#85 - Neobanks Are Not Coming for the Mega Banks

How to think of Neobank growth in the context of the broader financial sector. PS - They're not coming for large incumbents, it's the mid-size banks that should be worried

Hi all - This is the 85th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

Reach out at samora@frontierfintech.io to discuss sponsorships, content partnerships and advisory work. To find out more about working with Frontier Fintech, click the link below.

Introduction - A New Economic Paradigm

Earlier in the year I was heading home from a meeting. It was around 17:30 and I braced myself for the usual Nairobi rush-hour traffic. As is often the case, once I got into the cab, the driver started engaging me and talking non-stop. I braced myself for a long winded conversation on everything that Kenyans talk about; from politics to football and the typical Nairobi ups and downs. Little did I know that it would end up being a useful discussion on modern work and what it takes to succeed in a platform-driven economic paradigm. The driver was a man in his early to mid 30s, energetic and with a positive outlook to life. For this guy, let’s call him John, Uber was the best thing to have happened to him and it happened by accident.

John never intended to be an Uber driver. In fact, he was a trained lab assistant and had worked for a medical facility in Westlands. He was specifically competent in running X-Rays and CT-Scans. Nonetheless, things changed for him during Covid when the clinic he worked at was forced to shut down temporarily. Like many others, he found himself out of a job; with no income and bleak prospects. Like most people in Nairobi, he turned to the gig-economy to fend for himself and his family. Unlike most Uber drivers I meet, John reckons that this was the best thing that ever happened to him. 4 years on, he has 4 cars of his own, has built a house for his mom in the village and can afford to design a life that works for him. For John, the secret to his success in his words were; working extremely hard especially in the early days, being strategic about which routes you take and going out of your way to cultivate meaningful relationships with strategic clients. For John, this meant spotting high potential clients like tourists who are coming for business, foreigners who work in Kenya and in some cases well connected locals. It turns out that sometimes a foreigner can pay up to 500$ to use you exclusively as a driver for the weekend. John has medical insurance, saves diligently and is building financial resilience.

A study by McKinsey showed that 36% of Americans now earned from gig labour. According to the Gig Economy Data Hub, 25% of people participate in some way in the gig economy. John’s story reflects a broader trend in economic production. An endless march from stable industrial era jobs to gig work. Gig-work is an African reality too. In most African towns or country-sides, young men are making ends meet in the boda-boda economy and women are offering their labour on a daily basis to clean and cook. Gig-work is not a Western Phenomenon. The African Gig Economy is expected to contribute US$ 2.9 billion to Africa’s GDP with over 63% of Africans being involved in some form of self-employment.

Recently, the CEO of Anthropic Dario Amodei recently warned that AI could wipe out over 50% of white collar jobs in the coming years. Two of my favourite creators have written about it. Marc Rubinstein in his most recent Net Interest newsletter talks about how he was about to hire two students from London Business School for research, but AI has stopped him from doing so. Rex Salisbury speaks of the same scenario in a LinkedIn post. In his words “I was planning to hire 1-2 investment associates this year at Cambrian, but I've been getting so much leverage from LLMs for financial analysis, market sizing and more that I've put those plans on hold.” The world is changing and so is the world's economic structure. Personally, I’m able to do article research, produce GPS, research for podcasts and do advisory work for my clients all as a solo-preneur.

Whilst this news is foreboding especially for young people, I think those that lean into reality and logical conclusions derived from this reality will do well. If you zoom out, the industrial era and its creation of long-stable industrial careers is an aberration in millennia of economic production. For most of human existence, stability has not been a thing. For Africa, we didn’t even get to enjoy the fruits of industrialisation at scale. My long-term view is that economic production will be split into two divergent trends. There will be large platform providers who provide tooling and technology and a massive tail of small businesses and individuals that benefit from these tools and create value. The platform providers will include the likes of Safaricom providing telecoms, internet and payment solutions, OpenAI providing intelligence, Stripe offering payment services and YouTube providing media platforms. The long-tail will include solo barbers that can 10x their reach and brand by building social presence, small businesses providing ever niche services and solo creators like Rex Salisbury who now has extreme leverage. The middle will be hollowed out.

If you believe this to be true, then nowhere will this be felt more than the financial sector. You will either be serving the platforms and by platforms this means large African enterprises like Tolaram, East African Breweries and the likes. Alternatively, you could be serving the long-tail of solopreneurs, small businesses or gig workers. I argue that the best way to look at Neobanks is to look at mid-market banks in Africa because this is where market share erosion will happen. The big question is how quickly will existing Neobanks take share from mid-market banks?

