# 62 - Selling to Banks Part 2: Navigating Inertia and Closing the Deal (Free Post)

Increasing your odds of success when selling to Banks

Illustrated by Mary Mogoi - Website

Hi all - This is the 62nd edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

Sponsored by Skaleet

Complement, Don’t Compete, with Your Legacy Core

Changing out entire core banking systems can be a risky strategy with uncertain outcomes if not managed properly. It can make sense for large banks to retain their core systems, as the Skaleet platform offers a solution that complements, rather than replaces, existing cores. Banks can leverage Skaleet to run new digital propositions as an extension of their legacy core, which helps minimize the risk associated with full system migration. This dual-core approach allows banks to innovate without disrupting their primary system, preserving the trust and stability their customers rely on. This also enables deeper functionality than you’d get by just adding an engagement layer on top of your existing core.

Skaleet’s API-first design seamlessly integrates with legacy systems like Flexcube, Finacle, and Temenos, supporting fast, low-risk digital product launches. By creating standalone digital propositions, banks can explore new customer segments without disrupting their broader operations—a valuable solution for banks looking to modernize safely whilst avoiding over reliance on their existing core platform providers.

Introduction

Last week, we explored the people behind the bank and their unique circumstances. Margaret, the CEO, is like Game of Thrones’ Caitlyn Stark—balancing caution and transformation. David, the CIO, is a trusted advisor akin to Tyrion, eager for change but realistic about its challenges. The key takeaway for Founders and tech vendors is that selling to banks means understanding their complexity—a risk machine driven by humans navigating both professional and personal pressures.

This week is a continuation of that discussion but this time focusing on some of the sales tactics that in my view offer the most leverage. The way to think about leverage in this case is through some examples. Over 12 years ago, Michael Lewis wrote a fascinating article about his time with Barrack Obama who was then the president of the USA. In the article, they went into the challenges of running a country such as the USA and the complex decision one has to make on a day to day basis. Obama said “You’ll see I wear only grey or blue suits. I’m trying to pare down my decisions. I don’t want to make decisions about what I’m eating or wearing. Because I have too many other decisions to make… You need to focus your decision-making energy. You need to routinise yourself. You can’t be going through the day distracted by trivia.” Obama was making the case that to be productive, he reduces distractions so that he can focus on the few things that matter.

Great entrepreneurs like Peter Thiel, Elon Musk, and Steve Jobs share a similar approach: they focus on what matters most. As Johnny Ive recalled, Jobs once said, "What focus means is saying 'no' to something that you believe with every bone in your body is a phenomenal idea." Like Obama routinizing his life, these leaders use first principles thinking—breaking problems down and targeting what drives the biggest impact.

Sales, like leadership, requires identifying and focusing on the key leverage point at each stage of the process. Great salespeople excel at unblocking what’s holding up a deal. Whereas there’s plenty of sales literature out there, this week I’ll focus on what I’ve come to find as the key stages of a sales process and give my insights on what people need to get right at each stage. The article will be structured as follows;

General Overview of the Sales Process and the Key Stakeholders;

Understanding your product archetype;

The value of positioning;

The Sales Pitch;

Navigating the stakeholders (Negotiation);

As inspiration, I’ve relied on 5 books that I’ve found useful for sales. They are;

The Challenger Sale by Matt Dixon and Brent Adamson (h/t Ahanna from Finverity);

Selling 180 by Tom Batchelder (Tom was our in-house coach at Sote and I highly recommend him as a coach);

Overview of B2B Sales Process

I won’t cover the entire sales process but will highlight the areas that truly matter. In B2B sales, the journey typically moves from prospecting, where potential customers are identified, to qualification, assessing their needs, budget, and decision-making authority. It progresses through the presentation phase, addressing objections, and culminates in negotiation and closing. Each stage is influenced by key stakeholders: Margaret the CEO (Economic Buyer), who controls the budget; James the Product Owner (Champion), your internal advocate; Peter the Director of Corporate Banking (Decision-Maker), with final approval; and David the CIO (Technical Buyer), ensuring technical fit. Others, like Esther the CFO (Influencer) and Susan the CRO (Compliance), shape decisions and enforce regulations.

