#72 - Stablecoins Revisited - The Factors that could Stall Adoption - Free to Read

Evaluating the promise of Stablecoins whilst soberly analysing the factors that could derail adoption in Africa

Illustrated by Mary Mogoi - Website

Hi all - This is the 72nd edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

For group discounts, write to me at samora@frontierfintech.io. If you can’t afford a subscription, consider referring a friend. The more you refer the longer your complimentary subscription is.

Reach out at samora@frontierfintech.io for sponsorships, partner pieces and advisory work. Spaces are becoming limited on my advisory hours. I help clients with market entry, market mapping, strategic insights, sounding board to founders and general advisory across Pan-African Fintech.

Sponsored by Oradian

Build vs. Buy Decision

Every fintech reaches a critical decision point: build a core banking system in-house or adopt a proven solution? On the surface, building may seem like the more customizable option, but the real cost quickly adds up. Hiring engineers, maintaining infrastructure, and ensuring compliance can easily exceed $80K per month—and that’s just to keep things running. Worse, building an in-house core banking system is rarely a competitive advantage. Investors want to see fintechs focusing on customer experience, product innovation, and scaling—not reinventing the back end.

But buying the wrong core banking system can be just as costly. Many fintechs pick solutions designed for mature markets, only to find that they don’t support local regulations, customer behaviors, or lending models. Without built-in flexibility for dynamic markets, fintechs risk costly workarounds—or worse, having to start over.

That’s why fintechs like FairMoney in Nigeria choose Oradian. As FairMoney scaled, they needed a core banking system that could grow with them—one that understood the intricacies of African lending, from fee amortization to local compliance requirements. Oradian provided a flexible, cloud-based core banking platform, allowing FairMoney to focus on its mission: building innovative financial products, not maintaining infrastructure. Discover how Fairmoney uses Oradian to power its advanced lending business;

Introduction

Stablecoins are the hottest thing in Fintech at the moment, with a market cap of over US$ 221 billion, monthly transfer volume slightly above US$ 2.0 trillion and over 149 million holders of Stablecoins; it’s difficult to ignore the opportunity. To add to this, there’s a growing consensus that the Stablecoin opportunity is more of an emerging market opportunity rather than a developed market one. Stablecoins are digital money designed to keep a steady value—often by being linked to traditional currencies like the US dollar—making them more predictable than other cryptocurrencies. This feature coupled with global, instant mobility promises to unlock cross-border payments and store of value opportunities. Nonetheless, one can’t assume that the road to this ideal world will be smooth. Interestingly, history offers us parallels and we’re always reminded that “plus ca change, plus c’est la meme chose”. The more things change the more they stay the same. This article will look at an interesting but relevant historical monetary innovation, compare this historical era to the existing stablecoin era, evaluate the opportunities that Stablecoins bring particularly for cross-border payments, evaluate the failure modes for Stablecoin adoption in Africa and analyse what the Stablecoin industry needs to avoid to ensure success.

