#16 The Insurtech Opportunity

Analysing the existing insurance landscape and the insurtech opportunities within whilst looking at some global insurtech leaders

Hi all - This is the 16th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. 🚀

Executive Summary

Africas insurance market is worth US$ 68 billion in terms of Gross Written Premium. Over 70% of this business is based in South Africa which has a big life insurance market with insurance penetration of 17%.

The insurance business in Africa analysed from the Kenyan experience is plagued by poor and costly distribution, fraud, inefficient claims processing and pay outs. This is in addition to structural issues such as low GDP per capita and cultural issues surrounding insurance.

Insurtech as a subset of Fintech is focused on deploying modern technology to add value to elements of insurance such as customer acquisition, enterprise management, claims processing, fraud analystics and customer life cycle management. Globally, companies such as ZhongAn and Ping An in China as well as Metromile have shown that big data, analytics, telematics and other technologies can enable insurers to improve their performance in terms of loss ratios and contribution margins.

Ultimately, technology is arguably the main way African insurers can improve their operations and grow business as measured by Gross Written Premiums and insurance penetration.

Introduction

This week, I take a look at Insurtech and the opportunity for Insurtechs in Africa. Recently, Lami Technologies a Kenyan insurtech start-up raised US$ 1.8m to scale up its API-based insurance distribution platform. In January, Pula, an insurtech that provides digital and agricultural insurance raised US$ 6m for expansion as well. Other insurtechs such as Oko in Mali and Alphadirect in Botswana have also raised funds from investors to grow their business. The levels of funds being raised in the insurtech space are not as large as those in other fintech vectors such as payments and neobanking, but they are growing.

Africa has one of the smallest insurance markets in the world measured as Gross Written Premium which is estimated at US$ 68 billion. In contrast, the Asia Pacific region has GWPs both life and non-life of over US$ 1.1 trillion.

Source: McKinsey

The diagram above from an article by McKinsey gives a useful breakdown of the various markets. Kenya for instance has an insurance penetration of 2.7% with Tanzania having a penetration of 0.7%. In East Africa and West Africa, general insurance premiums exceed life insurance mostly due to mandatory motor private and commercial insurance. In Nigeria, the oil and gas sector is the main contributor accounting for over 50% of GWP in the non-life segment. In South Africa Motor insurance is the largest segment in non-life accounting for over 40% of premiums. Health and motor insurance account for over two thirds of the market in Kenya.

Focusing on Kenya, one finds that the insurance market despite having solid underlying fundamentals such as favourable demographics, increasing urbanisation and growing GDP is underperforming. Insurance penetration calculated as gross premiums divided by GDP has actually reduced from 2.75% in 2015 to 2.34% in 2019. Gross premium growth when adjusted for inflation has barely grown over the last five or so years.

Primer on the Insurance Business Model

Insurance is a risk business, the focus is largely on taking on risk on behalf of your clients. The idea is that for a fixed fee, an insurer can take on a risk on your behalf and cover you in the event that risk occurs. This is mainly done by pooling as many clients as possible with the implied assumption that the probability of all your clients facing loss at the same time tends to zero the more clients you have.

For instance, with medical insurance, the idea is to receive premiums from as many clients as possible. The premium should be well calculated so as to properly reflect the risk that is being taken on. If premiums accurately reflect the risk that is being taken on and if there is a sizeable number of clients such that the law of large numbers is in force, then in the event that there are claims, the pooled premiums will be able to cover the sum of claims. Insurers also cede some of these premiums to Reinsurers who tend to be larger and better capitalised.

To generate premium income, insurers usually have to work with brokers and agents who market their insurance products and service their clients. Brokers together with Bancassurance and direct sales are some of the traditional methods of selling insurance. These are incentivised through commissions which tend to be quite attractive rising to up to 30% for life insurance policies in some cases and between 6-12% for general insurance. Therefore, insurers have at the top line premium income from which reinsurance premiums are subtracted to arrive at net earned premium. Thereafter, insurers have to pay managerial overhead, commissions and any claims that may be incurred during the year. This then leads to the overall underwriting performance.