In the article I’ll look at;

How Economic production looks like in the 21st century;

How the Banking Sector is changing - The middle squeeze;

The Evidence - How Neobanks are catching up with mid-market banks;

Strategic implications;

How to compete;

Some strategic recommendations

Economic Production in the 21st Century

The economy has changed significantly over the last 20 years with the growth of mega-cap stocks like Alphabet, Microsoft, Meta and Amazon. What these companies have done well is to create production primitives that across most industries, lower the barriers to entry and create economic opportunity. Take AWS for instance, with a simple credit card, a small business can access world class storage and compute capabilities. For Alphabet, using both a smartphone running on Android and a YouTube channel, someone can create a media company from scratch. These companies have created platforms that at core democratise production. The result of this democratisation is a complete paradigm shift in how most industries and the broader economy is structured. A barbell of sorts.

At one end of the barbell, you have the infrastructure giants, a small group of hyperscale firms that own the foundational tools of modern production. They provide payments, cloud storage, AI models, logistics, identity, and even distribution. Their power doesn’t come from manufacturing finished products, but from renting out the rails on which others build. Locally this is extended by large firms like Vodacom, MTN and others that provide the infrastructure necessary to participate in this digital world.

At the other end of the barbell sits a growing class of micro-producers; individuals, small businesses, creators, and digital artisans who leverage these primitives to punch far above their weight. A single YouTuber can now reach more people than a traditional broadcaster. A trader in Onitsha with Moniepoint and WhatsApp becomes a 24/7 fintech-enabled storefront. These are lean operators: low fixed costs, global reach, and real-time data. In many cases, they operate more efficiently than legacy institutions ever could. Young people are setting up channels for instance on TikTok where they sell clothes, leveraging payments infra provided by the likes of Opay and Safaricom and the capabilities provided by the mega platforms.

And in the middle? Increasingly, not much.

The traditional mid-sized firm, the local clothes retailer, the legacy software vendor, the local distributor is getting squeezed. It can’t compete with the scale economics of the infrastructure providers, and it can’t match the agility or cost structure of the new artisan class. It’s too large to be lean, too small to be indispensable.

This is the barbell economy: platforms at the top, producers at the bottom, pressure in the middle. And this dynamic is reshaping not just tech and media, but finance, logistics, manufacturing, and beyond.