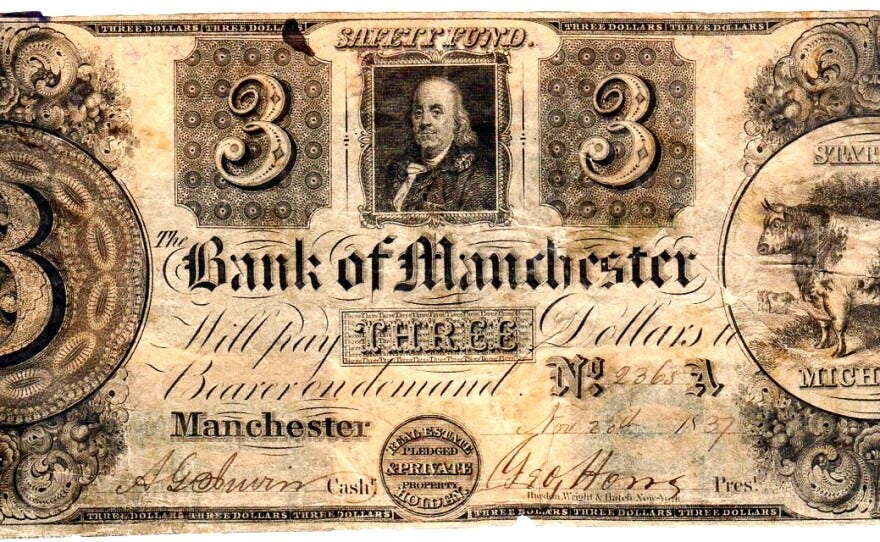

Free Banking Era

In the 19th century, a great experiment in banking arose across the world. This period was marked by what we now call the Free Banking era. In the United States, this run between the 1830s and the 1860s. the core idea was that State laws allowed anyone who met specific requirements to issue bank notes and coins so long as they were backed by acceptable assets. Unlike the current world where money issuance is done by the Central Bank, Free Banking involved private banks issuing their own notes and coins.

This experiment was not only constrained to the United States. In countries like Scotland, Canada, Australia and Sweden, Free Banking prevailed. In Scotland, this was further enhanced by unlimited liability laws that ensured that the shareholders of banks were personally liable for any difference between the value of the notes in circulation and the assets held to represent that value.

A US$ 3 Note from the Bank of Manchester, Michigan - Source

The decentralised nature of banking led to challenges such as interbank settlement and counterfeiting. This then lead to innovations. To deal with interbank settlements, clearinghouses were formed with Scotland in particular being a pioneer. Banks created unique security features in their notes such as the use of special ink and paper to deal with the threat of counterfeiting. Lastly, the concept of bank branches arose from the need to avail cash across a wider geographical area.

Whilst Free Banking worked relatively well in some countries, it failed in others. Countries like Scotland and Canada had relatively successful implementations of Free Banking. The banks in these markets were responsible and always ensured that they had sufficient assets to cover their liabilities. One core distinction was that Scottish Banks were governed under unlimited liability laws meaning that shareholders were on the hook for any losses the bank made.

In countries like Australia and the United States, the experiment was not as successful. In the United States, irresponsible banks particularly in the Mid-West issued an excess of bank notes to their assets. This led notes from some banks not being accepted the further you went from State Territory. It is estimated that around 20% of the banks in existence in the US during this period failed. In Australia, most capital inflows were due to investments by the United Kingdom. The Baring Crisis in 1890 led to a screeching halt in inflows leading to a banking crisis.

The failures of free banking particularly in the US gave credence to the idea of a unified monetary system. Through an evolutionary process, this eventually led to the creation of the Federal Reserve in the United States and Central Banking as a core aspect of modern monetary management. The value of Central Banks were that;

Central Banks ensure a dollar from JP Morgan is equivalent to a dollar from Citi and that this is all equivalent to a dollar in cash. Most people don’t even think of it that way but in essence, a bank like GT Bank issues its own digital Naira and Access Bank does the same. The Central Bank’s job is to ensure that these two are exactly the same through regulation and oversight. It’s one of the most fascinating elements of modern money and this is what enables payments to be seamless;

Acting as the lender of last resort - This is tied to the ensuring that money retains its principle of being single;

The lessons from free banking, such as decentralization and asset backing, provide a useful mirror to today’s stablecoin innovations;

Both relied on the idea of decentralisation where the focus was on private issuers of money rather than a central authority;

In both, there were recorded instances of instability in value of bank notes in the Free Banking era or Stablecoins in today’s era;

Competition amongst issuers in both eras drove innovation. In Free Banking we saw the rise of clearinghouses, branches and secure notes as a form of innovation. In Stablecoins, innovations such as the Cross Chain Transfer Protocol (CCTP) by Circle are driving the industry forward;

Both relied on a form of backing - With Stablecoins, the backing is through a basket of assets such as cash and T-bills and with Free Banking, notes were backed by gold and other assets;

As much as there are similarities, some differences remained. However, that’s not the point, the core points are;

The world has witnessed periods of monetary innovation before and will continue witnessing them. As long as humans exist, innovations in payments and money will exist;

For money to be accepted and fulfil its role in payments, particularly trade, it has to have the property of singleness. That is, a dollar in your wallet is the same as a dollar in your Mobile Money wallet and is equivalent to a dollar in any bank in the country;

Lastly, the current monetary system that is built on Central Banks and heavily regulated traditional banks has existed for centuries and has gone through significant upheaval. It has nonetheless proven to be very anti-fragile. Using the idea of Lindy, it’s more likely that it will continue to be in place over the next 200 years through evolution.