While ample literature exists on B2B sales processes, I’ll focus on the areas that matter most. To start, even before prospecting, it’s crucial to understand your product and its place in the market.

Understanding your Product - the PMF Framework

In my first article since restarting the newsletter,I discussed the Sequoia Product Market Fit (PMF) framework and its emphasis on understanding how customers perceive problems. According to Sequoia, problems fall into three archetypes:

Hair on Fire: These problems have a clear, urgent need, and buyers are focused on finding the best solution among competitors. Examples include digital banking platforms, where enterprise guides like Gartner or Forrester help buyers compare options.

Hard Facts: These are pain points widely viewed as unsolvable, with the market relying on workarounds to adapt. A status quo exists around the problem being "impossible" to solve.

Future Vision: Revolutionary products that enable entirely new realities, like autonomous vehicles, often sound like science fiction—understood conceptually but met with skepticism about their feasibility.

The two most relevant frameworks for banks are Hair on Fire and Hard Facts. To win in Hair on Fire markets, you need a superior solution and clear differentiation—examples include digital banking platforms like Backbase, CR2, and M2P Fintech. For Hard Facts, success comes from educating the market on how you’ve solved a previously "impossible" problem, as Cellulant and Craft Silicon did with mobile banking in the early 2000s

Failure happens in the following manner;

For hair on fire problems - you fail to differentiate and are out-competed;

For hard facts problems - either your solution is not convincing or the problem is not worth solving;

