running a business have reduced significantly. This has reduced the barriers to entry for many businesses. For instance, I have a “plug” who supplies me with sports gear. He has a stall in one of the many informal markets in Nairobi but most of his business is done through social media. Through these channels, he not only markets his products but he also coordinates sales, fulfilment and negotiations with all his stakeholders. His tools i.e. Instagram and Whatsapp are generally free asides from the costs of sponsored ads, data and a device. Alternatively, I met a young man who etches car registration details on the car windows for a living. He works fully remote and is often contacted by used car dealers to support new buyers. He earns around 40$ per car and can work on up to 5 cars per day. This is a serious business. Such dynamics are spread across a whole host of other industries.

AI is likely going to have an explosive impact on small business formation given that not only will the existing tools get better, but small businesses will have intelligence as an additional factor of production. Whereas large businesses could hire the best tax advisors and legal minds, small businesses will be able to access such capabilities at a fraction of the cost. Such dynamics will mean that coming generations will likely be composed primarily of entrepreneurs rather than workers. Capitalists rather than the proletariat.

If anything, prior to the industrial revolution, economic production was built around small artisanal businesses that were family owned. Large corporations and the resultant rise of a working class were largely a function of industrialisation. AI and better tech could lead us back towards artisanal production with the only difference being a concentration of large businesses that sell the picks and shovels to these smaller enterprises such as OpenAI, Facebook and large telcos. Jobs may reduce, but work won’t. It may be a rosy prediction, but it’s not a crazy prediction.

Urbanisation

In the 60s, the rate of urbanisation in Africa was in the mid to late teens. Currently, the rate of urbanisation stands at about 50% and this is expected to grow to 60% by 2050. Comparatively, urbanisation in Asia stands at 50% and in Europe it's closer to 75-80%. Packing people together in cities (agglomeration) has an impact on how people live their economic lives. Rural people often tend to live on subsistence meaning that they’re not tied into modern economic lives centred around cash and trade. Urbanisation in Africa is being driven by people moving into cities as well as former rural areas becoming urban. Increasing urbanisation will create increased demand for goods and services and this will likely impact the rate of business formation. It’s expected therefore that most of the businesses being formed will fall into the Emerging class of enterprises. Studies have shown a strong link between urbanisation and business formation through factors such as access to markets and faster exchange of knowledge.

With these factors in mind, it’s not crazy to think that the bulk of business banking will centre around this “emerging” class of businesses. Moreover, the fastest growing businesses are likely to still be this segment. It’s therefore impossible to ignore.

There is anecdotal evidence that this segment is growing and significant. In Kenya, there is a growing clamour amongst the tax authorities to get M-Pesa data and to get data from digital platforms such as AirBnB, Uber and other Tech platforms. The insight behind this is that they’re seeing a slowdown in corporate and income tax whereas economic activity doesn’t correspond to this slowdown. The logical conclusion is the growth of gig work. Recently, Lagos announced steps towards taxing gig work. One insight from the book “The Master Switch” is that governments only deal with facts and not ideas. Therefore the steps we’re seeing in Lagos and Nairobi with regards to gig work is a response to actual facts that they’re seeing with regards to business formation and growth.

Why Banking SMEs is so difficult

The next question that can be asked is, why is it important to bank these emerging SMEs that also include gig-workers? After all, in a world of Mobile Money, a merchant wallet that has basic store of value features is sufficient. Indeed, Safaricom introduced a product called “Pochi la Biashara” which is simply a merchant wallet that enables small business owners to separate personal funds and business funds. It has seen incredible success growing to over six hundred thousand wallets with annual inflows of over US$ 500m per annum. Although this is not a reasonable proxy for deposits, it shows the sheer volume of collections being done by Safaricom in the SME space. So the question remains, despite this, why do Emerging SME’s need bank accounts. There are a few of reasons that truly stand out and make sense when put under scrutiny.

Access to Sustainable Credit Products - Banks given their lower cost of funds relative to other players in the market can offer lower cost loans. APRs for non-banks, especially those targeted at the emerging SME segment are often very high, up to 100%+ in most cases. Banks can offer term-loans and overdrafts that are reasonably priced considering the cost of risk;

Legibility and Credibility - Bank accounts give a business legibility and credibility when it comes to suppliers, applying for contracts and a whole range of scenarios in which counterparties may request for certified bank accounts.

Access to a wider suite of payment services - Whereas players such as Safaricom, Airtel Money and MTN have done an incredible job in expanding the suite of payment services available to MoMo subscribers, including the use of virtual cards, there are still payment options that are beyond the reach of Emerging SMEs. These include mostly trade payments such as LCs or guarantees;

The growth of Pochi la Biashara in Kenya further is a proof point of the demand for small business banking services in the market. Why is it so difficult to provide small business banking services in Africa? In particular, why is it so difficult to do successful small business lending at scale?

