#64 - Are African Fintechs Overvalued?

Rather than answering this question, let's work backwards to understand what long-term success should look like for modern valuations to make sense.

Illustrated by Mary Mogoi - Website

Hi all - This is the 64th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

Reach out at samora@frontierfintech.io for sponsorships, partner pieces and advisory work.

The beauty of Substack is that the more you refer your friends, the more you can read paywalled content.

Sponsored by Skaleet

Expand Your Embedded Finance Offering with Skaleet’s Platform

Embedded finance is redefining how financial services are delivered, allowing banks to seamlessly offer services within non-banking platforms as well as allowing non-financial services players to distribute financial services products. Skaleet’s solutions are designed to help banks embrace this trend with ease, providing banks the ability to operate as a Bank-as-a-Service and distribute their platforms to third parties, also leveraging a powerful network of pre-integrated partners to create an embedded finance ecosystem. Through Skaleet’s platform, banks can integrate directly with partners across payment processing, lending, KYC, and more, streamlining the journey from idea to launch.

Skaleet’s end-to-end solutioning approach empowers banks to embed financial services in new channels, reaching customers in unique ways without the need for extensive in-house development. This plug-and-play approach, combined with Skaleet’s strong partner network, allows banks to go live with embedded finance propositions rapidly, connecting with e-commerce, insurance, and retail platforms. With Skaleet, banks are able to remain relevant to their Fintech partners whilst not having to over-invest in in-house technical skill. Contact Brice for Partnerships and Beatrice for Sales;

Introduction

The last couple years have been full of introspection about the future of VC funding in the continent particularly within Fintech. Fintech has traditionally accounted for the bulk of VC funding in the region accounting for 27% of total volume of VC funding in Africa between 2014 and 2021. By value, VC funding in Fintechs accounted for between 42% and 48% of the value of deals between 2021 and 2023. It has been the most funded sector in the African start-up space for over a decade. Driving this has been the opportunity set opened up by low levels of financial inclusion and the ability to employ tech to drive new ways of distributing financial services. Nonetheless over the last two years, VC funding has been on a retreat. According to the Africa Venture Capital Association VC report of 2023, total deal volume declined from 854 deals in 2022 to 603 deals in 2023. Total deal value declined from US$ 6.5 billion in 2022 to US$ 4.5 billion in 2023. According to figures compiled from Africa The Big Deal, 2024 figures are trending slightly lower than 2023 figures and therefore we should anticipate a further fall in VC funding this year.

Of course these declines lead to all sorts of post-fact discussions. One has been whether VC funding is suited to Africa and another about whether VC funded start-ups are overvalued. Both questions have their merit but I’ll focus on the latter. The idea that VC funding is not suited to Africa is broad strokes thinking that is anathema to this publication. Saying VC funding is not suited to the continent is like saying Project Finance is not suited to the continent. VC is a capital structure decision and such decisions are always contingent on what the end goal is. One can make the argument that a good portion of businesses in Africa don’t lend themselves to VC funding but a similar argument can be made globally. In fact, according to a study by the Stanford Graduate School of Business shows that venture capital funds invest in only about 0.19% of new U.S. businesses. So VC is a cottage industry globally and most businesses across the world aren’t VC fundable.

What matters is to discuss valuations and whether valuations are out of whack in the continent. One way to do this is by doing a fundamental analysis of the valuation of a bunch of Fintech start-ups and evaluating their growth models. The pitfall to this is that from my understanding of different early stage valuation methods, this is not a science and therefore there’s little to be gained by going deep into a subjective endeavour. At the early stage of a business, the core idea is to give the founder enough capital to allow him to achieve his milestones whilst minimising the dilution he takes. The best way to have a reasonable discussion of Fintech start-up valuations in Africa is through inversion. The idea here is to start at the end and say, “what does success look like for a successful Pan-African Enterprise?”. Once you’ve defined this picture of success, you can then work backwards and say, what would it take for a Fintech start-up to achieve this scale.

Ultimately, as Warren Buffett keeps reminding us, intrinsic value is the discounted value of the total cash flows that a business is expected to generate now and into the future. At the end of the day, this is the gravity that all enterprises have to deal with. Every start-up at some point will be valued like a mature company and therefore starting at the end, one can have better insights into what a US$ 150 million Series A valuation means. In one of my favourite books, “Anti-fragile” by Nassim Taleb, he reminds us that

"The greatest and most robust contribution to knowledge consists in removing what we think is wrong—not in pushing what we believe is right. In other words, inversion and subtraction are more powerful than addition”

Peter Thiel took this further and said;

"Brilliant thinking is rare, but courage is in even shorter supply than genius. It takes courage to ask tough questions and look at problems through the lens of inversion: What if we started at the end? What if we built from the opposite direction?”

This article will look at what success looks like in African business by looking at the most successful companies of the previous generation, the terminal state of a successful African business. Thereafter we will look at the different start-up rounds in the context of this terminal state and simply ask, what is the probability of x given y. Finally, we will make some hopefully logical conclusions as to how both operators and investors should look at valuations and investing in African Fintech start-ups.

