#89 - Mercado Pago and Embedded Finance: Charting the Next Era of Digital Lending

What Latin America’s market leader reveals about Africa’s path to sustainable digital credit.

Hi all - This is the 89th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

🚨🚨 New Sponsor Kit Just Released 🚨🚨

Want to reach Africa’s top fintech decision-makers? We’ve updated our offering with premium content, executive visibility, and strategic advisory options.

Click the link below for media enquiries

Click the link below for consulting and advisory enquiries;

Introduction

I was recently at a conference where the digital lending space was being discussed. The conference was anchored by a presentation which showed that digital lending especially in Kenya is leading to better financial outcomes for borrowers. An interesting fact emerged that over 70% of borrowers take loans for commercial reasons. However, on the sidelines of the event, a persistent issue cropped up. Borrowers were not happy with the limits that digital lending platforms set for them. The result was that borrowers, mostly small businesses, took multiple loans from various platforms to augment their borrowing. It’s an unsustainable dynamic because at core, it creates a fragmented market where no single lender can scale with their customers.

Some solutions were discussed such as open banking as a data tool that would enable better underwriting capabilities. My core argument was that unlike banks which are able to take a comprehensive view of a customer across a number of dimensions, digital lenders simply lack that central relationship with their customers. Whereas Open Banking can give data, what is ultimately required is a relationship because in a relationship, particularly a healthy one, both sides are incentivised to do the right thing.

The question then is how do you build such relationships in Africa. An obvious solution is embedded finance given that at least within Africa, this has meant a partnership between two entities. One that has the relationship and the data and one that has the balance sheet. Fuliza, a partnership between M-Pesa and Loop (NCBA) is the best example. Nonetheless, this seems to be the only game in town at least in Kenya.

If you’re building digital lending for SME’s, how do you create similar dynamics? How do you build the confidence to increase loan limits on digital lending platforms?

One solution globally has been embedding finance in e-commerce platforms such as Shopify, Alibaba and Mercado Pago. If you’re concerned about digital lending towards SME’s, e-commerce matters because it should in theory capture SME economic activity.

To this end, Mercado Libre is an extremely interesting story because within a generation, it has grown to be South America’s most valuable company worth over US$ 120 billion. Moreover, it is a world class embedded finance play with Fintech accounting for over 40% of its revenues and commercial and fintech revenues growing at CAGRs of 36% and 48% respectively over an impressive 17 years. It has enabled SME’s in South America to get access to credit and thus grow their sales.

This article will dive into the story of Mercado Libre, how they built an Embedded Finance flywheel with Mercado Pago, how the South American context contrasts with the African context and how builders and investors in Africa need to think of e-commerce driven embedded finance. The core argument is that e-commerce in Africa has been built on a fragmented framework consisting of decentralised platforms like WhatsApp and Facebook and distinct payment systems such as M-Pesa and OPay that live separately to the e-commerce frameworks. In such an environment, embedded finance becomes difficult to scale meaningfully.

Mercado Libre

It was back in the late 90s and the internet era was in full swing. Amazon had formed back in 1994, four years later, Google was founded, taking its place in a then crowded search market. Every young entrepreneur at the time wanted to build for the internet.

Source: Mercado Libre - Marcos Galperin in the middle

In Latin America, an Amazon style story was taking shape. Marcos Galperin, then an Argentinian student studying at Stanford for his MBA, felt the urge to build a tech company back home. Whilst finalising his MBA in 1999, Marcos felt that there was a need for a homegrown internet based company back in Latin America. This was particularly the case as some of the large companies like eBay were expanding globally. His then professor at Stanford Jack McDonald saw the potential in the opportunity that Marcos spelt out and helped Marcos by introducing him to John Muse who invested in Mercado Libre. This initial round was later augmented by J.P Morgan, Flat Iron Partners, GE Capital and Goldman Sachs. The total amount was US$ 7.6 million. Together with his co-founders Marcelo Galperin (his brother and CTO), Hernan Kazah and Stelleo Tolda, they set off to Buenos Aires and in the quintessential start-up approach, set-up in a garage that belonged to the Galperin family.