An interesting element of the insurance business is that you receive funds immediately for claims that may be incurred at a much later date. This situation leads to insurers having “float” i.e. premiums received but yet to be paid as claims. This float is usually invested so as to generate investment income and has been the pillar of Warren Buffett’s Berkshire Hathaway conglomerate. This article by the ever brilliant Marc Rubenstein is a very useful read on how insurance float has supercharged Berkshire Hathaway's investment success.

To succeed as an insurer, you thus need to be able to perform the following very well and consistently;

Accurately price risk;

Grow premium income in a low cost and disciplined manner;

Accurately assess claims and payout in a timely manner;

Run an efficient business i.e. managerial overhead should be sustainable;

Invest float to generate positive returns over the long-term;

As regards to overall performance, the key metrics are the loss ratio and the combined ratio. The loss ratio reflects total claims divided by total earned premium whilst the combined ratio includes the loss ratio plus commissions and overhead divided by the total earned premium. A combined ratio that is less than 100% is good as it means that you’re being paid to hold float. Any investment return is thus pure bonus. If your combined ratio exceeds 100% then you have to generate investment income to cover your loss. In life insurance, the key is to ensure that the value of your assets exceeds the estimated value of your liabilities.

The Kenyan Experience;

Source: Insurance Regulatory Authority (Kenya)

The table above shows KPIs for Kenya’s insurance industry. In both the life and non-life segment, commission expenses have been reducing whilst management expenses have been relatively stable. In life, the surplus to actuarial liabilities have been growing from 7.4% in 2015 to 12.6% in 2019. In the general insurance segment, the combined ratio shows that overall underwriting performance is negative and additionally, the claims ratio has been growing. This means that insurers have been relying on investment income which is largely variable and unpredictable.

Some key concerns about the Kenyan insurance space which can be extrapolated to other markets;

Insurance is a commodity product largely indistinguishable from the customers perspective, this has led to aggressive price competition thereby lowering premiums in key categories such as motor and health below their economic level;

Fraud in the claims process largely abetted by brokers and claims processors negatively affects profitability within the sector;

Medical inflation in the country coupled with underpriced premiums is a long-term concern for the sector. This boils down to larger policy issues around public health, whether the country takes on a fully private system like the USA or a more public system like in Europe or UK;

Legacy technology and processes. If you thought banks have legacy tech, you’ll be surprised at how old and outdated insurance core systems are in the region;

Poor distribution - buying insurance in Kenya is a horrible experience from quote generation to payments to renewals, there’s a lot of room for improvement in this sector.

Slow claims processing and payments;

In the past 10 years, underwriting performance has been masked by investment income which has consisted largely of fair value gains on investment properties. In the event of a slow down in the property sector and the stock market coupled with low interest rates, then the financial performance of many insurers is at significant risk.

Cultural issues around insurance which are exacerbated by the above issues. These centre on how Africans manage insurance through social systems such as fund raising as well as attitudes towards purchasing intangible promises - You often hear that if nothing happens to me then the insurance company will “eat all my money”;

As said earlier, the performance of the insurance sector in Kenya and Africa largely does not reflect the positive underlying factors such as urbanisation, growing GDP and demographics. I think there’s a major role to be played by technology in dealing with these factors;

Insurtech

Insurtech can be surmised as the introduction of modern technology in the overall domain of insurance. There is no single description as to what an insurtech is as it largely includes companies that are attacking different problems within the insurance value chain. These can be companies that focus on improving customer acquisition, claims processing, fraud analysis, risk analysis and pricing as well as customer life cycle management. The core technologies that are being applied in the insurtech space are;

Big Data and cloud computing to analyse large data sets that could help in various facets of the insurance lifecycle such as premium pricing and product development;

Artificial Intelligence and Machine learning;

Telematics - the collection of remote data onto a centralised location - very useful for motor insurance to analyse driving patterns and behaviour. Also very useful for health insurance using wearable technology to monitor health outcomes;

APIs that enable insurers to communicate with other services and can help with insurance distribution;

The diagram below gives a rough representation of the insurance purchase process, particularly within the field of non-life insurance which has had the most activity in terms of innovation.

