Sponsored Article - Mambu and Composable Banking

Analysing the factors that are driving demand for Composable Banking and the Mambu Value Proposition

Sponsored Post

People want more flexibility in how they interact with financial services than ever before, and changes in consumer behaviour mean it's time for banks and financial providers to adapt to meet growing demand.

Legacy tech infrastructures and outdated core banking platforms are stifling innovation. Banks, lenders, fintechs, telcos, and even retailers, are turning to SaaS cloud core providers like Mambu to help them build modern digital financial products faster, securely and cost-effectively.

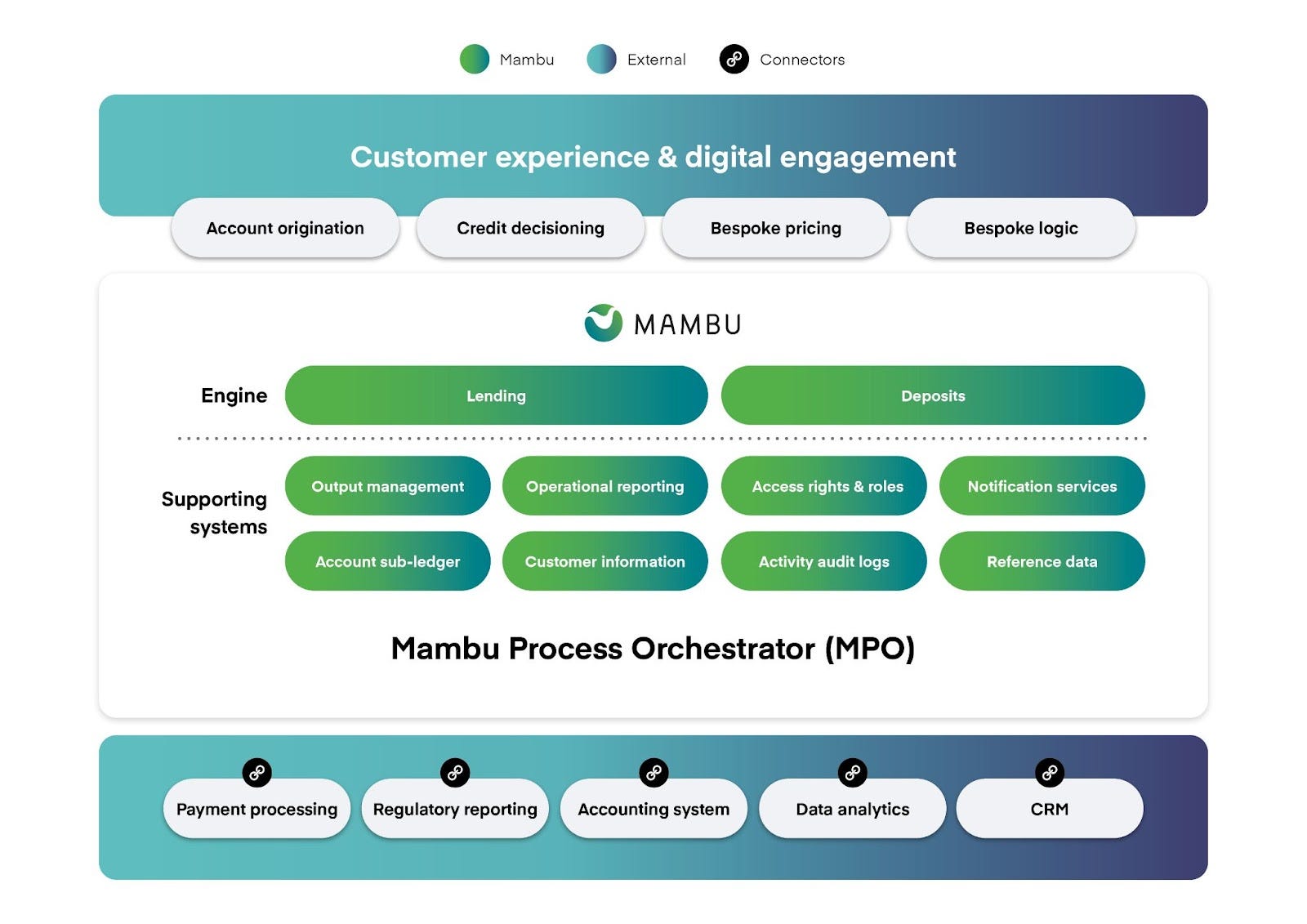

Mambu makes it possible for banks to innovate at speed through an approach called composable banking. This allows for independent components, systems and connectors to be assembled in any configuration to meet business requirements and the ever-changing demands of end customers.