Given that Free Banking was a period of great innovation, but ultimately failed, then the approach the Stablecoin industry should use is around avoiding failure rather than trying to achieve breakout success. It should be a negative science.

Stablecoins so Far

We’ve written about Stablecoins before highlighting their core features from a technological perspective and also looking at the use cases. It’s useful to recap these two things;

Stablecoins as a Technological Innovation

Traditional payments from the Venetian era to the current era of global payment companies such as Thunes, Wise and Nala have always operated on three distinct phases of payments; Messaging, Reconciliation and Settlements. A payment of US$ 100 from the UK to Ghana includes the sender instructing the bank (message), the bank confirming that it has the balances to make the payment (reconciliation) and a payment being made between the sending bank and the receiving bank (Settlement). Most of the innovation in payments has focused on the messaging and reconciliation layers.

Usually in Africa and large parts of the emerging world, that settlement is often the biggest blocker to efficient transactions. It takes many days for that settlement to happen (usually 5-7 days) and that delay causes risks from a currency perspective, in essence in 5 days, the cedi may change its value and therefore let me adjust my pricing to reflect that risk. These delays and risks are the largest driver of cross-border payment costs in the continent.

Eytan Masika, an entrepreneur in the Stablecoin space, Founder and CEO of Nilos and one of the most insightful people in the space had this to say;

Correspondent banking works well when the corridor is extremely liquid on both sides and that currencies are relatively stable like EUR-USD / EUR-GBP pairs because the risk of holding currencies in vostro accounts is virtually 0….I can’t stress this enough ; in the current OS - in correspondent banking : MONEY DOESN’T MOVE. …From first principles, you quickly realize that if money doesn’t move ; holding it comes with an exposure. And this is where it becomes interesting : The less liquid a corridor is —> The higher the risk of holding a currency for fintechs/banks is —> The higher the cost for customers to cover for this risk It works ; except where it doesn't. That’s why in emerging markets rates are high ; settlement are slower even for those fintechs. The OS can’t make it more efficient. You’d have to make their economy stable to make it work. Also from first principles, we realized early on in Nilos that the only way to not bear the change risk would be to NOT HOLD the currency at all. But how? We would need a way to ACTUALLY MOVE MONEY IN REAL TIME in an interoperable, fast and liquid way in both emerging markets and developed economies. That’s stablecoins. This is the new OS.

Commenting on the same post, Nicolai Eddy, COO of Nala added additional nuance;

I mostly agree with your point, Eytan Messika. Beyond local currency liquidity challenges—which are more of an FX issue but still impact the ability to send funds over SWIFT—the larger issue I'd say is that many emerging markets are classified as high-risk. When global dollar-clearing banks (like Citi, JPM, etc.) receive payments from a bank in an EM, they often flag (and as a result, delay) the payment due to various compliance reasons. These include regular transaction monitoring or missing KYC information not provided by the originating bank.

I couldn’t have said it better. With a Stablecoin, messaging, reconciliation and settlement happen all at once. This speed is inherent in making them cheaper if you agree with the insight that the delay in settlement is the biggest driver of costs.

The Business Case for Stablecoins

There are a number of use-cases that have emerged for Stablecoins. They’re listed below;

Retail Payments;

Crypto-Trading - The original use case where people needed a low-risk asset to get in and out of as they traded crypto;

De-Fi and Programmable Money - We’ve covered this here;

Store of Value and Savings - Particularly important in countries that experience high levels of inflation and currency depreciation;

Basic Financial Inclusion;

Cross-Border Payments and Remittances;

I think cross-border payments are the biggest potential use case for Stablecoins in Africa for a number of reasons. Total African Trade is worth US$ 1 trillion, trade in China stands at US$ 300 billion and total remittances are estimated at US$ 100 billion.