The main areas where Insurtechs can add value particularly from an African perspective are;

Customer acquisition and onboarding - this is one of the most broken areas as its largely paper based and manual. Additionally, with insurance, pricing is not transparent, clear and reflective or individual risk. Total commissions and managerial overhead in Kenya within this sector can be estimated at around USD 200m per annum reflecting a significant TAM for insurtechs disrupting this segment;

Risk analysis and evaluation that enables dynamic and individualised policy pricing. This can eventually incentivise better driving and health outcomes;

Claims analysis and processing - using AI, computer vision and other technologies to better process claims, evaluate their correctness and make payouts. Computer vision for instance is being used to evaluate the damage caused by a car accident and calculate the cost of the payout. This is often combined with GPS to analyse the exact location of an accident;

Policy life-cycle management can be improved significantly. Renewing premiums is a headache, insurtech can work on products and customer journeys that enable you to plan and pay for your next renewal cycle by accurately predicting the cost of your premium and offering financing solutions for the same;

The below diagram shows some of the insurtechs covering the different areas of the insurance lifecycle;

Global Insurtechs that I Like;

Zhong An

ZhongAn Insurance was formed in 2013 and its initial focus was online insurance starting by shipping insurance on Alibaba. A decision was taken early on that it had to invest in its internal cloud based insurance platform if it was to succeed. Investments in big data processing, AI and ML, telematics and computer vision have enabled it to grow significantly over the years by venturing into other business lines.

Zhong An is currently the largest online P&C insurance in China and the 9th largest in the country. It’s the youngest P&C insurer in the top 10 ranking. It has grown to over 520 million users and its Gross Written Premium stood at US$ 2.6 billion dollars as at end 2020. ZhongAn has two core lines of business; the existing P&C insurance business as well as technology export where they offer their core platforms as a service to other insurers.

The diagram above shows that over time, Zhong An has been growing its GWP whilst reducing the combined ratio. The reduction in the combined ratio is led by improved understanding of risk and pricing led by analytics, improved product design and disciplined underwriting.

Some things I like about Zhong An;

Zhong An has 47% of its staff working in technology and has made 503 patent applications markings its credentials as a genuine technology company;

New innovative products within their digital domain have grown to account for over 16% of total GWP compared to the traditional health and motor insurance;

Zhong An launched a full stack internet hospital that offers diagnostics, basic primary care and pharmaceutical deliveries. It currently has 23.9 million users and is growing. This is a core factor that insurers need to consider. Brand perception in health insurance is low and customers view it as a commodity. Integrating upwards into a full stack health offering can drive brand value and customer loyalty whilst better controlling costs;

Due to its technology leadership, Zhong An launched a fully digital bank and insurer in Hong Kong called ZA Bank which has grown to over 220,000 clients in HK.

Ping An Insurance

Ping An is a global insurance behemoth with revenues of US$ 169.1 billion, assets of US$ 1.4 trillion and a market cap of US$ 211 billion. Net profits stand at US$ 20.8 billion. Ping An was started in 1988 in Shenzhen targeting the staid P&C business. Ping An literally means safe and well. The company has later diversified into all aspects of financial services including asset management, banking, stock brokerage and leasing. In 2008, the founder Ma Mingzhe decided that Ping An would pivot towards being a technology company and fully embraced cloud computing.The company sees itself as a technology company and has built its business around technology. Ping An shows that a traditional insurer can pivot towards being a tech driven company. Incumbents need to have the courage and boldness to take on this vision.