A robust marketplace ecosystem offers integrations across credit decisioning, payment processing, AML, KYC, regulatory, CRM, accounting, customer experience and more. This extensive network gives you unrivalled vendor flexibility and no lock-in. Not only that, Mambu works with all major consultancies and SIs to ensure a smart and strategic cloud deployment.

To learn more about how Mambu can transform your bank or financial institution through a composable core platform, visit www.mambu.com.

Introduction

Banks across the continent are having to make strategic investments in technology and their customer propositions to stay relevant in an ever changing industry. It is quickly emerging that banks have to evolve and adapt otherwise their survival is at risk over the long term. In Africa, banks are still profitable but taking Nigeria, Kenya and South Africa as an example, ROE’s in these markets have been declining. In Kenya for instance, the average ROE’s have declined from 30.9% in 2011 to 22.2% in 2019. 2020 of course was bad for every bank due to the Covid-19 pandemic. Globally, these shifts have been gradually happening since the global financial crisis that took place over a decade ago, bank valuations have been stagnant due to a number of headwinds amongst them; increasing capital requirements brought about by regulators, a low interest rate environment as well as a fundamental shift in how people access financial services brought about by a rapid change in technology.

This latter factor has been encapsulated in the term “Fintech” with Fintech in this sense including crypto-currencies and Decentralised Finance (De-Fi). Fintech has been a major disrupter to the traditional banking business model. According to KPMG, total VC investments into Fintech in H1 2021 totalled US$ 150.6 billion. In H2 2020, the corresponding amount was US$ 109.5 billion reflecting an increase of almost 50%. In Africa, over US$ 330 million was raised in the first half of 2021, an amount that was almost double what was invested in all of 2020. Capital and talent are flowing into Fintech with new players picking away at the revenue pools that have been exclusively owned by banks from payments to remittances to lending.

In addition to this, a number of challenges ranging from cultural to regulatory challenges hobble banks when it comes to evolving their business models. A major consideration for banks will be how to deploy their technology so as to best position themselves in their respective markets for future growth. In Africa, this will come with its own unique set of challenges which present both a threat and an opportunity. This article will discuss the context in which African banks must operate, the idea of composable banking and how banks can partner with Mambu, the global leader in the composable banking framework to future proof their business.

Banking in Africa - A Never Changing Landscape

Banks are having to negotiate a number of challenges from technology to demographics to underwhelming valuations across the board. It’s often that you hear a bank CEO or Chairman in Africa saying that “we have a fantastic business, but the market doesn’t value us properly”. As Ben Graham said, “In the short run, the market is a voting machine but in the long run it is a weighing machine.” The valuations of African Banks in the market have been stagnant for over 10 years, clearly 10 years is long enough to reflect that the market is operating in its capacity as a weighing machine. So what are the challenges?

Technology

I was once having a chat with an experienced banking leader. He spoke about his career in banking and how different it is to lead a bank now as opposed to thirty years ago. In his words; “30 years ago, a new innovation used to come every 10 years, 20 years ago, a new innovation would come every 5 years, 10 years ago, a new innovation would come every year or two. Now, a new innovation comes every day”. He went further to cleverly articulate that leadership now is all about knowing which innovation matters and which doesn’t, whilst also always remaining open minded.

Indeed, this is true, the only thing constant now is change and banks have to future proof their businesses. The framework for technology is deeper than just changing the underlying tech stack, it involves having a full understanding of how to organise your business around technology. Some of the considerations should involve;

Waterfall to Agile - Most of the times when people think of Agile methodology, they think about it in terms of project management. I’d venture to say that Agile is actually a commercial principle where experimentation and discovery happens in an asynchronous manner. Companies like Google and Stripe operate in an agile manner where products are released at a dizzying pace. This requires a culture change in how products are evaluated and how they are launched. Often with banks, product ideation occurs in a top down, waterfall approach whereas the execution is handed over to “Agile teams”. Being agile means the full commercial cycle from ideation to delivery to improvements should be done in one loop;

