#90 - The Business Case for Institutional Crypto

Evidence, risks, and winning models for banks entering the digital asset economy

Illustration by Mary Mogoi

Hi all - This is the 90th edition of Frontier Fintech. 10 more to 100 articles! A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

🚨🚨 New Sponsor Kit Just Released 🚨🚨

Want to reach Africa’s top fintech decision-makers? We’ve updated our offering with premium content, executive visibility, and strategic advisory options.

Click the link below for media enquiries

Click the link below for consulting and advisory enquiries. We’ve worked with past clients on Go-to market, market mapping, investment advisory support and general fintech strategy support.

Introduction

In New York, the political landscape is being reshaped by figures like State Assemblyman Zohran Mamdani, a democratic socialist whose platform has sent shockwaves through the city's political establishment. I watched a video in which he proposed public supermarkets to deal with the rising cost of living. Moreover, there was another video in which he said that the existence of billionaires is a sign of a broken system. The political and economic establishment came out strongly against him, suggesting that his comments and proposals were at core un-American and went against the values that made America what it is. Interestingly, the Gen-Z block i.e. voters between the age of 25 and 34, a group that includes younger millennials had the largest turn-out, representing over 40% of the voters. These voters gave him his overwhelming victory in the recent democratic primary, a marker that his message resonated. Some of the rhetoric by the political administration has been to castigate the Gen-Z block as naive and lacking knowledge. It’s like they “just need to be shown the right way”.

Across the Atlantic, Kenyan Gen Zs have spent a year openly challenging their president. What has been interesting about this protest wave has been its digital sophistication, the bravery the Gen-Zs have shown as well as the fact that it seems non-tribal. The latter has made it a complex situation for the existing political structure which traditionally has responded to any political dissent by stoking tribal biases. From a far, you can sense the confusion in the entire situation. How do we deal with this amorphous issue?

Source: Rocknheavy

At a fundamental level, what we’re seeing globally is the Gen-Z’s throwing their demographic heft around. In the 60s and 70s, boomers made their stance known through the counter-cultural revolution and this shaped much of the world thereafter. That counter-culture later inspired Microsoft and Apple’s push to democratise technology. Bill Gates' famous vision was to “put a personal computer in every desk and in every home”. A couple of generations earlier, Thomas Watson said that “I think there’s a world market for maybe five computers”. There was a generational divide in their world view.

Gen-Zs are here and they will shape a lot of what is seen as acceptable in society. Like we’ve seen in New York, they have the numbers, the sophistication and energy to shape their outcomes. Whether we agree with them is another issue altogether, that they will shape society is what matters. As Bezos always reminds us “reality is the undefeated champion”.

Why does this matter to a Fintech audience - If Gen Zs are shaping society, then financial services are designed to fit into the society that exists. A Gemini survey found that fifty-one percent of Gen Z respondents own cryptocurrency, far ahead of older groups. Gen-Zs see Crypto as a core part of their financial lives, TradFi will have to adjust and not the other way round.

The role of Gen Z in technological and financial trends is amplified on the African continent due to its unique population dynamics. Africa is the world's youngest continent, with a median age of just under 20 years, compared to a global median age of over 30. A staggering 60% of Africa's population is under the age of 25, meaning the Gen Z and Gen Alpha cohorts constitute the vast majority of its people. In countries like Nigeria, the continent's most populous nation, this youth bulge is even more pronounced. This demographic reality means that the behaviours, preferences, and adoption patterns of Gen Z are a powerful indicator of mainstream economic and social shifts across the continent. Their engagement with technologies like cryptocurrency, therefore, holds profound implications for the future of financial services in Africa.