The diagram below shows the strategic positioning of the firm.

Some things I like about Ping An;

Ping An invests 1% of its revenues into R&D on an annual basis. This amounts to approximately 1.7 billion US$. This has enabled it to build first in class capabilities in blockchain technology. Ping An’s One Connect is the largest commercial blockchain application in the world with over 44,000 nodes offering services such as trade finance and custody;

Ping An just like Zhong An launched a full stack health offering called Ping An Good Doctor. Good Doctor has just over 300 million clients in China and processes just shy of a million consultations per day;

Ping An is the largest car insurer in China with over 55 million vehicles insured;

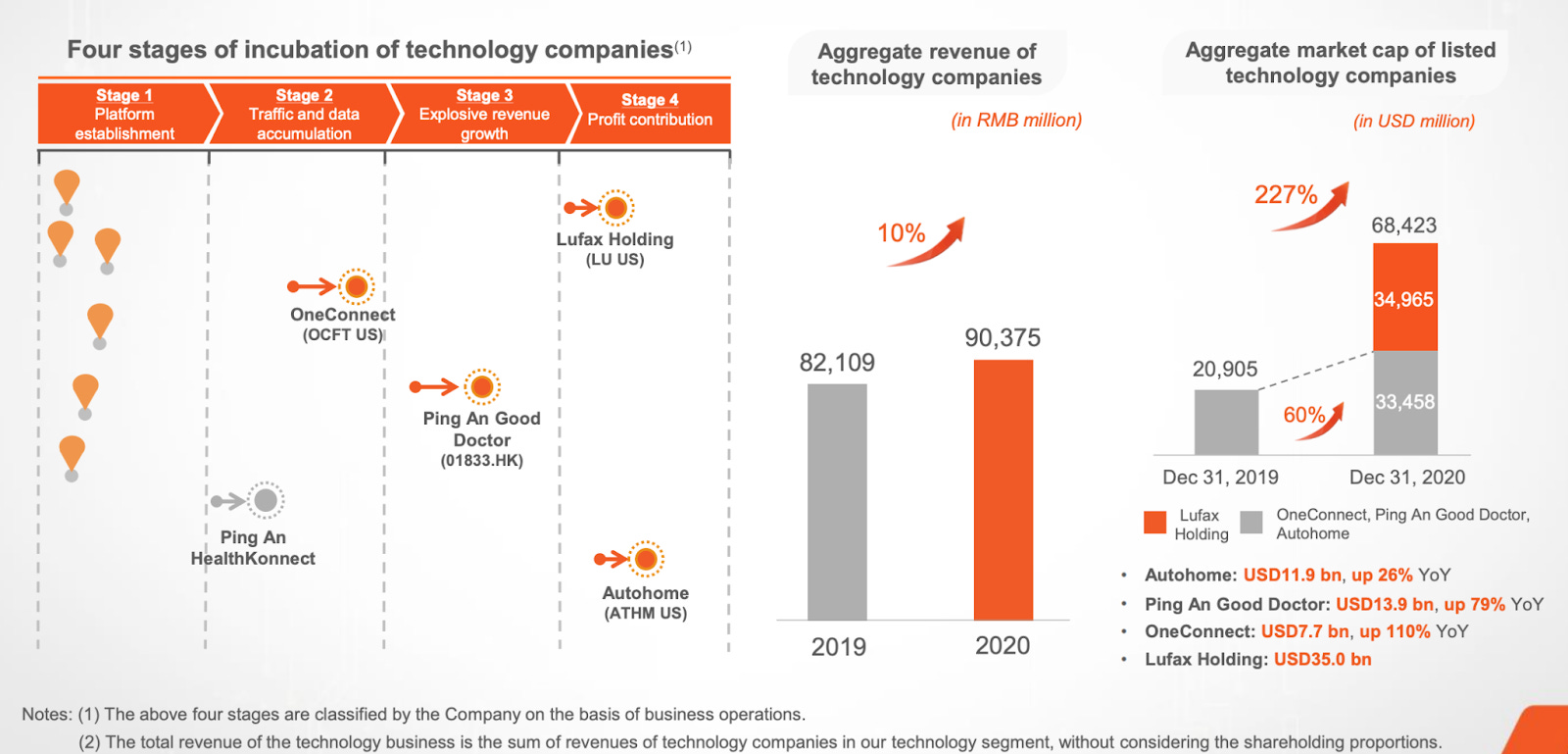

The slide below shows how Ping An thinks of its businesses. At core, an idea first of all has to have data generation capabilities that can then be transformed into explosive growth and better unit economics vis-a-vis incumbent businesses. One Connect, Good Doctor and its autohome business are worth US$ 7.7billion, 13.2 billion and 11.9 billion respectively. This is a very good podcast on Ping An.

Metromile

Metromile is a pay-per mile insurer based in the USA. The idea is simple, given the uniformity of insurance premiums across demographics, there is cross-subsidisation between low mileage drivers and high mileage drivers. In essence, low mileage drivers are low risk based on the idea that there is a positive relationship between miles driven and probability of an accident. Metromile uses telematics and big data to analyse your driving behaviour thereby enabling you to save on your insurance policy if you are a low mileage driver.

Just like ZhongAn insurance, Metromile has two lines of business, insurance and technology export. Overtime, the more data it collects on its customers, the better it can price risk and the more profitable it can be based on its combined ratio. Additionally, the cost savings it provides its customers coupled with first in class customer experience should increase its Net Promoter Score thus reducing its long-term customer acquisition costs.

Some things I like about Metromile;

The model seems to work, the loss ratio has reduced from 101% in 2016 to 57% in 2020 showing that its data models are leading to better underwriting decisions;

