#73 - Ecosystem Banking - Why it Matters and the Keys to Success

A look at one of the most successful Ecosystem plays, why Ecosystem Banking matters and the core things to get right in Ecosystem Banking

Illustrated by Mary Mogoi - Website

Hi all - This is the 73rd edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

Reach out at samora@frontierfintech.io for sponsorships, partner pieces and advisory work. Spaces are becoming limited on my advisory hours. I help clients with market entry, market mapping, strategic insights, sounding board to founders and general advisory across Pan-African Fintech.

📢📢I’m carrying out a Reader Survey over the next month to get insights from you on what works, what I should improve, what you value as well as some information that would help me make Frontier Fintech a thriving Media Business. Please fill out the survey below.📢📢 It shouldn’t take more than 3 minutes of your time.

Sponsored by Oradian

Built for Local Realities

Scaling a fintech or financial institution in Africa means navigating unique regulatory, operational, and market-specific challenges. Many global core banking solutions—built with mature markets in mind—lack the flexibility to accommodate local realities. A prime example? Loan fee structures. In many African markets, lenders need the ability to amortize fees over the length of a loan—a feature that most global core banking platforms don’t natively support. Fintechs and banks are forced to rely on cumbersome workarounds or build expensive custom solutions just to meet everyday business needs.

Oradian solves this by offering a core banking system designed specifically for dynamic markets. Our configurable platform adapts to local requirements, allowing financial institutions to operate seamlessly without compromise. From flexible fee structures to regulatory-ready workflows, Oradian provides the infrastructure you need to scale efficiently. Stop forcing global solutions to fit local challenges. Discover how Fairmoney uses Oradian to power its advanced lending business;

Introduction

Miles in the Sky

In 1978 the Airline Deregulation Act in the United States officially ended sweeping US Federal regulations over areas such as fares, routes and market entry for new airlines. This instigated a Cambrian Explosion of innovations in the airline industry. A natural consequence of de-regulation was extreme price competition particularly amongst the big airlines such as American Airlines, Delta and United. Clearly, there was a need for a new approach to retaining customers for the airlines to remain competitive. American Airlines legendary CEO Robert Crandall knew that there had to be a better way to drive loyalty, avoid price competition and run a profitable airline. In the early 80s, he together with his team at American Airlines came up with a solution that would change the industry forever. American launched a Frequent Flyer program called Aadvantage in 1981. Whereas similar programs based on accumulating loyalty points had always existed, the true innovation behind Aadvantage was that customers could redeem points for flights. It turned accumulated miles into actual money, an innovation in Finance rarely talked about. The more you flew the more miles you earned and these miles could be redeemed for flights. This created a flywheel of demand and enabled the loyalty that American Airlines set out to create.

Robert Crandall nonetheless could never have imagined the multiplier effects on the economy that these frequent flyer miles would have.

Citibank and their Foray into Credit Cards

At around the same time that American Airlines was innovating on Frequent Flyer miles, Citibank under their then CEO John Reed was also experimenting on their foray into retail lending. Whilst credit cards got into the mainstream in the 50s through efforts by both Diners Club and Bank Americard which later became Visa; Citi had sat out the business of credit cards in the 50s and parts of the 60s. Their thinking was that they didn’t want the defaults and managerial overhead that would come with running card programs. Nonetheless, they couldn’t sit this out forever as they saw the immense growth of the industry from the sidelines. In the 60s they dipped their feet into the industry by launching what was then called the Everything Card.

The idea behind the Everything Card according to John Reed was that the bank needed to make a line of credit available to consumers efficiently. Unlike in Britain, overdraft banking was not allowed in the United States. Unfortunately the Everything Card was only acceptable in New York and didn’t gain popularity. John Reed’s colleague Dave Philips pointed out that since cards were already based on contacts by phone and mail, then they could extend their card program outside of New York. Citi at the time was known for their international banking operation. In the United States, they maintained branches in New York only. In the 70s and 80s, the confluence of credit scoring and direct mailing drove Citi to run a nationwide direct mailing campaign to distribute credit cards. The challenge though was that New York maintained Usury laws and therefore there was a cap on how much interest the bank could charge on their cards. This coupled with the high interest rate environment initiated by Paul Volcker’s aggressive monetary policy made the credit card business unprofitable.

In 1981, Citi got a reprieve, South Dakota lifted its usury laws and Citi shifted their entire credit card operation to South Dakota. Now, it could lend profitably and their credit card operation grew. Nonetheless, the business was not sticky and they needed a better way of attracting the right customers. Striking gold would mean finding customers who spend big amounts of money, paid interest and were loyal. With such characteristics, the credit card program would be transformed into a gold-mine.