With money in the bank, raised largely on the back of leveraging the South American internet opportunity, there were three business models that they could pursue. There was a local Google competitor option, a Latin American Amazon or a local eBay. For Google, the local friction points either in language or context were not sufficient to create demand for a local search engine. An Amazon model would demand significant capital and Marcos was unsure whether a South American company would be able to access the same amounts of capital as an Amazon. An eBay model would work better. To start with, they faced the typical challenge that marketplaces face - how do you kick-off the flywheel? You needed “liquid products” i.e. fast moving goods, initial buyers who would drive adoption and enable growth in both buyers and sellers.

To spark early liquidity they zeroed in on collectibles such as stamps, coins, comics, and early tech gadgets like Palm Pilots and computer parts - categories where passionate buyers and sellers already existed. The team plastered posters in cybercafés across the region and paid café owners to evangelise the platform, creating a real-world viral loop that brought more buyers, which attracted more sellers, which deepened liquidity.

They experienced early growth and traction that validated their approach. By October 1999, they had 15,000 users who had transacted in goods worth US$ 2 million. Nonetheless they faced a cross-roads, the year was 2000, the internet bubble had popped and they were running out of cash. Luckily, they managed to raise a US$ 46 million round supported by Goldman Sachs - Susan Segal then of Goldman Sachs called it a miracle. This was a sobering lesson for the founding team and it shaped their approach towards profitability, a contrast to the profligacy that was characteristic of Silicon Valley startups in the dot-com bubble.

Their market place model continued to grow. In 2003, they launched Mercado Pago out of a problem unique to Latin America. Card penetration was low and so was trust in online payment methods. To solve this, they needed to create a payment solution that solved these twin issues whilst primarily supporting cash and cheques. Their solution was typical to how innovation works in the global south, leveraging on an agent network that embeds trust and accountability. When a cash buyer made a purchase online, he would be instructed to deposit money at a local agent, once this happened, the system would instruct the seller to deliver the goods ensuring that the seller could not defraud the buyer. This is not too dissimilar to the Escrow service that birthed Alipay from Alibaba. Fundamentally, it was about solving contextual problems.

In 2007, Mercado Libre IPO’d and as they say “the rest is history. Interestingly, at the time of their IPO, they still had half of the US$ 46 million they raised 7 years before in the bank. Evidence that Marcos and his team had indeed internalised the lessons from the dot-com bubble.