The Picture of Success

Now let’s focus on a term that I mentioned earlier and that you will encounter in future annual reports. Intrinsic value is an all-important concept that offers the only logical approach to evaluating the relative attractiveness of investments and businesses. Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life. - Warren Buffett - Berkshire Hathaway Owners Manual

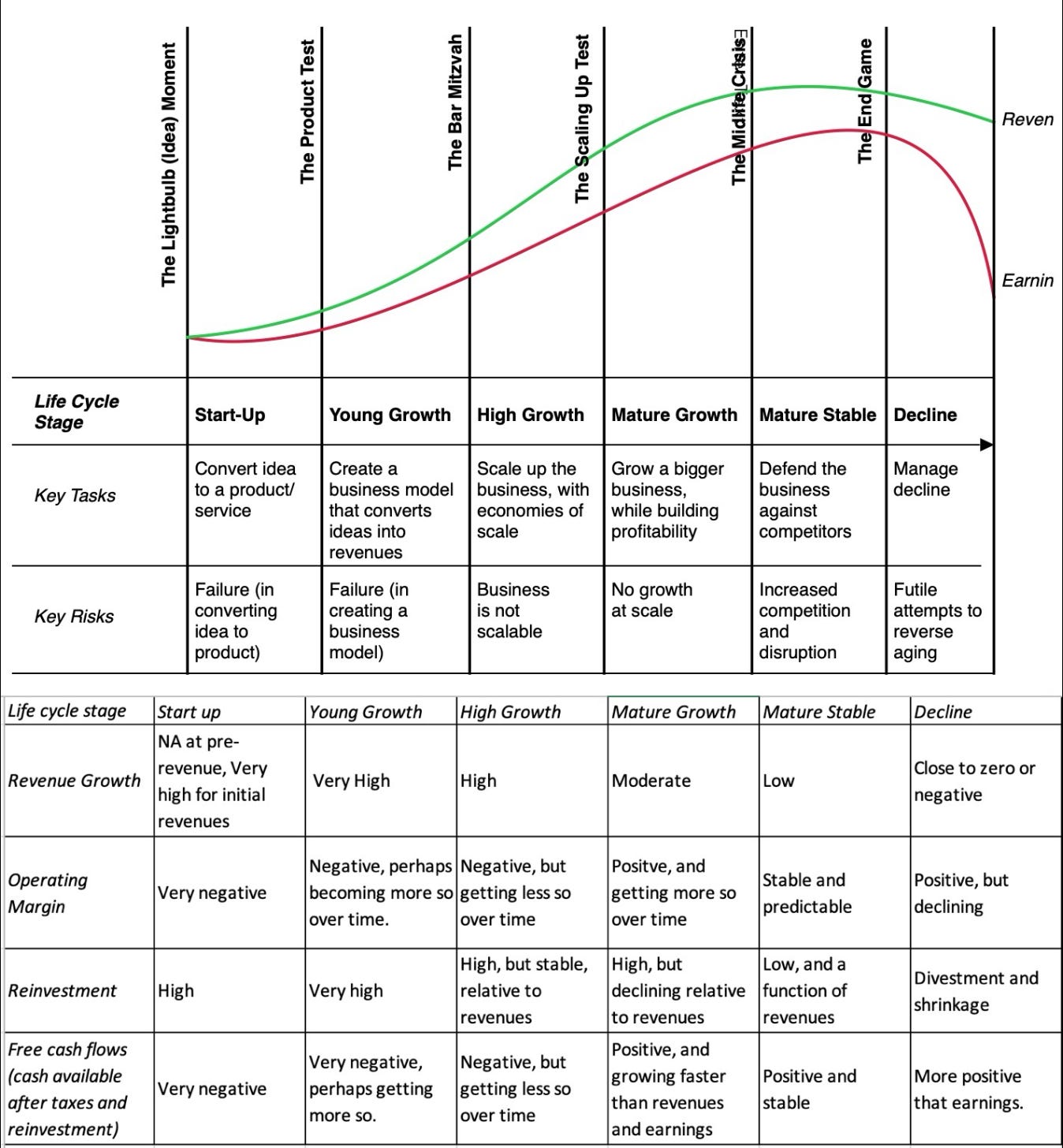

It’s useful to define what is the picture of success for an African business i.e. what should a company look like at maturity once the founders have executed everything that they need to execute and now the business is generating significant free cash flow for their shareholders. To start, it’s useful to borrow from Aswath Damodaran, a guru of modern financial analysis, especially company valuation. He has written an excellent article in his evergreen blog called “The Corporate Life Cycle: Managing, Valuation and Investing Implications!”. In it, he talks about the corporate life cycle from start-up to maturity and the different implications in terms of capital structure, use of cash flows, financing decisions and valuation. He produces this diagram;

Source: Aswath Damodaran;

Most African start-ups are between the start-up stage and high growth stage. We’re interested in companies that are in the Mature Growth and Mature Stable stages of the corporate life-cycle. Moreover, they should be at least a generation old so as to be replicable by existing founders i.e. within a generation and my lifetime, I can achieve similar success. Finally, they should be in the services sector given that Fintech is a service industry that requires a mix of tech infrastructure and licensing to serve clients.