The question then becomes, is there a case for traditional institutions like banks, asset managers and insurance companies to participate in Crypto? This article will cover the issues that a typical TradFi business case would cover and hopefully help leaders think more clearly around where Crypto fits into their long-term strategies. Financial services have to adjust to the societies they serve, if crypto adoption is growing, it only makes sense for banks to take this trend seriously. The article will cover;

Global trends in crypto adoption - Social Proof;

Regulatory drivers for Crypto Adoption in Africa - Regulatory Cover;

A review of the demand drivers if any - Commercial case;

A review of the maturing institutional crypto infrastructure industry - What will it take;

What business models banks can leverage with Crypto - think payments and institutional custody - How do we play?

How do we think it will evolve - What’s our right to win?

Global State of Play

Globally, the Crypto industry is moving from a niche sub-sector of financial services to a more mainstream adoption. This is playing out in the form of both regulatory changes as well as incumbent organisations making increasingly bold moves in the space. Overall, it’s impossible to ignore the trends.

Proven business models from leading financial institutions and landmark regulations have established a clear blueprint for entering the digital asset market, significantly de-risking entry for other institutions. We’ll look at what global tier 1 banks are doing, what global Neobanks are doing and how global crypto regulations are evolving.

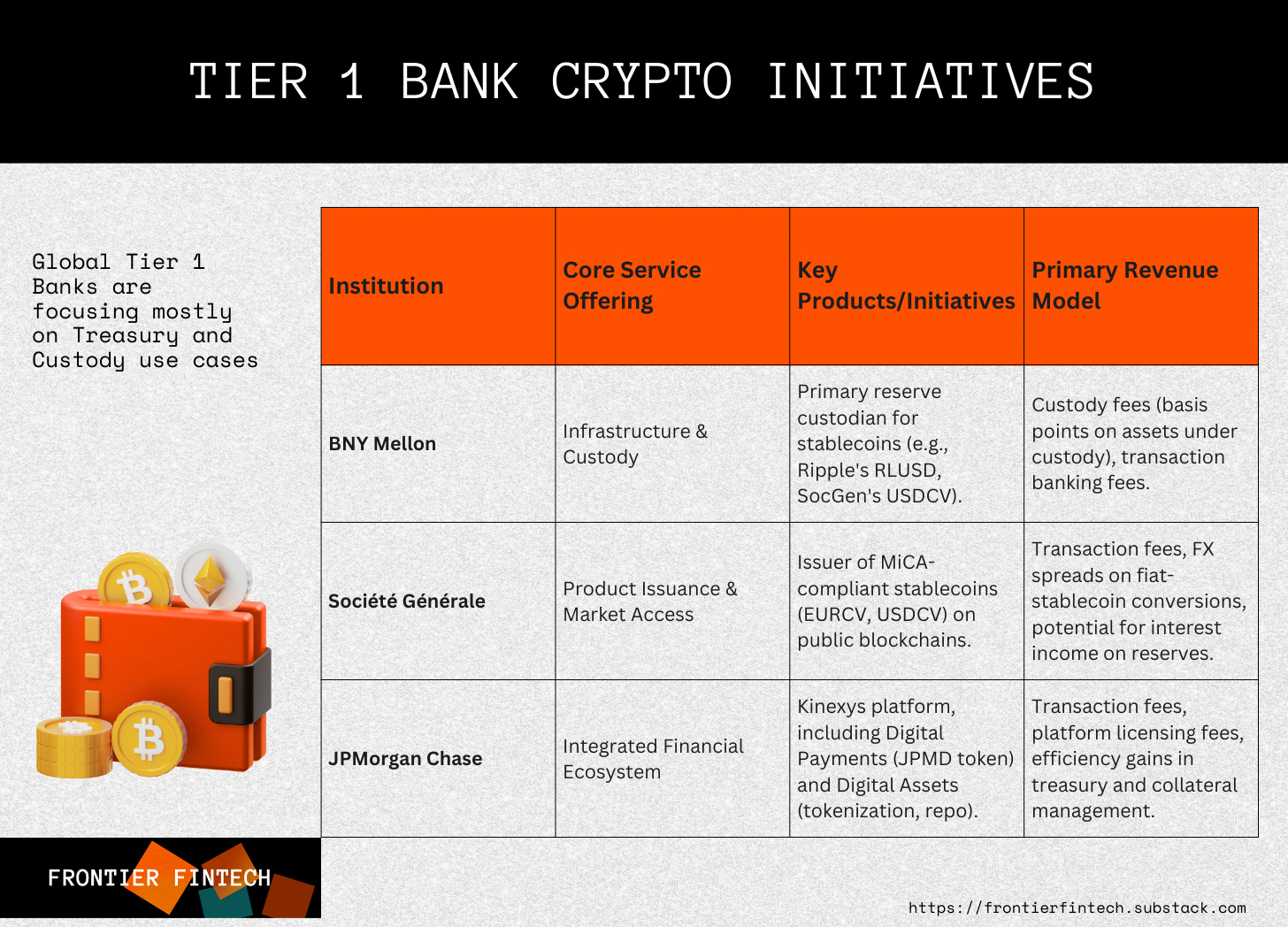

Tier-1 Banks: Building Institutional Infrastructure

Global banks are actively building the foundational rails for digital finance, offering replicable strategies that range from low-risk infrastructure plays to fully integrated ecosystems.

BNY Mellon: BNY Mellon monetises its asset-servicing expertise by safeguarding stablecoin reserves, earning custody fees with minimal market risk.

Société Générale: Through its subsidiary SG-FORGE, it demonstrates a product-issuance model. It offers its own MiCA-compliant stablecoins (EURCV, USDCV) on public blockchains for institutional uses including payments, on-chain settlement, and cash management.