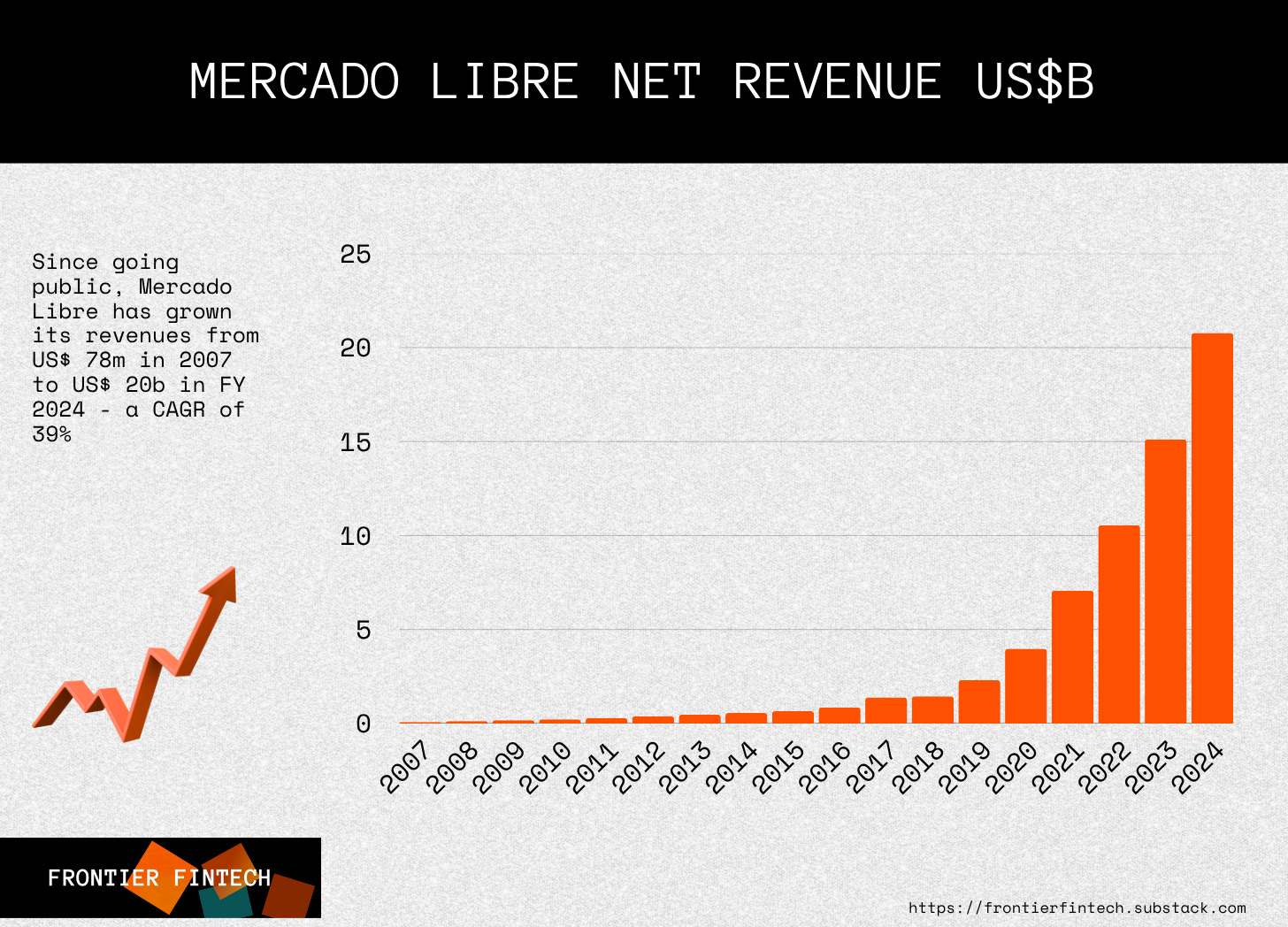

Revenue Growth - At the time of their IPO, Mercado Libre made around US$ 76 million dollars - this has grown by an impressive CAGR of 38% over the last 17 years to FY 2024. Total revenues stood at US$ 20.24 billion as of FY 2024. Their Q1 2025 revenues stood at US$ 5.9 billion reflecting a total FY 2025 number that could exceed US$ 25 billion if you consider a Q4 spike. This has been nothing short of impressive.

GMV Growth - In a similar period, Gross Merchandise Volume grew by a CAGR of 22% from US$ 1.7 billion in 2007 to slightly over US$ 50 billion in FY 2024. Q1 2025 GMV stood at US$ 13.3 billion again showing that the trend in growth will remain stellar.

Even more impressive has been the growth in payments volumes powered by Mercado Pago. These are both off-platform and within platform given that Mercado Pago is a standalone Fintech that powers broader payments outside of the Mercado Libre marketplace. Since their IPO, TPV has grown by an impressive 51% CAGR over 17 years. Currently, Mercado Pago supports US$ 194b in payments volume. If you consider that Latin America’s GDP stands at US$ 7.04 trillion, you can clearly note that there’s significant upside potential. A further growth of say 40% over the next five years would lead to a TPV of slightly over US$ 1 trillion.

Subsequently, the growth of Mercado Pago has led to a situation where Fintech revenues now account for slightly over 40% of total revenues at US$8.60 billion. Since their IPO, Fintech revenues have grown by a CAGR of 48% over the last 17 years, an impressive feat indeed. If the growth dropped down by 1000 basis points over the next 5 years, then Fintech revenues would stand at US$ 44 billlion by 2029. If Nubank is anything to go by, then this is not an impossible feat and is far within the realms of possibility.