Retail payments are solved. Even in cash only markets, people can make payments, cash is a technology and so there’s no market failure. Store of value is interesting particularly in markets where access to dollars is difficult. That being said, Africans for a long-time have figured out ways to hedge against inflation including things like purchasing land. It’s the second largest use-case behind cross-border payments all the same. For crypto-trading and De-Fi, these are activities that are not core to most Africans on the continent and are niche opportunities. Africans by and large are focused on trade, agricultural activities and employment.

Whilst the store of value proposition is important both for individual and institutional purposes, my core point is that with GDP per Capita in most African countries being sub US$ 2,000 and with median ages less than 20, the bulk of Africans are not even in a position to store value. There’s no value to be stored. The biggest job to be done is to enable the creation of value and that’s where payments come in.

If you believe that the biggest innovation in stablecoins is the unification of payments messaging, reconciliation and settlements; then cross-border payments should be the biggest opportunity. Stablecoins therefore are more of a replacement of SWIFT and Correspondent Banking. Their core job will be to enable Africans to easier make and receive payments. That should be the big opportunity and this is where the focus of the article will be.

Why Stablecoins are an Important Trend to Watch

In my previous article I explained the similarities between Stablecoins and Mobile Money from an e-money issuance perspective. In fact, I used the table below to explain the key differences;

The simple point here is that we’ve seen a simple innovation in payments and store of value driving a revolution across the continent. Mobile Money in the last decade has enabled not only financial inclusion but it has acted as the payments layer for a new local trading economy where a new type of e-commerce has emerged. In places like Kenya, Nigeria, Uganda and Ghana, it has activated the urban gig-economy all the way from boda-boda riders, fast retail and the creator economy.

Stablecoins could in theory unlock the global and regional payments opportunity. For instance, payments from Nigeria to Ghana can be made cheaper and faster using a mix of local currency and foreign currency stablecoins. This would obviate the need to go through the New-York correspondent banking system.

Nonetheless, there’s a long road ahead. Rather than asking how will Stablecoins succeed, I have approached this from a “How did Stablecoins fail”. I’ll highlight the potential failure points for Stablecoins in the following section.

What does Stablecoin Failure Mode Look Like?

There are a number of factors that could derail Stablecoin uptake in the market. It’s worth looking at each in some details

Lack of Regulatory Clarity

When I speak to players in the crypto and stablecoin space, there is a growing clamour for regulation of the space. This is being driven with a view to legitimising the space and therefore enabling trust which is crucial for mass adoption of stablecoin based payments. The talk is always “we’re engaging regulators and it’s an ongoing discussion because we have to educate them. There’s an understanding gap”. Nonetheless there are some factors that give me pause about this approach.

Players in the crypto space from South Africa, Nigeria to Kenya have all engaged Central Banks with a view of having some sort of licensing available to Crypto players. To be honest, these discussions have not led to any Central Bank licensing. Despite South Africa having a very robust engagement with the Central Bank, the outcome has been Crypto Asset Service Provider licensing frameworks across the continent. These are governed by the respective capital market authorities e.g. the SEC in Nigeria and FSCA in South Africa. There is a clear trend and dynamic emerging across all these regulatory engagements. Central Banks are being non-committal.

The poker game being played by the Central Banks is feigning ignorance and stating that “it seems you should engage with the Capital Market Authorities” as this is not in our mandate. The industry is interpreting this ignorance as an awareness gap whereas a seasoned salesman in Africa can clearly see that its a poker game. Why does this matter?

If Cross-Border payments are the biggest use case for Stablecoins, then regulatory activity should be centred around a mix of applying FX or PSP regulations to stablecoin players. Nonetheless, the Central Banks have side-stepped this and pushed them to be licensed as asset providers where crypto including stablecoins are a financial asset.

How this becomes a failure mode is that eventually Stablecoins will become captive assets that are then taxed like financial assets. Anytime you trade them, there will be levies applied to each transaction under the guise of digital asset taxes. It will simply be impossible to use a stablecoin as a payment rail if each transaction is taxed at such rates.