JPMorgan Chase: The Kinexys platform represents the most advanced model. This proprietary blockchain ecosystem has already processed over 1.5 trillion in notional value with average daily volumes exceeding 2 billion as of early 2025, offering high-value programmable payments and asset tokenization.

HSBC and Ant Group have experimented on Corporate Treasury payments riding on Ant Group’s Whale blockchain. Deutsche Bank have also worked with Ant Group.

In Africa - Absa and Standard Bank Group have both made announcements around their participation in Crypto with both seemingly looking to start off with Custody services.

Large Tier 1 banks seem to be focusing on the Custody or Treasury use cases of Crypto. JP Morgan is definitely worth watching because they could build powerful trusted infrastructure for global money movement that slowly phases out SWIFT.

Neobanks: Driving Retail and Super-App Integration

In parallel, leading neobanks are focusing on retail adoption by integrating digital assets directly into their user-friendly platforms, leveraging their large customer bases.

Revolut: Acts as a key on-ramp by integrating crypto trading and staking services directly within its financial "super app," providing seamless mobile-first access.

Nubank: Has embedded cryptocurrency trading into its core banking app in Latin America and launched its own loyalty token (Nucoin) to deepen customer engagement.

Kakao: Leverages its dominant messaging app in South Korea to integrate a crypto wallet and promote its Klaytn blockchain platform, driving adoption through its massive existing user base.

It seems Neobanks are focusing on making crypto-exist with the rest of your financial products.

Global Regulators: Establishing Clarity and Confidence

Regulatory developments, particularly in Europe, have been a primary catalyst for institutional confidence. The European Union's Markets in Crypto-Assets (MiCA) regulation, fully effective since December 2024, is the world's first comprehensive legal framework for this asset class. It replaces a fragmented and uncertain landscape with a single set of rules for service providers and stablecoin issuers, alongside robust consumer protection standards. By transforming crypto into a formally recognized and regulated asset class, MiCA provides the legal certainty required by corporate boards to approve strategic initiatives, setting a global "gold standard".

Just as GDPR set a template for global privacy rules, MiCA is likely to guide other crypto regulators.