Linear vs non-linear growth - In the digital world, growth is non-linear. In the physical world, there were physical limits to what you could actually do. So for instance, the number of SWIFT payments was actually limited by how many staff you have in your payments department and how many payments they could manage. In a digital world, there is technically no limit to the growth rate. This then creates a whole different conversation about your technology decisions and in particular your infrastructure decisions. Cloud technology is native to the digital world. Most leaders who are adopting cloud are effervescent in their praise for Cloud, the popular statement being that the costs may be high, but I never have to worry about downtime and capacity;

Constant change - Banks have operated for a long time based on 5-10 year strategies. Inherent in these plans is an assumption about many things remaining constant. In the modern world, change is the only constant. Jaco Fourie, the Managing Director for Africa at Mambu aptly says that “in the past, banks were built to last, now they must be built to change”;

APIs as the glue holding together the digital economy. APIs or Application Program Interfaces are essentially standardised communication protocols that enable two systems to communicate. They are the new plumbing in the global economy and must be a key consideration in any product or technology strategy. APIs help companies to abstract the complexity of any product or process into a single line of code. Stripe for instance abstracts the complexity of the global payment system into one line of code thus enabling any developer to create global payments acceptance on any website. The biggest value add for APIs is their ability to enable companies to seek out best in class capabilities and integrate them into their product.

Demographics;

Africa has a very young population. The median age is 19.7 years compared to Europe, USA and China with median ages of 43.7, 38.1 and 38.4 respectively. This not only shows the massive opportunity in the financial services space, but it also shows the threat of maintaining traditional banking channels. The younger generation particularly, Gen-Zs are the first truly digitally native generation. This generation came of age when Facebook, Instagram and Whatsapp were mature products. Millennials experienced the pre-web2 era and so are not as digitally native as the huge African Gen-Z cohort.

Gen-Z’s will just not relate or empathise with traditional banking products. They are used to seamless, personalised and relevant digital experiences and the instant gratification that comes from a fully digital experience. It won’t be enough to digitise, banks will have to be fully digital. This will be particularly the case with vectors such as Retail and SME banking where digital experiences will have to be intuitive and fit for purpose.

The current Group CEO of Equity bank best captured this in his 2019 annual letter to investors.

...We took note of the fact that our external context is changing rapidly given two key factors, technology and demographics. For several decades, the banking sector’s business model had been relatively unchanged, hinged on brick and mortar branches and client facing services. This has changed radically in the last few years with technology enabled channels becoming the main means by which clients interact with financial products and services… This wide generational spectrum presents challenges and opportunities in terms of delivering relevant products and preferences of channels. While our legacy customers prefer to use branches and engage directly with the bank through people facing functions, the younger generation is interested in convenient channels that empower them to conduct their own affairs anywhere anytime. Today we are engaged with a large and growing demographic that wants to consume banking in a different way and views financial services not from a utilitarian perspective but from an experiential and value perspective.

Catering to this demographic space will require a complete rethink of how you service and maintain your clients.

A Changing Economic Paradigm

Proclaiming a paradigm shift in how things work is often ridden with pitfalls. Prophecies of change have often been proven wrong or premature. As they say “the more things change, the more they stay the same”. Nonetheless, societal change in the past has largely been driven by technological change. The shift from the agricultural revolution to the industrial revolution was powered by new technologies such as the steam engine and electricity.

5G, Machine Learning, Big Data and Artificial Intelligence are the big innovations that are powering the shift from an industrial era to an information era. One of the likely consequences will be another structural shift in how labour organises with us potentially seeing a shift back to a smaller share of wage labour. In fact, Mario Gabriele in an article for his newsletter “The Generalist” noted that as late as 1820, just 20% of the American workforce was organised through wage labour. Fast forward to 1950 and over 90% of the workforce was organised through wage labour. This had 2nd and 3rd order consequences across the economy with one of them being the standardisation of retail banking built on financing the “salary”. As we move into the information age, we may see a shift back towards less wage labour. Covid-19 has accelerated this trend. According to the St. Louis Fed, there were over 9.6 million unfilled job vacancies in Q2 2021 up from 5.4 million in a similar period last year. In some quarters, this is being called the Great Resignation. A lot of people are realising that gig work as well as online work can be fulfilling and lucrative at the same time.