The Perfect Storm - Citi and American Airlines’ Aadvantage Card

Necessity truly is the mother of all invention. Citi needed a way of attracting high spending customers who were likely to remain loyal. What if you could partner with someone who could confer these benefits. Someone who was also keen on driving adoption of their product whilst also engendering loyalty. In retrospect, Citi partnering with American Airlines makes perfect sense. In 1987 Citi partnered with AA to launch the Citi Aadvantage co-branded credit card. The innovation was that you could now earn miles by purchasing every day goods. Whenever you swiped your card at grocery store or at the movies, you earned American Airlines frequent flyer miles.

The financial innovation that emerged from frequent flyer miles was now circulating in the real economy. By the 1990s, the Citi Aadvantage card had become the most popular credit card in the United States. Other airlines scrambled to launch their own but American had the first mover advantage. Both got what they were hoping from this partnership. Citi and American attracted high spending customers who were also super sticky. The average Citi Aadvantage card holder uses his card for 7 years compared with the 2 year average of normal credit cards. For American Airlines, these partnership became a multi-billion dollar business.

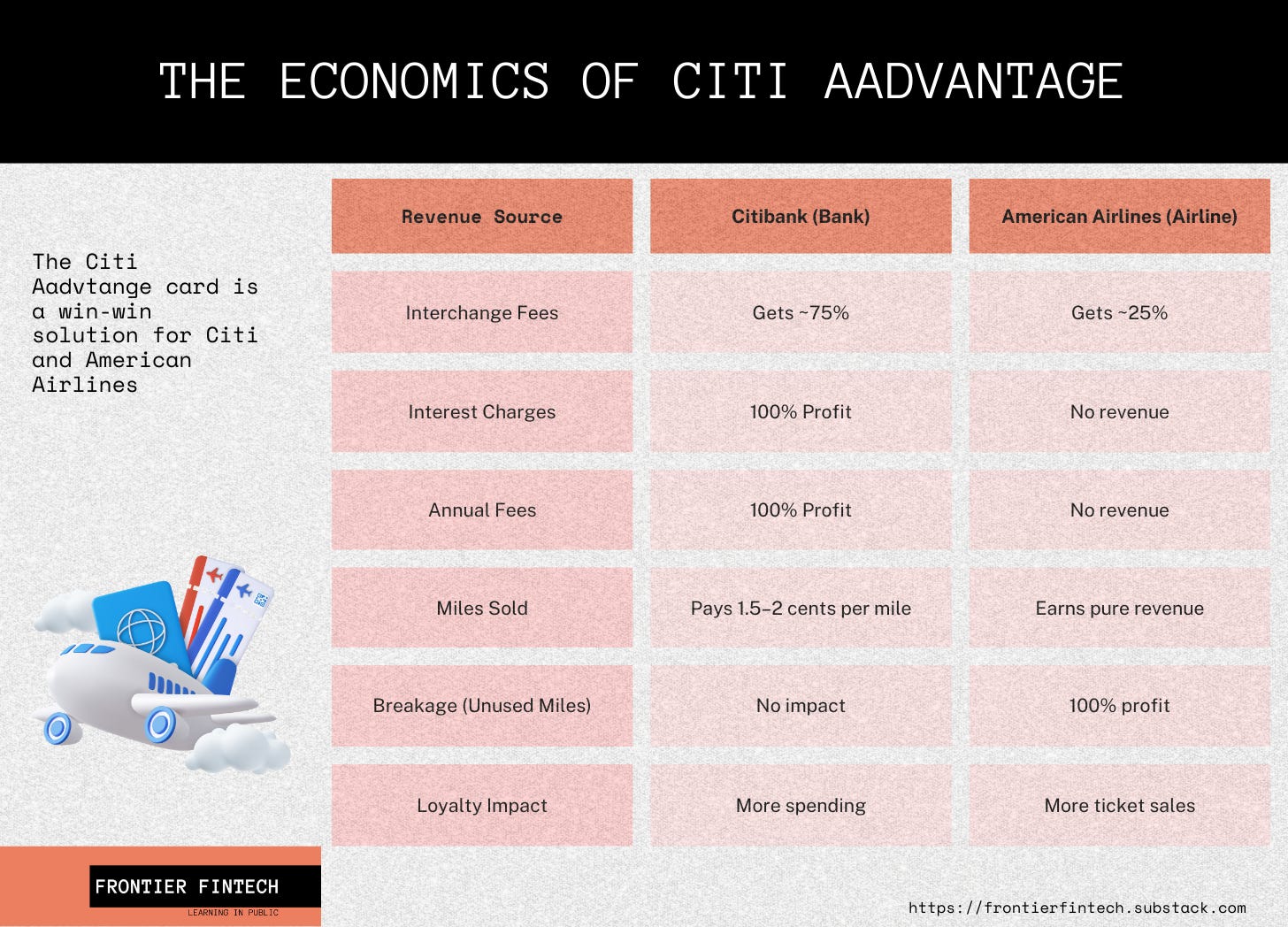

The Economics of Co-Branded Card Programs

One might ask, how do these entities actually make money from these programs? At the core of the partnership was a highly profitable exchange:

Citibank buys miles from American Airlines at a wholesale rate (typically 1.5–2 cents per mile).