Mercado Pago

The growth of Mercado Libre and the subsequent growth of Mercado Pago is one of the most successful embedded finance stories ever.

Simply, Mercado Libre built an engine that attracted buyers and sellers - these in turn created economic activity centred around daily life services such as shopping and commerce, which in turn created the seeds for Mercado Pago as a payments platform. Once Mercado Pago was built, it was only logical that they would go deeper into the stack. Since its founding back in 2003, it has grown to over 64 million active users and a deep product stack. Mercado Pago’s product stack includes credit services, asset management, payment services both on-platform and off-platform and increasingly comprehensive banking services particularly in Argentina.

Some core highlights emerge that show the depth of Mercado Pago’s Fintech business and how this creates a positive reinforcement loop that leads to more growth;

Its credit portfolio stands at US$ 7.7 billion as of Q1 2025 - growing by 75% from a similar period in 2024. Of this;

Credit cards account for 42% of the portfolio;

Consumer credit accounts for 38% of the portfolio;

Merchant loans account for 18% of the portfolio;

From an earnings perspective, their Net Interest Margin After Losses (Nimal) stood at 22.7%. This in a rough way shows that for each dollar lent out, they earn 22 cents on an annual basis. For context, Nubank’s Net Interest Margin in Q1 2025 was 17.5%.

From a credit quality perspective, Mercado Libre performs well. Their 15-90 day past due loans stand at 8.2% of the portfolio as of Q1 2025 and their 90 day past due default rate stands at 18%.

Mercado Pago offers savings products for its users under their Asset Management division. In Q1 2025, total AUM stood at US$ 11.2 billion dollars. Note that Nigeria’s pension industry has an AUM of around US$ 16 billion for context. Mercado Pago’s AUM grew by 102% year on year;

Their acquiring business also showed robust growth. The TPV from their acquiring business in Q1 of this year stood at US$ 40.3 billion of which US$ 26.3 billion was off-platform i.e. normal merchants who are accepting payments through Mercado Pago outside of the Mercado Libre marketplace.