You must remember that Central Banks are keen on protecting their own currencies and their role as the ultimate custodians of a country’s FX and Payments markets. Such an outcome is therefore favourable to them. It’s not wise to assume that they have an “understanding gap” when it comes to Crypto. The best way to approach this is to assume that they are even more knowledgeable than you and be clear that Stablecoins should be licensed as a payment business rather than a store of value business.

Dollarisation

In many parts of Africa, even those countries that have relatively open capital accounts, hard currencies are treated like a national asset where the government should have some say in how they are distributed across the country. In Kenya for instance, part of the clampdown against betting companies over the last 6 or 7 years was largely because they were ultimately collecting hard currency from the country and repatriating it without any net benefit. In other countries like Nigeria, Burundi and Malawi, they are an even bigger mechanism for redistributing wealth and getting to determine who can participate in the trading economy. Dollarisation is therefore a massive threat to most African countries.

Christian Catallani, a member of the Libra team that was tasked to create the global Libra crypto-currency by Meta had this to say about dollarisation;

Crypto has a history of greatly underestimating the influence of regulation on its future. We learned this the hard way with the release of the first Libra whitepaper, which led to two grueling years of intense regulatory interactions to align the project with the expectations of policymakers and regulators.

The same is true for stablecoins today. Many assume that stablecoins will seamlessly operate as low-cost, global dollar accounts for consumers and businesses. After all, in a crisis, everyone in the world would prefer to hold dollars in a too-big-to-fail U.S. financial institution. Moreover, one might think the U.S. government would support this, as it strengthens the dollar’s position as the world’s reserve currency.

The reality is far more complex. While the United States risks losing a great deal if its financial and sanctions infrastructure is no longer the global standard—and would face even greater consequences if the dollar’s ‘exorbitant privilege’ erodes, as it has for every reserve currency before it—this doesn’t mean the U.S. Treasury will always favour accelerating dollarization. In fact, its Office of International Affairs would view this as a significant challenge to both diplomacy and global financial stability.

Countries that value monetary policy independence, fear capital flight in a crisis, and worry about destabilising their domestic banks will strongly oppose the large-scale adoption of frictionless USD stablecoin accounts. They’ll use every tool available to block or limit these accounts, just as they’ve resisted other forms of dollarisation. And while it may be impossible to stop crypto transactions entirely, as the Internet has shown, governments have numerous ways to restrict access and curb mainstream adoption.

Counter-examples of places that have embraced dollarisation such as Zimbabwe and Ecuador exist. Nonetheless, I don’t think these serve as models of how countries want to run their economic affairs.

In short, don’t underestimate the threat to dollarisation and don’t underestimate the toolkit that governments have to protect against such a threat.

FX Liquidity

To understand this challenge, one has to understand how cross-border payments using Stablecoins are currently done.

Clients interact with cross-border payment companies such as Cedar to make a payment say to India;

An exchange rate is agreed upon and the client places the equivalent local currency to the payments company;

The payments company has to source US$ from somewhere, it could be an exchange or FX bureau;

The payments company then has to source a USD Stablecoin e.g. USDT or USDC from another exchange e.g. Mansa, Yellowcard etc;

You then work with a company like Conduit to make the Stablecoin payment to the final beneficiary and this is a Stablecoin to Fiat conversion;

The beneficiary receives their funds in their local currency in this case Rupee;

This is a general overview and there’s way more nuance that I have avoided. It’s simply for illustrative purposes. The point to be made is that point 3 i.e. the need to source actual hard currency so as to buy either USDC, USDT or PyUSD is a chokepoint. Stablecoins as a replacement to correspondent banking are great. However, they don’t solve the fundamental liquidity challenge that exist in Africa brought about by FX shortages. These are ultimately issues around trade and capital inflow imbalances. One could argue that Stablecoin based players could try and capture more FX inflows but I think this is largely a price game and no natural advantage accrues to them.