Cost of Service Delivery - Africa is a phygital market or a ‘cybernetic’ market as Stephen Deng says in which physical presence and relationships are needed to augment digital services. This then requires investment in physical infrastructure such as branches so as to build out relationships. Nonetheless, branch investment is expensive especially when coupled with the associated investments in people and technology. This is made worse by Africa’s geography. Africa is a very large continent that is sparsely populated leading to very low branch density i.e. branches per 1,000 people. This same reason is what made Mobile Money take off in Africa and not succeed to the same extent in countries like India that are more densely populated thereby enabling branch based banking.

Fragmentation - SMEs vary widely in terms of size, industry, maturity and financial needs. This makes existing banking methods that rely on standard customer archetypes unsuitable for this business segment. Catering to Emerging SMEs requires a more flexible product architecture that is data driven and built for customisation;

Data for Risk Analysis - Following on from the previous point, there is a dearth of data from SMEs given they lack accurate financial statements and operational data. This makes it very difficult to underwrite risk for credit analysis. Banks therefore are not able to provide loans to this segment. This makes it difficult to onboard because access to a loan is a major incentive for an SME to open a bank account. If a bank can’t provide a loan, then why should an SME open an account? It’s a chicken and egg problem;

Customer Acquisition and Service - Emerging SMEs require strong relationship management particularly when it comes to building trust. Given their low revenues and subsequently bank balances, the unit economics of providing relationship management to this segment doesn’t make sense. This becomes a negative cycle of low acquisition, insufficient customer service and therefore low customer retention;

Low Margins & High Risk- Emerging SMEs have low revenues and are also very price conscious. The emerging SME segment therefore tends to suffer from low revenues per customer and less than stellar unit economics compared to, say affluent personal banking. SME banking thus becomes a volume game and especially one that benefits from bundling multiple products.

KYC and Compliance - The costs of staying on top of compliance for SME accounts are not only high but also variable and unpredictable. SMEs tend to lack business registration and have poor record keeping practices if at all. This often requires throwing an incredible amount of bodies to ensure that the bank is generally compliant.

In a nutshell, it’s important to offer banking services to this emerging segment and there are valid reasons as to why this segment has been excluded.

Key Factors Required to Win in this Space

So far we have mapped out the following;

Which segment of SMEs is most in need of banking services;

Why this segment matters;

Why banking services are required on top of existing mobile wallets;

What challenges exist when it comes to banking the emerging segment of businesses;

If this is convincing and true, then the question that should follow is “how do you win in this segment?” and also “how do you build for this segment?”. I’ll answer these sequentially.

How do you win in this segment;

This is more of a discussion as to what competencies you should have to win and this should be informed by the previous segment on why it’s so difficult to win here. At a minimum, any company building a proposition for this segment should have the following;

Strong Cybernetic or Phygital Capabilities - Given the issue of physical dispersion of SMEs and the need to build trust with clients, one requires physical presence coupled with strong digital capabilities. The physical presence is largely to enable in-person discussions that would support onboarding, client support and advice. The scale and breadth of your cybernetic capabilities needs to be credible;

Strong Technological Core - You need to be a technology company so that you can credibly build the tech solutions that this segment would require. This would largely centre on onboarding, customer life cycle management, payments, user experience and importantly embedding AI to enable AI driven agents for your emerging segment. The latter would be a key differentiator and can credibly create winner take all dynamics;

Data and Visibility - A company needs to have access to a wide spectrum of data on their clients that includes financial, operational and alternative data. Although the latter may be not so relevant on its own, combined with the former two, it could create very unique insights that are proprietary to the entity managing the data. Given that data is a key hindrance to banking the emerging segment, an entity that has access to this data has a very strong head start. The data should be coupled with full visibility of the client’s cash flows. This visibility should be complete i.e. no cash flows should be getting into the business that are unseen.

Leverage - This is simply the ability to get your clients to do things and them feeling the need to follow your instructions given they feel they have something to lose if they don’t. Ant Group has leverage on its SME clients given that it can boot them out of the marketplace.

Multi-product - Given the low-margin nature of Emerging SME banking, it’s useful to be able to bundle multiple products into your offering so that you can increase revenue enabling you to cover your costs of acquisition and serving this segment.

Of course, you need to have banking knowledge and expertise, but this is table stakes.