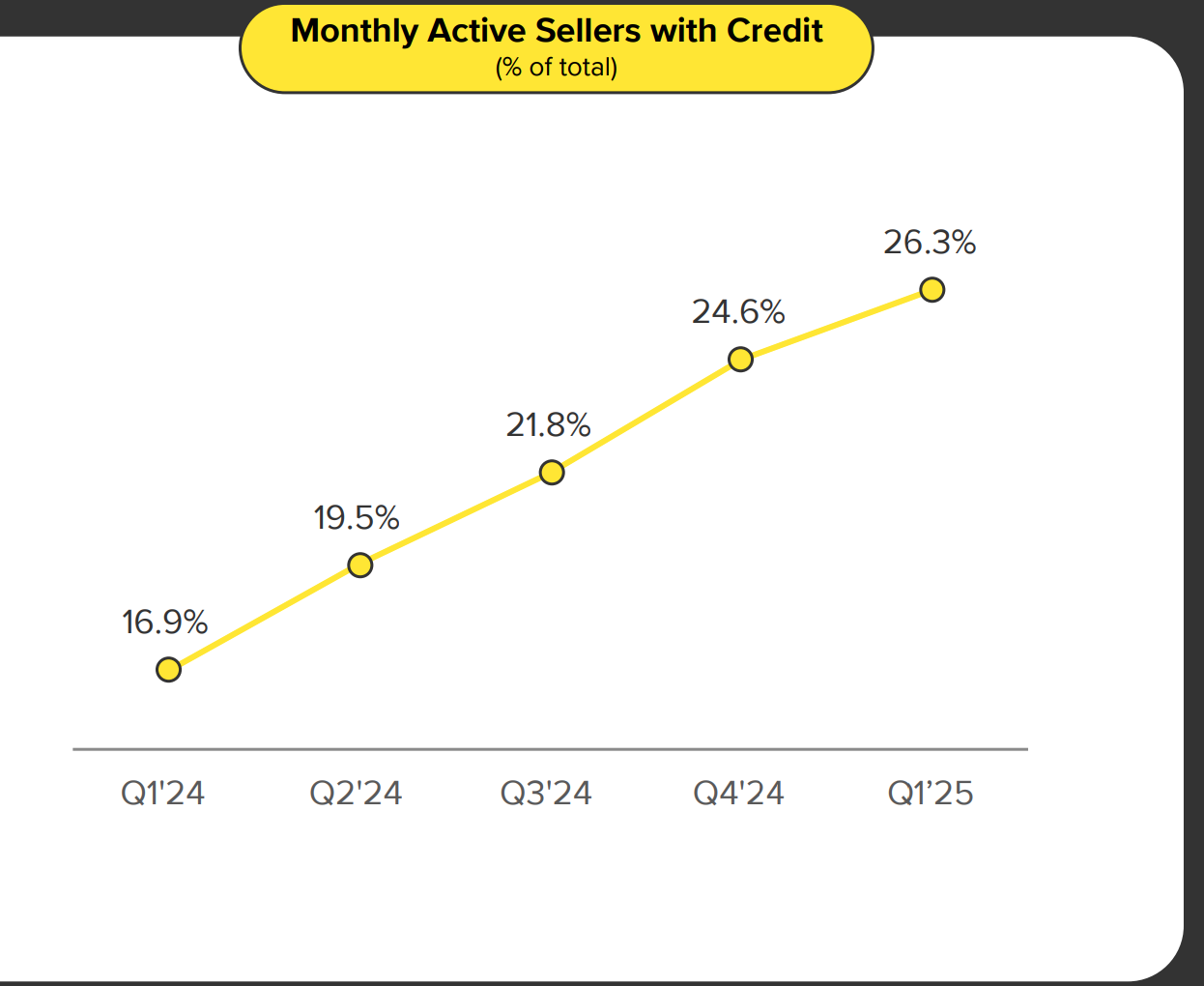

Interestingly, the total number of sellers within the platform who have active credit stands at 26%, up from 16.9% from a similar period last year.

Mercado Libre or MeLi has built an embedded finance powerhouse where the following core elements exist;

Active buyers and sellers;

Platform dependence i.e. merchants specifically derive a significant portion of their revenues from the marketplace;

Robust data from a number of financial interactions specifically payments, savings, past repayments data and more that enable a comprehensive credit rating;

Solid funding capabilities enabling outside capital to power their balance sheet growth;

A real relationship with their clients both buyers and sellers borne out of delivering consistent and increasing value. Mercado can actually claim to “own their customers” similarly to how Amazon can claim to own its Prime customers.

This resembles Alipay and what they’ve built in China. It enables Mercado to grow its credit business in a more aggressive manner and this creates the kind of economics we’ve analysed i.e. 40%+ CAGR growth across a number of metrics over a 17 year period with room to grow. It’s an exceptional Fintech. The question is, do similar conditions exist in Africa?

Mercado’s Context

It’s important to understand the context in which Mercado Libre grew and draw parallels to African e-commerce and subsequently, the embedded finance opportunity in the continent and how it will look. A few interesting themes emerge that explain how e-commerce evolved in the rest of the world and why a number of markets were able to build MercadoLibre’s whereas a similar business doesn’t exist in Africa.

Urbanisation - Latin America had a surprisingly high urbanisation rate in the late 90s and early 2000s. This concentration of population in major cities provided the density required to build out logistics and delivery networks more efficiently than would be possible in a predominantly rural region.

Argentina: Urban population as a percentage of total was 89.1% in 1999, rising to 89.7% by 2003.

Brazil: The urbanization rate was 80.5% in 1999, growing to 82% by 2002.

Mexico: The urban population share grew from 74.4% in 1999 to 75.7% in 2003.

In Africa, the numbers were significantly lower. In Kenya, the urbanisation rate was 20% in 1999, in Nigeria it was higher at 43% but comparatively it was less than half of Argentina’s

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.