Using this criteria, the companies that emerge are;

MTN Group;

Safaricom;

Vodacom Group;

Equity Bank Group;

Access Bank PLC;

These companies are all in the mature growth stage, are a generation old in terms of their existing shape, have Pan-African operations, are cash-flow positive and all provide digital financial services. One can argue that they may not yet be at their peak given they’re still growing, but given that they all issue dividends, it can also be argued that they are not fully prioritising growth.

Source: Different Company Financials - MTN Figures are skewed due to significant losses in Nigeria that affected net earnings, their PE ratios look different using EBITDA. Exchange rates are as at 6th December, 2024

All these companies are generating over US$ 1.0 billion in revenues and all of them are profitable. Financial services contribute significantly to the incomes derived from the Telcos and this contribution is growing. Apart from Access Bank, all these companies are worth over US$1.0 billion with Access suffering from the significant depreciation of the Naira. In normal times, Access’ metrics should be at least triple their existing dollar values. Vodacom is the largest amongst these and it’s worth noting that they’re a major shareholder in Safaricom. Using the criteria of being at least one generation old and being in the service business, Vodacom is the most successful and is therefore the pinnacle of commercial success in Africa. From a Revenue perspective, MTN Group is the biggest and in normal times would have a higher valuation and higher profits. Nonetheless, what is “normal” in Africa? If you’re building in the continent then depreciations and macro volatility will be part of the game.

To this end, one can argue that as African Fintechs scale and reach the mature growth phase in the corporate life-cycle, they should expect in a best case scenario to approach the success of Vodacom. What this means is that they should;

Have revenues in excess of US$ 10 billion per annum sourced from multiple countries;

Have net earnings in excess of US$ 1.0 billion;

Trade with a Price to Earnings Ratio of 12x - 15x;

This would mean a valuation of US$ 12 - 15 billion;

Operate in multiple countries with most in-country subsidiaries being profitable. Ideally, run big operations in at least 2 of Nigeria, South Africa and Kenya;

Whilst the Price to Earnings Ratio is not a robust measure of intrinsic value, at least it is how mature growth companies are evaluated as opposed to earlier stage such as revenue multiples. Fundamentally, it’s an acceptance that at that stage you should be profitable and the key things to measure are earnings growth and earnings quality which are all encapsulated in the PE ratio.

There has never been an African company that is valued at US$ 100 billion. The largest company in the continent is Napsers with a market cap of US$ 43.61 billion largely due to its stake in Tencent. Naspers is therefore not necessarily representative of an ‘African Company’ generating the bulk of its revenues in the continent. It’s therefore not realistic to estimate terminal market caps in excess of even US$ 10 billion for an African start-up. This foundational reality is driven by;

A small market encapsulated by a sub US$ 2,000 GDP per capita across the continent;

Capital restrictions that lead to aggressive currency movements;

Infrastructure constraints that lead to fragmented supply chains with the final outcome being high inflation;

Geographical issues in terms of the sheer size of the continent and the lack of river systems that enable low cost trade - This video made from an excerpt from Thomas Sowell’s book “Conquests and Cultures” gives a great overview of how difficult it was and continues to be to trade across the continent;

If we assume that most African Fintechs that are scaling will reach this terminal stage in 10 years time, then if we assume the economy doubling in 10 years (unlikely), we can double some of the existing metrics. In 10 years, time a successful African Fintech can look at having the following core metrics;

Revenues in excess of US$ 20 billion;

Net earnings in excess of US$ 2 billion;

Trade at a similar PE of between 12 - 15x with this lower PE reflecting the challenges of trading in the continent;

Have a valuation of at least US$ 25 billion; (rounded up)

It would be unrealistic to expect anything more than this. One can argue that some of the large Fintechs in Africa are building for the global market. Be that as it may, very few have actually achieved meaningful success outside of the continent. Therefore this premise is yet to be tested and not worth discussing. That’s not to say that it’s impossible, but I would be speculating.

Building towards a US$ 25 billion Outcome

We have defined what a terminal outcome looks like based on the success of existing African business. As an African Fintech, you’re aiming for the success of a Vodacom or an MTN. If you’re a licensed Challenger Bank you’re aiming for the success of Access Bank or Equity Bank Group. For the latter, hopefully you can build a bank that has way better operating leverage than existing banks therefore attracting a higher P/E or Price to Book valuation than the existing players. Nonetheless, within 10 years and given Africa’s market you’re aiming for a 25 billion dollar outcome. The question therefore is how do we get there? We’ll define why staged funding rounds are a necessary element of building a VC funded business, introduce a fictional payments company, walk through its growth and ask how plausible it is for the company to become a US$ 25 billion company within 10 years of its Series C.

The Onion Theory of Risk

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.