Who is best place to win in this Segment

Given the criteria above, it’s easy to see how Mobile Money would do well if they launched a business banking proposition;

A mix of a wide agent network, multiple customer service points driven by their telco heritage and an existing digital relationship means that they’re as cybernetic as they come. The uptake of Pochi la Biashara shows that they can acquire customers at scale and at a very low cost given that these phygital relationships already exist. Moreover, MoMo players have a trusted brand;

MoMo’s have tech capabilities given that they have existing engineering teams and experience in managing tech projects. It’s not crazy to suggest that MoMo players already hire some of the best tech talent in their markets.

MoMos have rich data that includes transactional data both personal and business, data that can enable them to map out your transactional and behavioural patterns;

Given that MoMos have strong brands, wide networks and given their market share; may control a key choke point of having control over your business collections wallet; they can exercise leverage over you. I always say that leverage is more important in managing a loan portfolio than data driven credit analysis;

Multi-product - Given the Telco heritage, MoMos naturally have multiple products. Whereas such data is sketchy, most SMEs use data, calls, SMSs, mobile money and a few other products. It’s therefore easier to look at this group and form a blended ARPU that includes business banking.

Other players that have set themselves up to win in this segment both in Africa and globally include;

Moniepoint - They have built world class cybernetic capabilities in Nigeria and continue to do so in other markets in Africa including Kenya. They control a client’s collections and have a strong core technology team. I wouldn’t be surprised if Moniepoint in the next 10 years is one of the largest banks in Nigeria;

Yoco - Starting off on SME point of sales enables you to develop not only visibility but relationships. This is coupled with digital invoicing and online payment solutions targeted at the Emerging SME segment;

Wave - Mobile Money but on a modern arguably more scalable tech platform;

G-Cash in Philippines has all the makings of a successful Emerging SME business banking player. On the base of Globe Telecom which has a 54.7% market share, G-cash passes the test;

To sustain the impressive growth of MoMo, a breakthrough needs to be made in their product offering that can unlock a significant revenue pool. Using M-Pesa data for instance, the take rate on business payments is only 30bp compared to a take rate of 106bp for consumer payments. Revenue from Merchant overdrafts was only US$ 2.3m against total business payments revenues of US$ 300m. Simply, MoMo is barely scratching the surface when it comes to the total revenue pools available in business banking. Given that consumer payments are relatively mature and are only being driven by demographics rather than an increase in revenue per user, then it’s time to unlock the next billion dollar opportunity.

How Mobile Money Players can Execute;

Small business banking is not a new concept. Banks have been doing this at varying levels of success for centuries. Table stakes include basic payment capabilities, working capital loans, relationship management, credit risk management and monitoring and a whole host of other services that already exist. To create true differentiation, particularly for MoMos, there needs to be some heavy duty problem solving using first principles thinking. My view is that there are three key areas of innovation that are required. Licensing, Product and Capital Management;

Licensing

Mobile Money companies are not banks and therefore they can’t offer banking services. Currently, they only offer payment collections under the existing wallet model. To be able to offer banking services for the reasons stated earlier, some thinking needs to be done as regards licensing. I think there are three options, each with their risks and rewards.

Obtaining a banking licence - This would include either applying for a banking licence or acquiring an existing bank. There are a number of benefits that would come with this including access to central bank payment rails as well as better treasury management options. Nonetheless, I don’t think that African Central Banks and Commercial Banks would be welcoming of MoMos into their ranks given the risk of losing access to the liquidity that MoMos enable e.g. Trust Accounts. Moreover, this would be a multi-year project with very little scope of experimentation and product iteration. It’s a project that I would only green-light on the basis of sufficient traction and market validation;

Acquiring a Microfinance - This is a lighter touch version of obtaining a banking licence and has successfully been executed before by players such as Branch. In fact, a number of Neobanks in Nigeria are actually licensed Microfinance Banks. It’s a good stepping stone to a full banking licence. In Kenya for instance, M-Pesa could explore the option of acquiring a Microfinance Licence and offering SME banking given it would now have a balance sheet it can control. On top of such a licence, MoMo players like M-Pesa could work with a panel of commercial banks for international payment services such as SWIFT as well as FX capabilities;

Banking as a Service Model - In as much as there has been hullabaloo about BaaS recently given the failure of Synapse and the resultant mess with Evolve Bank and Trust, I still think that BaaS is a valid business model. The key conclusion here is that there needs to be clearer regulatory standards around this. Therefore to execute on BaaS, you need strong technical chops and sufficient credit in the bank with your regulators. This is something that MoMo has in spades and can even launch as a stand-alone product. The execution of BaaS would have to be build on the Mercury model of working with multiple banks so as to spread out risk rather than having concentration risk with one bank counterparty;