In addition, Metromile has best in class contribution margins defined roughly as total income minus total expenses including claims and tax adjustments. This has grown to 13% in 2020 from a low of -25% in 2016. Already, Metromile has positive unit economics in a market worth US$ 250 billion;

In a changing world, Metromile is best placed to take advantage of major themes such as mobility as a service, telematics and the ubiquity of smartphones;

Other companies worth a mention;

Pineapple Insurance - General insurer based in South Africa that is fully mobile based covering car insurance and home content insurance. It uses a sleek user interface and intuitive customer journeys whilst partnering with Old Mutual on the back end;

Naked Insurance - Another South African insurer employing an almost similar model to Pineapple insurance.

Luko - A french company offering home insurance via your smartphone;

Tractable - A company utilising deep learning and computer vision to assess real world damage thus helping insurers assess damage and claims;

Sureify - SaaS tools for insurers helping them to digitise their operations;

Some Thoughts;

Digital transformation in the insurance sector in Africa will soon be a matter of life and death. Companies like ZhongAn and Metromile are exporting their tech and soon start-ups will be able to offer consumer value propositions that are magnitudes of times better than existing propositions. The drive to transform should be at the forefront of board thinking in incumbent insurers. One of my friends says that “in tech there’s no FUBU (for us by us)” alluding to the fact that tech converges towards global standards and insurers need to approach their tech efforts with the same attitude;

Embedded insurance will be a key vertical in the coming years and moves by companies like Safaricom towards this sector validates this. Insurance being a commodity product at core should be embedded within customer journeys in a more intuitive manner. This includes embedding it in digital commerce and banking and finance. Bancassurance for instance is a form of embedding insurance in products such as mortgages and car loans but the experience is awful;

Insurtech is a very promising vertical in Africa for two main reasons. Firstly, there is very low penetration pointing towards significant growth potential and additionally, the incumbent system is antiquated and ripe for disruption.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@gmail.com;

Well written , clear understanding that Insurance needs to be embedded as a protection element or a savings element.