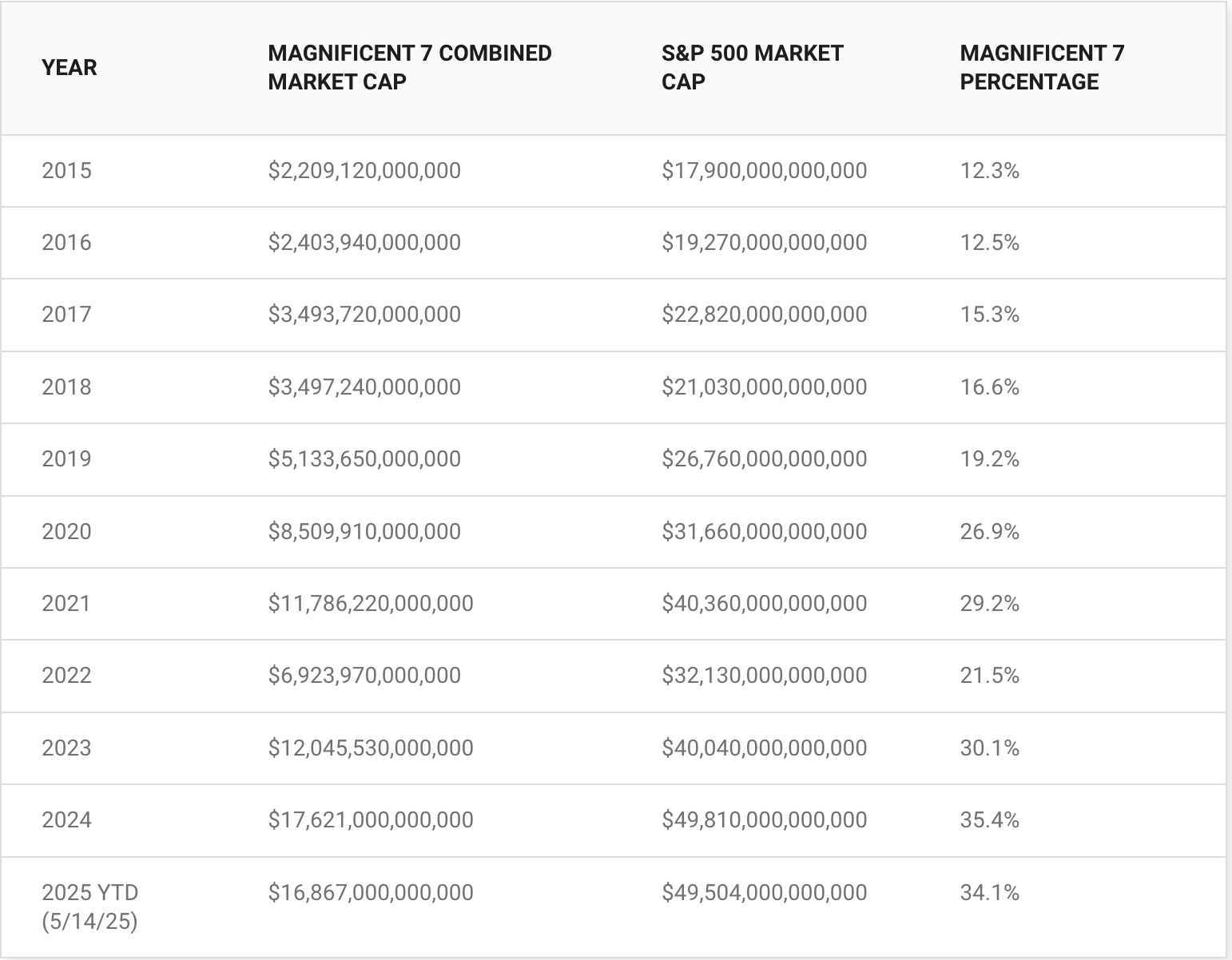

Source: Motley Fool

Globally, the Mag 7 accounts for 34% of the S&P 500 up 3x from 2015. In Kenya, Safaricom accounts for an unhealthy 39% of the NSE in terms of market cap. In Nigeria, the top 3 of Bua, Dangote and MTN account for around a third of the total market cap of the Nigerian Stock Exchange. Across the world, there is an increasing separation between the mega corps and the mid-sized companies.

This trend is likely to explode with AI as these large entities benefit from increasing primary data advantages coupled with the capex to invest in AI infrastructure. My view is that the mega corporations will get much larger and continue to take an unhealthy chunk of global GDP unless there are some regulations in place. They will be joined by new players like BYD and other Chinese manufacturers in the automotive, aviation and robotics sectors. Nonetheless, at a niche and local level, small innovative players will thrive in terms of retail, niche production and services. The smaller players will be those that leverage technology the best. It could be agro-vets in the country-side who leverage AI to help farmers with crop management or dairy output for instance. The barbell will continue.

The barbell effect in labour is clear: a small, well-paid elite inside the mega-corps, a shrinking middle of risk-averse managers in legacy and public-sector roles, and a vast, precarious pool of gig workers and micro-entrepreneurs trading stability for upside.

Banking and Financial Services in the 21st Century

Interestingly, the financial sector is no different. The same mega-corp dynamics are at play in the banking sector with ramifications in terms of how the Neobank and digital payments space will be shaped. Banking too is being structured like a barbell with increasing concentration at the very top.

Financial services evolve to fit in with the existing industry dynamics. From the Medici era to today’s digital era, banks have shaped themselves to serve the economy and that’s why it’s always useful to understand economic structure prior to understanding the competitive dynamics in finance. The financial services sector from a competitive dynamic will shape up to deal with the barbell economy consisting of;

Large platforms and mega corporations;

A big mass of agile and hyper competitive niche players;

A squeezed middle.

At the top of the barbell, very large banks are evolving into infrastructure providers. They don’t just serve end-customers, they increasingly serve other banks, fintechs, and platforms. At the bottom of the barbell, neobanks and fintech insurgents are competing on pure cost-to-serve and digital agility, building lightweight, API-native services that plug into the real-time economy. And in between, mid-sized banks are getting squeezed too slow to scale, too expensive to compete, and too thin to matter in the digital value chain.

The Giants

For the largest banks, the barbell economy has turned out to be a feature, not a bug.

These banks have the capital, regulatory licensing, global relationships, and technology budgets to evolve into platforms themselves. They’re embedding banking functionality into enterprise workflows, becoming the financial backend for ERP systems, e-commerce platforms, treasury departments, and even governments. Moreover, they have the budgets to not only participate in RnD, but to build moon-shot projects. In AI for instance, JP Morgan has invested in an AI Research Centre and have made structural changes to have a Chief Data and Analytics Officer. In our last article on AI and platform shifts, we discussed how Chinese Banks like ICBC have built their own billion parameter models like Zhiyong. These large banks are actively shaping the future of financial services and will more and more built tools to serve the mega corps. Some examples suffice;

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.