Competition from CBDCs

Source: Bank for International Settlements - Highlight my Own;

A number of people outrightly dismiss CBDCs as some clunky form of innovation from bureaucratic Central Banks. Nonetheless I’ve always cautioned against outrightly dismissing them. If you agree with the earlier thesis of blockchains being an innovation in payments as they unify the core trinity of messaging, reconciliation and payments; and you further agree that money needs to maintain its property of singleness, then CBDCs check both boxes.

Big players like Thunes, Wise, Terrapay and even X would be agnostic to the underlying rails, so long as they get the job done and therefore would happily play an intermediary role in a CBDC driven world. They’re clunky but undermine them at your own risk. The advantage that CBDCs at scale would have is theoretically, incumbent adoption particularly wholesale CBDCs.

Trump’s De-regulation Drive

Some weeks back I wrote about what African Fintech should expect from Trump 2.0. One of the points I made was about de-regulation, specifically how Correspondent Banking in Africa has suffered due to significantly higher levels of regulation and oversight. African Banks over the last 20 years, particularly tier 2 and 3 banks have been locked out of global correspondent banking due to increasing demands for compliance. For global banks, despite there being a business opportunity, the risks and costs outweigh the benefits. As a sign of the changing landscape, Jamie Dimon recently came out and adopted a more aggressive stance towards regulators calling the former CFPB head; arrogant and out of touch. This vibe shift should lead to a reopening of correspondent banking relationships and less stringent oversight and regulation. Nicolai Eddy pointed out that global banks flag payments from Africa as “high-risk” and delay payments. If the regulatory stance changes then payments should become easier.

If Cross-Border Payments become significantly easier then whilst they won’t be as seamless as Stablecoin based payments, they would still be a viable option. This is particularly the case if tech-savvy tier-2 and 3 banks decide to invest in payments. Realistically with Swift GPI and ISO20022, cross-border payments should be seamless. There’s a space where incumbent industries protect their turf by innovation. This can only happen if global banks ease up on African banks from a correspondent banking perspective.

In my view, these are the core challenges to widespread adoption of Stablecoins as a new layer in cross-border payment capabilities. The industry need to focus their efforts on solving these challenges. Of course there are a number of challenges but these are the key ones. I think the other issues are easier to solve and are endogenous to the industry i.e. they’re within the control of the overall crypto industry. Some examples are blockchain inter-operability (see CCTP), Driving adoption and incidences of fraud.

Wrapping it Up

The Stablecoin industry particularly in Africa is evolving rapidly. Some of the smartest operators are joining due to the amounts of money that are flowing into the industry. I’ve interacted with a number of them and they’re savvy and thoughtful. The key take-outs from the article, which I’m sure most operators are aware of are;

Don’t underestimate the savvy of incumbents to snuff out the industry using legislation and sometimes pure skullduggery;

Be very clear with regulators and don’t accept regulation for the sake of regulation. If Stablecoins are to be used for payments then Virtual Asset Service Provider license may actually be detrimental in the long-run;

Don’t assume that Central Bankers don’t understand the space and need to be hand held. Rather, assume that they know exactly what they’re doing and take their slowness at face value;

Ensure that the industry is well co-ordinated so that the customer experience of making cross-border payments feels 10x better than the existing method. The reason why this matters is that existing systems are getting better and there may be a boost due to Trump’s de-regulation efforts;

Deal with the threat of dollarisation upfront. Use the accusatory audit method and don’t assume that you can just ignore this threat when dealing with regulators. Rather, communicate how Stablecoins for payments will not lead to dollarisation;

The risk is that regulators see stablecoins as a form of de-facto dollarisation and they step in to limit their use locally

Thanks for the clear thoughts Samora. Even though I'm investing in this space, I share a lot of your concerns and it makes me worry about the long-term success of many of the new entrants. Ultimately I believe one set of winners will have a direct relationship with consumers and will look very similar to neobanks, differentiating a lot on experience and very importantly pricing. That way when regulations ease for the traditional players, the new guys don't lose all their mojo.

Another set of winners will power the rails especially around liquidity on/off ramping and KYC/AML.

Definitely exciting times ahead.