My niece, for instance, finished studying to be a chef. As she waited to get a job, she started using social media to show off her cooking skills and share the different recipes she uses. Soon, this morphed into a business where she would take orders and deliver ready cooked meals to her clients. The revenue she’s currently generating from this is powered by improved search and discovery via social media, cheap communication tools through Whatsapp and transport and delivery infrastructure that is easily coordinated through a smartphone. In essence, it’s very easy to start a food delivery business now vis-a-vis 20 years ago. This is making her question the logic of whether to get employed. Across her generation, similar thinking is occurring with skilled workers such as graphic designers, data scientists, engineers, writers, photographers and artists.

Just like in the past, the 2nd and 3rd order effects will involve a change in how banking is done and how clients are served. At the core of this will be improved data capabilities to power innovative lending as well as constant product innovation.

Legacy Technology and Culture

Following on from the previous point, legacy technology and thinking still pervades the industry. From a technological perspective, there are a number of elements holding back large parts of the industry from evolving;

Older Core Banking systems were built for branch-based banking with customisations and workarounds being created to handle modern digital banking propositions. These led to significant technical debt as well as high maintenance costs. For instance, traditional vendors sold and serviced API middleware often at very high costs;

Existing solutions architectures were built around siloed data thus hampering product innovation, customer experience and personalisation;

Client-server and on-prem architectures led to expensive maintenance budgets whilst at the same time lowering performance particularly during peak demand such as end of month;

Vendor lock-in over multiple years was and continues to be an anchor to product innovation;

These technology decisions have created an adverse path dependence. Given that it took significant expertise to maintain these byzantine systems, and that this expertise has moved up the decision making chain of the organisation, legacy technology has led to legacy culture. One way this manifests is in how the leadership in many banks think about core banking. For example, many banks still operate in the framework of having one big bang core banking transformation despite the significant risks inherent in such processes. Not only is it risky, in many cases it’s not even necessary

For instance, the demands of a corporate bank differ vastly from the demands of an SME bank. If you are a universal bank, it’s not necessary to move all your business lines to one core banking system. In fact, it’s expensive and redundant. A corporate bank may need a basic core banking system, an advanced payments engine and maybe a digital banking platform. A retail bank may need more advanced technology particularly for elements such as remote account opening and personalisation. If you separate these two, you will likely lower your cost given that you would reduce the number of “user licenses” or “per account licenses” with your existing CBS vendor. Nonetheless, the prevalent thinking is still based on big-bang core transformation despite the fact that the different business lines will move at different speeds when it comes to innovation.

With this in mind, a modern approach is based on having shared services and technology in the form of an Aircraft Carrier whereas different business propositions can have their own nimble tech stacks in the form of a speedboat. In essence, there’s a reflexive relationship between legacy tech and legacy culture.

Mambu and Composable Banking;

What is Composable Banking;

The idea of composable banking is quite intuitive once you internalise the factors above that were used to contextualise the current environment facing banks. If best of breed capabilities are abstracted through APIs and customers are coming to expect increasingly better experiences from their service providers, then service providers need to be able to orchestrate best of breed capabilities across their product stack. Shopify for instance uses Stripe for payments acceptance whilst using Twilio for messaging and communication. Both of these providers are best of breed and both connect via an API. This enables Shopify to focus on building a world class experience for both merchants and shoppers on its platform.

The idea of best of breed functionality has actually existed in other industries without the glue of APIs. Formula 1 is a perfect example. In F1, constructors combine best of breed capabilities to try and win the F1 championship. There are many elements that go into creating a winning team, from the choice of engine to the choice of brake pads to gearboxes and electronics. Red Bull for instance uses Honda for their engine while using Brembo for their brake pads. Through the clever combination of best of breed capabilities, the team at Red Bull can focus on other elements such as driver recruitment and racing strategy to compete for the championship.

Similarly, modern technology allows banks to build out best of breed capabilities that are fit for purpose and fit for time. This allows them to focus on what matters most to compete in the market, including product innovation, marketing and strategy. Underlying all this is the fact that vendor selection must be well structured. The bedrock of any composable banking framework is the choice of core banking platform. The core banking platform has to be able to support this through a rich API ecosystem.

Mambu

Mambu traces its history to Africa actually. It started off as a project by three students from Carnegie Mellon University who were working on their Masters projects. The three students were Eugene Danilkis, Frederick Pfisterer and Sofia Nunes. During the course of their work in Mozambique, they realised that financial inclusion in many parts of the world is held back by inappropriate, not fit-for-purpose technology. The thinking was that with built for purpose banking technology, banks, micro-finance institutions, and lenders could offer appropriate finance and lending products.