Every time a cardholder swipes their Citi AAdvantage card, Citibank collects an interchange fee (1.5–3% of the transaction amount) from the merchant. A small portion of this goes to American Airlines.

If the cardholder carries a balance, Citibank earns interest (18%–25% APR), which is the most profitable part of the business.

American Airlines benefits because loyal cardholders book more flights, generating ticket revenue in addition to the money they make from selling miles.

Not all miles get redeemed—some expire unused, making them pure profit for the airline.

In 2023, American Airlines made over $6.5 billion from selling miles, with a significant portion coming from Citibank. Meanwhile, Citi’s credit card business generated billions in interest and transaction fees, making the AAdvantage card one of its most lucrative products.

The numbers were staggering. Citibank was effectively printing money, while American Airlines had turned loyalty into a financial asset more valuable than flying planes. The partnership has been running for 37 years and recently both Citi and American Airlines signed for 10 more years with Citi as the exclusive issuer.

Why does this matter

The Citi Aadvantage card is one of the most successful implementations of Ecosystem banking in the world. Whilst the term Ecosystem banking may not have existed at the time, the fundamentals of what Ecosystem banking are were embodied in this partnership. As markets mature, ecosystem banking offers a path to differentiation beyond commoditized products, a trend critical for long-term relevance.

The market has caught on. Numerous banks have stated intentions to invest in Ecosystem Banking. Standard Bank in 2021 stated that it will meet clients “on the digital platforms where they are shopping, socialising and doing business” and will do so “by driving or contributing to ecosystems – combining its own offerings with those of partners to fulfill a broad range of needs seamlessly.” I&M Bank of Kenya in the last couple of years have stated their intention to become a market leader in ecosystems through leveraging their own corporate supply chains and building new ecosystems. Equity Bank in Kenya has talked about shared prosperity and has an ambitious Pan-African program called the African Recovery and Resilience Plan which at its core is a massive Ecosystems undertaking. Ecosystems banking is an area that will be critical for banks to get right to maintain market relevance in the long-term.

This article will give an overview of Ecosystem banking, give local and global examples of Ecosystem banking, define what key characteristics permeate all successful ecosystems and give some recommendations to how banks can increase their probability of success in Ecosystem banking.

Ecosystem Banking

In traditional banking, institutions attract customers with standardized offerings such as loans, savings accounts, and credit cards, competing largely on distribution channels, pricing strategies, and promotional efforts. However, as these products become commoditized as banking markets mature, banks struggle to differentiate themselves, leading to shrinking profit margins and diminished returns. Ecosystem banking presents a transformative alternative, where financial institutions partner with external entities to integrate services into customers’ everyday lives. A prime example is Citi’s AAdvantage program, which ties banking services to airline loyalty, creating a unique value proposition that’s difficult for competitors to replicate. This model not only opens new revenue streams but also strengthens customer retention by embedding banking into broader lifestyle ecosystems.

As traditional banking faces mounting pressures, this strategy gains traction globally. Sberbank’s CEO, Herman Gref, emphasized its urgency in an interview, stating, “Sber does not have another alternative than to build an ecosystem as banking margin is declining. Sber has a relatively small ecosystem comparing to our banking business, and we don't see any risks for now.” To support this shift, Sberbank has committed over $2 billion—roughly 3% of its capital—demonstrating the substantial investment required to succeed in this competitive, evolving landscape.

Successful Implementations of Ecosystem Banking

Whilst Citi’s example is definitely riveting, there are plenty of examples of successful Ecosystem Banking in Africa and Globally. Here are some examples;

African Ecosystem Banking Successes

NCBA x Safaricom M-Pesa

Product - M-Shwari

Bank - Commercial Bank of Africa - Now NCBA after merger with NIC Bank;

Ecosystem Partner - Safaricom’s M-Pesa Product

Description - CBA had been providing Trust Account services to Safaricom’s M-Pesa product since 2007. This meant that the bank stored all the e-value that was in circulation in M-Pesa. Initially, this partnership was driven by M-Pesa’s need to store this money in a regulated entity but importantly, CBA’s need to secure low cost and sustainable deposits. After 5 years of this partnership, CBA realised that they could leverage M-Pesa’s growing customer base to offer savings products as well as issue short-term loans directly to M-Pesa users. The partnership was formed whereby M-Pesa customers could open savings accounts with CBA and benefit from short-term loans. In the first week, M-Shwari registered over 700,000 customers and by 2016 this had shot up to 14 million customers with over US$ 700 million disbursed. The key insight was that Safaricom’s ubiquity, M-Pesa’s increasing utility and the Sim-Card as a form of identity would drive positive repayment behaviour.

Value for Bank - More customers, new revenue streams, more sources of deposits;

Value for Safaricom - Increased revenue, higher customer loyalty and a stronger value prop for M-Pesa. This client testimony shows the value that M-Pesa customers received from M-Shwari

Stanbic Bank of Kenya - Kenya’s Tea Industry

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.