Africa’s Regulatory Heat Map

Across Africa, a clear shift towards formal regulation of digital assets is underway, driven by a pragmatic need to oversee massive, pre-existing grassroots demand. Key economies are moving decisively to create structured legal pathways, reducing the ambiguity that previously hindered institutional involvement. As we’ve always argued, governments deal with facts and the facts are that African countries are playing an out-sized role in crypto adoption. According to a recent Chainalysis report, Africa received US$ 125 billion in crypto value with Nigeria leading the pack with close to US$ 60 billion. Such numbers can’t be simply brushed away. Three years ago, this Quartz article showed how Kenya was leading the world in P2P crypto activity. For African regulators, the approach is, better regulate it in an orderly manner than let it go on in an unregulated manner.

South Africa: A regional leader in regulatory clarity, South Africa declared crypto a financial product under the FAIS Act in October 2022. The FSCA began licensing Crypto Asset Service Providers (CASPs) in June 2023, approving 248 of 420 applications by December 2024.

Nigeria: Representing the most dramatic regulatory reversal, the Central Bank lifted its 2021 ban on banks servicing crypto firms in December 2023. The SEC is now the primary regulator, a role formalized by the Investments and Securities Act (ISA) 2025, which classifies cryptocurrencies as securities.

Kenya: The country's positive regulatory direction is evident from the Capital Markets (Amendment) Bill, 2023, and the proposed Virtual Assets Service Providers (VASP) Bill 2025. These legislative proposals aim to define digital currencies as securities under the purview of the Capital Markets Authority (CMA), establish a formal licensing regime for crypto platforms, and introduce a clear tax framework. The move is intended to bring the millions of Kenyans already trading crypto into a supervised environment, providing legal recognition for the asset class and paving the way for regulated financial institutions to offer digital asset services.

Stances in Other Key Markets

Mauritius: The nation offers a comprehensive framework under its Virtual Asset and Initial Token Offering Services (VAITOS) Act of 2021. The Financial Services Commission (FSC) provides clear licensing for Virtual Asset Service Providers (VASPs), positioning Mauritius as a well-regulated fintech hub.

Namibia: With its Virtual Assets Act of 2023, Namibia appointed the Namibia Financial Institutions Supervisory Authority (NAMFISA) to license and register all VASPs. The framework provides legal certainty and aligns with global anti-money laundering standards.

Ghana: The Bank of Ghana plans to begin regulating virtual assets by September 2025, pending a new VASP law. This move aims to provide consumer protection and legal clarity in response to growing digital asset use.

Rwanda: A draft law introduced in March 2025 aims to regulate virtual assets under the Capital Markets Authority (CMA). It establishes licensing requirements but clarifies that virtual assets will not be legal tender and bans crypto mining, reflecting a cautious, risk-mitigating approach.

Egypt - Egypt still has a blanket ban against Crypto and there’s little to show that this stance is changing.

Where’s the Demand

Whilst there’s global proof of bank crypto adoption and an increasingly favourable African regulatory environment, the question is whether there’s significant demand that you can model a business case around. The top-line numbers show that there is. On-chain data reveals that Sub-Saharan Africa processed an estimated $125 billion in transaction volume between July 2023 and June 2024 alone. This activity is heavily concentrated in key hubs, with Nigeria standing out as a global heavyweight. The country processed approximately $59 billion in cryptocurrency value during this period and now ranks 2nd globally in the 2024 Global Crypto Adoption Index, a measure of grassroots uptake by ordinary people. This is not an isolated phenomenon; Kenya and South Africa also rank highly at 28th and 30th respectively, confirming that a multi-billion-dollar parallel financial system has already formed to meet real-world user needs.