In 2011, the co-founders launched Mambu to provide a cloud based core banking platform through a Software as a Service model. Initially, the product was targeted at micro-credit institutions quickly being accepted and lauded by regulators in over 30 countries. Nonetheless as the product matured and Mambu gained recognition, larger banks, challenger banks in Europe and USA as well as Fintechs signed on to the Mambu Platform. Led by current CEO and co-founder Eugene Danilkis, Mambu has grown to over 800 staff spread across over 15 offices worldwide including Amsterdam, Berlin, Abu Dhabi, Miami and Singapore. Mambu is considered the leading SaaS based core banking engine in the world with clients such as ABN AMRO, N26, Solarisbank, TymeBank and Oaknorth.

Mambu has over 30,000 product configurations, processes over 100m API calls per day and serves over 50m end customers. Since its inception, Mambu has raised over US$ 152 million including a US$ 135m Series D early in 2021 that raised its valuation to nearly US$ 2 billion.

Mambu’s Value Proposition;

There are many factors that drive Mambu’s powerful value proposition.

Mambu’s solution is cloud native and born in the cloud. What this means is that unlike traditional vendors, there are no legacy migration journeys into the cloud and thus Mambu has an API for every function. In my view and from my experience, this needs to be the most critical factor in the evaluation of a core banking vendor. To innovate, what you need is that every action that happens in the Core System has an API. For instance, there needs to be an API for the full account cycle from opening, to dormancy to closure. In the absence of such assurances, technical teams have to conduct expensive evaluations during the RFP phase to ensure that they can access the APIs that they will need. The issue with this approach is that you don’t know which APIs you may need in a year’s time so inevitably, this may not work. If a solution is API-first and genuinely cloud native then you can sufficiently future proof your business. Mambu is additionally available across all major cloud platforms i.e. AWS, Google Cloud and Microsoft Azure. This is largely a commercial decision as customers may have their own preferences as to the cloud system they want to work with. The benefits of being cloud native extend to the following;

Source: Mambu

Mambu has strategically focused on the core engine, in this case being the ledgers, basic customer data and the product factory. These are the core capabilities of the systems of record and they are available through very powerful APIs. This hyper focus on the core system combined with being cloud native, has a number of benefits;

There’s no vendor-lock in across your tech stack as you can work with any vendor that is fit for purpose and switch them out via APIs. For instance, if you’re in Nigeria, you can quickly switch between Flutterwave, Paystack and Paga for payments depending on what works best for you;

Given that the system is cloud native and is a single code base, Mambu can push updates to the system on a weekly or even daily cadence enabling all its clients to have access to the latest functionality. During Covid-19 for instance, regulators in India required that banks offer their customers repayment holidays on their loans. Through a simple upgrade, Mambu was able to push this functionality to all its customers. This is unlike legacy vendors who have a 5 year upgrade cycle;

A thin-core cloud based framework enables it to handle multiple account permutations thus powering numerous business cases;

Geographical expansion does not have any major licensing implementations and a new subsidiary can be put up in the click of a button;

Being cloud native whilst focusing only on it’s core allows Mambu to have availability of 99.99% which is embedded into the SLA’s signed with clients;

Long-term savings in OPEX due to lower hardware and staff costs as all workloads are on cloud. Indeed, cloud deployments are expensive, but on-prem deployments are arguably more expensive when seen from a like for like perspective, particularly as regards to maintaining staff who will manage cybersecurity risk;

Mambu’s Process Orchestrator (MPO) - The MPO is a built-in middle-layer between different systems that enables a client to pull, process and push data via APIs. It operates through a drag and drop user interface enabling a low-code product development framework. This is quite different from legacy core systems where product creation requires specific technical expertise including leveraging consultants recommended by the core banking vendor. In an era of rapid product innovation, having a low-code product development middle-layer such as the MPO is critical for innovation. New business models such as BNPL are emerging and Mambu can enable a bank to rapidly create a BNPL product through the MPO and quickly test it out and launch. In fact, Mambu’s quickest implementation was 14 weeks. Read more about MPO here;

Source: Mambu Developer Documentation

Mambu’s advanced architecture significantly improves processes such as EOD (End of Day) processes. EOD configuration happens at the implementation stage and the system will automatically run jobs based on your configuration. Some jobs can be done hourly and others will be done at the end of day. Upon configuration of your time zone, an automated EOD will run at midnight every day. EOD will run asynchronously to your normal jobs and thus you can continue to process your transactions whilst EOD is running. Streaming architecture allows jobs to be run both as batches as well as through real time streams. Read more about Mambu EOD Jobs here and here;