Product

Small business banking has unique problems but also unique opportunities. The product function at a Mobile Money driven business bank has to be top class taking inspiration from the likes of Stripe. A number of problems need to be fixed;

Onboarding - Onboarding Emerging SMEs requires a lot of thought. Remember, only 21% of this segment are registered businesses. The issue therefore of incorporation needs to be baked into your product thinking. Stripe Atlas for instance has done a remarkable job of enabling entrepreneurs from around the world to register Delaware based entities. Frontier Fintech, Inc is a prime example. Most people fail to register due to the effort-reward calculation. It is a hustle to register a business and most of the time you have to deal with complex terms that tend to intimidate rather than simplify the process. A MoMo driven SME bank needs to enable businesses to easily incorporate. Simply, just copy Stripe Atlas and enable incorporation, business account opening, tax registration and document management in one place. Telcos have the capabilities to do this given they already offer hosting and cloud services to small businesses. Moniepoint for instance has partnered with the Corporate Affairs Commission in Nigeria as well as the Federal Inland Revenue Service to enable business and tax registration for small businesses through the app;

Integrations - Small businesses need solutions such as bookkeeping, payroll management and tax advisory services as they scale. Traditional approaches to these won’t work and they need to be offered through a full digital suite of services. This could enable proper ecosystem partnerships as MoMo work with digital services such as Seamless HR, Workpay, Zoho, Quickbooks, Churpy and other digital CFO and back-office tools;

AI Agents - AI is here to stay, in an earlier article, I talk about the evolution of AI and why we should expect AI to only get better, in fact in a violently rapid way. Small business banking is a scale game and traditional human based services cannot scale. A MoMo driven digital bank will have to utilise AI at its core for a number of services;

Customer support particularly context and client specific customer support - Klarna has already started benefitting from this and Airwallex is experimenting with AI for its sales teams;

Business advisory services - Imagine enabling small businesses to have world class legal, tax and accounting advisory services through your app. This is a recipe for extremely sticky winner take all behaviour;

Compliance and Credit - Risk functions such as compliance and credit can enable companies to detect anomalies, fraud and other issues much faster than traditional human based approaches. All these would ultimately reduce the cost to serve the Emerging SME segment;

Capital Management

One of the issues around SME lending is based on Basel 3 and its onerous capital requirements for a licensed bank. Simply, for each loan, under Basel 3, banks are required to hold more in capital. This gets worse when loans go bad and there is no acceptable collateral. For an SME lender, this would mean holding more capital given that defaults are likely to be higher and lending will not be predominantly based on traditional collateral such as real estate. Nonetheless the mitigating factors would be that your loan book would be more short-term and higher frequency i.e. loans are taken and repaid at a much faster clip. These would be working capital loans and shorter term loans for equipment and other capital expenditures. The higher capital would also be off-set by a higher proportion of non-loan based income such as subscriptions for the AI, FX revenue and trade finance revenue.

If only it were so easy

One must understand that either my whole thesis is completely wrong or if it’s right, then these insights have been discussed within MoMo corridors and there could be reasons as to why they’re not being executed. These could include;

Very strong regulatory pushback - In Kenya for instance, regulators could be afraid of market dominance by M-Pesa if it were to get a licence to offer such services. The challenge could be that already M-Pesa is a systemic risk to Kenya’s economy and expanding their scope could be a further systemic risk. I think the solution to this would be to enable M-Pesa have banking capabilities whilst simultaneously pushing for a universal payments system like Pix and UPI that would lessen the systemic risk and open up the P2P and merchant payments space;

Talent - MoMo in Africa is almost an adult given it has been in existence for 17 years now. Its success could mean that the hunger for innovation has waned. How this happens is through atrophy. Whereas extremely talented senior executives can be hired, the challenge comes in incentivizing middle management which has calcified around their benefits and has an incentive to retain status quo. This is an area where entities like Moniepoint could benefit from but need to be careful about in the long-term;

Lobbying by the Banking sector - This is related to the second point above. Nonetheless, MoMos obtaining banking licences could have a significant impact on existing banks liquidity. Lobbying by banks is not new. They have arguably played a part in the evolution of MoMo licensing in Nigeria with the outcome being failure to launch by MoMo.

Ultimately, this is a space that I think requires banking solutions at scale. Currently the convergence of technology, physical presence and AI are creating the conditions that would enable most of the traditional barriers of SME banking to melt away. It will be interesting to watch how this space evolves.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora@frontierfintech.io

It's one of a number of issues. The challenge is that penalties to non compliance are so high that from a risk reward perspective, banking SMEs becomes a headache

Lovely article. You should check out Lesaka, who are trying to provide the full suite of products you mention in the SADC region + Kenya