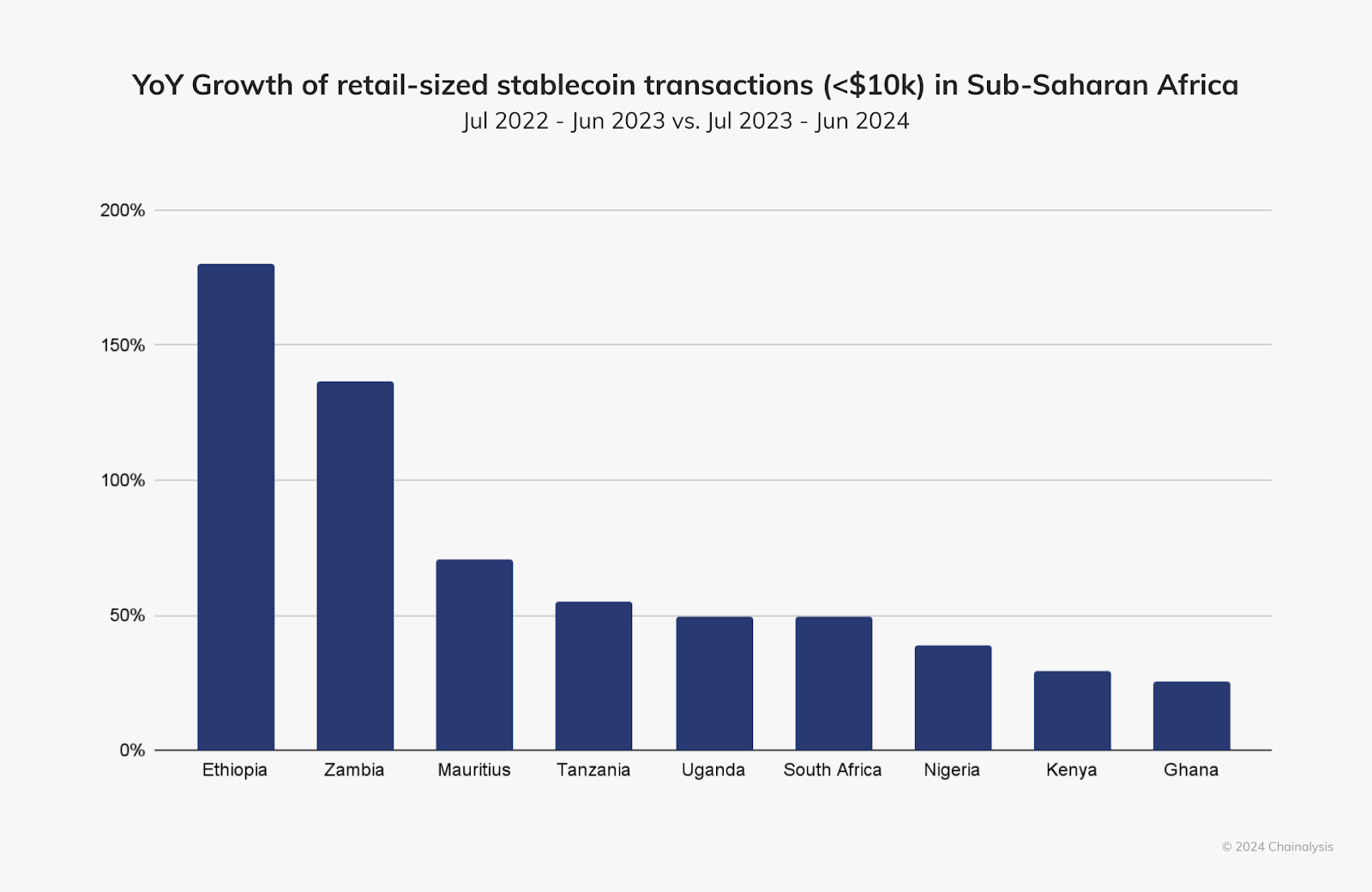

Source: Chainalysis

The graph above shows that Nigeria is an outlier in terms of Crypto volumes with close to US$ 60 billion in transaction value. South Africa follows with around US$ 24 billion and Kenya is third with less than US$ 10 billion. Stablecoins are growing as a proportion of total volumes. Whilst this is the core headline, what matters is how fast other markets are growing. From the same report, Ethiopia and Zambia were the fastest growing markets from a Crypto adoption perspective, particularly at a grass-roots level (sub US$ 10k transactions) with Ethiopia’s crypto adoption growing by 180% between 2023 and 2024.