Source: Mambu Developer Documentation

Mambu has supported various use cases and thus is a powerful platform for a bank that has a multi-product, multi-vertical strategy. Mambu for instance powers Solarisbank, a leader in European Banking as a Service. Oaknorth offers SME Lending where Mambu powers its core ledgers whilst Oaknorth focuses on its credit scoring and decisioning engine. In Africa, Mambu is powering TymeBank which is the leading Neobank in South Africa. TymeBank has grown to over 3 million customers, opening between 100,000 and 200,000 accounts per month.

How to Onboard onto the Mambu Platform;

A modern core banking solution requires a different approach to onboarding and customer success. Onboarding onto a cloud-native core banking platform is a long-term decision and thus, an organisation must ensure that there is long term strategic alignment.

Value Proposition Definition;

With offices around the world, Mambu is able to offer its services across a number of time zones. Africa falls under the EMEA region and is served through South Africa, Amsterdam and Abu Dhabi from a resource perspective. Each Mambu engagement begins with three teams;

Solutions Engineering;

Customer Value Creation team &;

Research and Development team;

These teams work with a client to define the consumer value proposition that will be built, be it an SME, BaaS or Retail proposition. Advisory and R&D teams work with the clients to architect a solution that aligns with the organisation's long-term strategy. A key decision framework behind this approach is to ensure that the technological choices made align with the commercial strategy taken. At this phase, a client can ask all the relevant questions, particularly as it pertains to how future strategic pivots can be supported by the proposed stack.

Key Dependencies

Projects often fail because the core dependencies that are required for successful project implementation are lacking. For a successful Mambu implementation, the following are required;

A clear requirement of what the organisation is trying to achieve from a commercial perspective and it’s preferable that this is documented and signed off to avoid the inevitable undocumented permutations that arise whilst whiteboarding;

Sufficient staffing to ensure that the project is successfully executed. These include product teams, engineering staff and DevOps people;

Sufficient internal staffing to maintain the system post implementation without an overreliance on the vendor. Mambu undertakes thorough pre and post implementation training with each deployment being availed a customer success manager;

Well defined target architecture - Mambu helps through the customer value proposition teams as well as the solutions architects;

The organisation at pre-implementation has to map out the ecosystem partners to ensure that the solution is actually viable;

Partners and Ecosystem;

Mambu is developing and managing a growing partner ecosystem. Current players such as Form3, Backbase, Onfido and ComplyAdvantage are technology partners. The full list is available here. Within Africa, Finplus is the main consulting and systems integration partner. Nonetheless, Jaco Fourie is scouting and growing the partner ecosystem.

However, as a fully API based system, any bank or Fintech can easily integrate existing systems to Mambu due to its easy to use API documentation. For instance, an implementation in Kenya can be done to Pesalink, M-Pesa, IPRS and any other relevant partner whilst front-end engagement layers can be built by any Fintech in the market. Kwara for instance has built a fantastic SACCO product that helps SACCO’s digitise. Using Mambu’s lean core, Kwara has built out the front-end and consumer apps whilst performing integrations to local payment partners.

Thoughts on Regulation;

Mambu is only available on cloud and this can cause a conundrum particularly in many African countries where cloud deployments are not yet approved by regulators. This is an ever evolving target given that a number of regulators are starting to see the value of cloud, particularly due to its ability to power low-cost and reliable financial services. My general view is that on-premise deployments don’t give you the power of cloud, particularly the freedom it gives to fully focus on your business.

Nonetheless, given that it’s a composable banking framework, some workarounds could include maintaining customer data on-prem through an on-prem CRM solution whilst running the ledgers and product factories on cloud. Some banks have adapted to the regulatory constraint through this approach. Having said that, banks and fintechs should proactively engage regulators so as to ensure that working guidelines around cloud computing can be developed.

Way Forward

If you’re a Registered Bank, Micro-Finance Institution or Fintech looking to modernise your technology stack whilst evolving into a customer-centric organisation, then Mambu should definitely be part of your consideration. Whether you want to launch a BaaS proposition, build out embedded finance on your platform, launch an SME digital bank or a modern digital consumer proposition, Mambu powers all these use cases.

Register to attend the next Mambu demo or contact sales to learn more.