Source: Chainalysis

Nigeria, SA and Kenya were early adopters but other markets are growing.

The clear use cases are around remittance, cross-border payments and store of value use cases.

However a cynic would have the following arguments that would all be valid;

A good chunk of these crypto numbers could reflect illicit activity. Increasingly fraudsters are using crypto to move proceeds of crime out of the economy - Why should we pay attention to this market whilst it’s obviously not serviceable? a banker would remark;

Whilst US$ 125 billion is an impressive number, African trade exceeds US$ 1 trillion and this is expected to grow. The US$ 125 billion number is around 10% of total trade, impressive but not game-changing;

Nigeria did US$ 60 billion in total crypto volumes, but this is dwarfed by the US$ 703 billion digital payments volumes in 2024;

This is the payments market. When you look at Crypto as a Store of Value, similar questions would emerge;

Outside of South Africa, other markets have relatively small pension industries with Kenya and Nigeria combined having less than US$ 50 billion in pension assets - If you compare this to the respective infrastructure deficits in these markets, it can be argued that national savings are better off going to fund infrastructure than funding crypto investments;

Whereas global institutional crypto adoption by large institutions such as BlackRock and BNY Mellon seems to be demand driven, locally it may not necessarily be the case. In the US for instance, Pension assets are 170% of GDP, note that US GDP is US$ 27.7 billion. In Kenya for instance, pension assets are less than 15% of GDP. In Nigeria, this figure is even smaller.

Therefore the cynical argument against institutional crypto adoption is somewhat valid. While the cynic's points on current volumes are valid, they represent a snapshot in time. The argument isn't that crypto will replace the $703 billion digital payments market tomorrow, but that its dramatic growth and superior efficiency in key areas, like cross-border remittances, demonstrate its potential to capture an increasingly significant share of that market. The business case is not built on today's 10% share of trade, but on the trajectory to capture 20% or 30% as regulatory clarity and infrastructure improve.

A Mature B2B Crypto Infrastructure Environment

A primary barrier to institutional adoption has historically been the perceived technical risk and complexity of handling digital assets. Today, that barrier has been effectively dismantled by a matured ecosystem of specialized, enterprise-grade B2B providers. The core infrastructure required for a bank to launch crypto services is now available as a suite of "plug-and-play" solutions, turning a daunting technical build into a manageable strategic integration. For every critical function, from safeguarding assets to ensuring regulatory adherence, battle-tested solutions now exist. Secure custody, once a major question mark, is now a largely solved problem, with firms like Fireblocks and Copper offering sophisticated Multi-Party Computation (MPC) platforms that eliminate single points of failure and are used to secure trillions of dollars in assets for institutional clients. Similarly, the challenge of compliance is addressed by blockchain analytics leaders like Chainalysis and TRM Labs, whose software provides real-time transaction monitoring and risk-scoring, allowing banks to meet AML/CFT obligations with a level of transparency often exceeding that of traditional finance.

Local players have also matured from KYC players like Smile Identity, transaction monitoring providers like Orca and forensic experts like A&D Forensics.

This matured technology stack fundamentally changes the go-to-market calculus for a financial institution. The challenge is no longer one of high-risk, in-house technical development but one of strategic vendor selection and integration. Just as a modern bank wouldn't build its own core banking system from scratch, it no longer needs to build its own custody or compliance engine. By partnering with these established providers, an institution can leverage proven, audited, and often insured infrastructure to launch services faster, with lower risk, and with greater confidence. This allows the bank to focus on its core competencies: designing compelling customer-facing products, managing client relationships, and developing a winning market strategy, rather than getting bogged down in foundational engineering.

Where to Play

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.