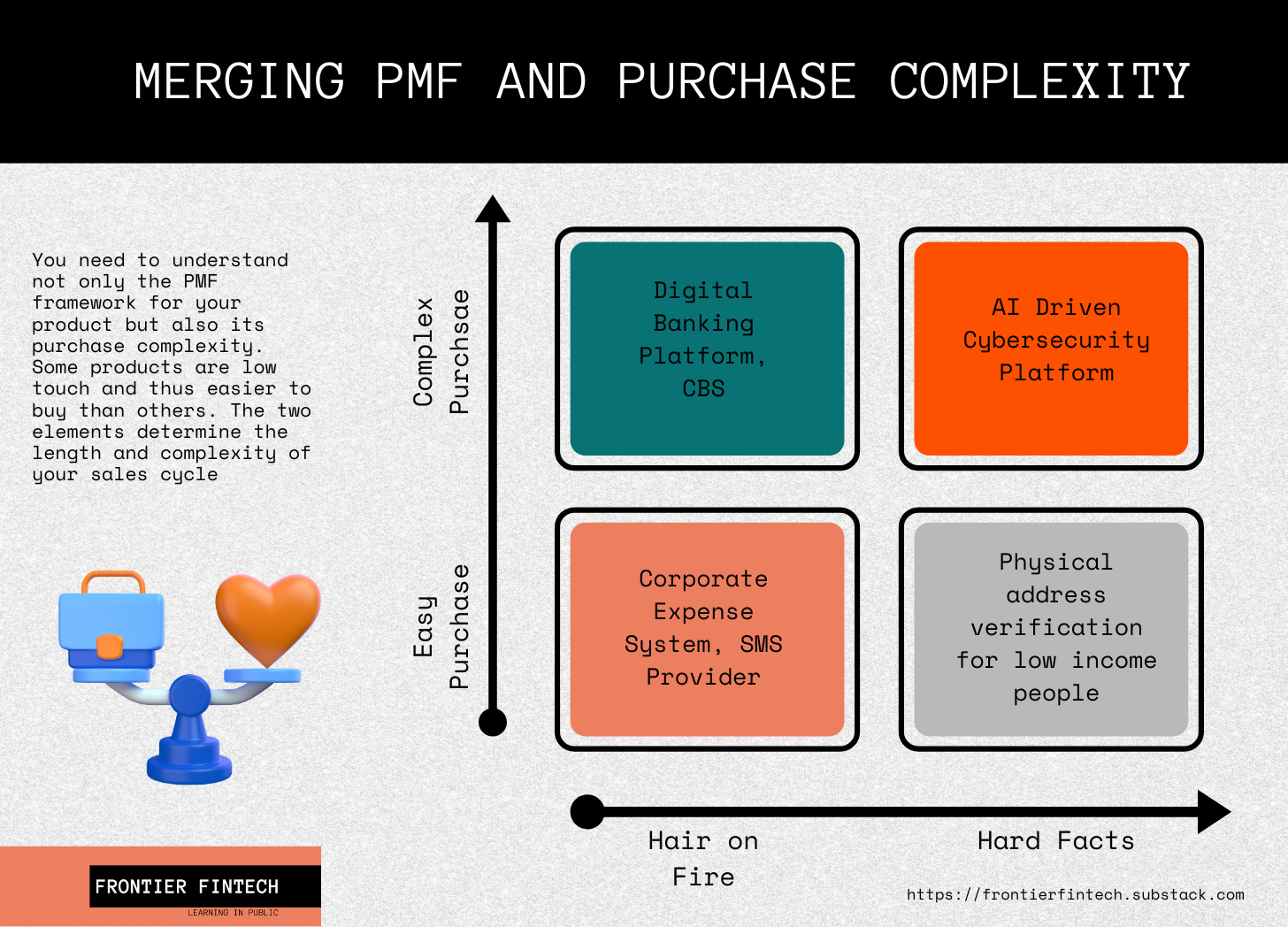

An additional factor to consider is the complexity of the purchasing process. For instance, Core Banking Systems are a Hair on Fire problem. Everybody knows that it’s good to have a modern core banking, but migration is costly and complex. On the other hand, a corporate expense solution targeted at bank employees is easy to buy. It’s not only useful to understand your PMF framework, it’s important to also understand how complex a sale would be for your product. The diagram below makes it clear. For instance, a Digital Banking Platform is a hair on fire problem, everybody understands the need and can compare alternatives in the market but selling one is a complex multi process sale. On the other hand, a corporate expense solution is also hair on fire but can be thought of as low-touch as the bank can pilot it in one department and scale from there with little to no integrations required.

Your product’s archetype should shape how you sell and structure your company. Solving a Hard Facts problem requires patience—a 2-3 year runway to educate the market before major breakthroughs. Once you close your first deal, scale quickly to seize the opportunity. Most category-defining businesses weren’t first movers—Facebook followed MySpace, and Google followed AltaVista. In a Hair on Fire market, the priority is investing in product and sales to create and clearly communicate differentiation. For Hard Facts with complex purchasing processes, you face two challenges: educating the market on your product and teaching them how to buy it.

The key thing for a founder or vendor at this stage is;

Develop unique insights into your product and market—be brutally honest about whether it’s Hair on Fire or Hard Facts and the complexity of your sales. Domain expertise is invaluable here.

Map out your sales process and study how other vendors have succeeded. Deep knowledge of your differentiation and sales strategy is critical.

One thing that I’ve come to appreciate is that if you’re building a product that is intended to improve customer outcomes and is a hard facts problem, you’re better off just going straight to the customer rather than selling to banks. Imagine if Nubank wasted 4 years trying to sell its credit scoring solution to banks? I can’t emphasise this enough, I would advise any founder that has an interesting approach to customer care to serve the market directly.

With your product’s market fit clear, the next crucial step is positioning.

Product Positioning

The old brain is self centred - Do not assume that it has any patience or empathy for anything that does not immediately concern its survival or well-being;

The old brain seeks contrast - Without contrast, the old brain enters a state of confusion which ultimately results in delaying decision;

The old brain remembers what’s tangible - The old brain cannot process concepts like ‘flexible solution”, “integrated approach” or “scalable architecture”;

The old brain remembers beginning and end - Placing the most important content at the beginning is a must, and repeating it at the end an imperative. Keep in mind that anything you say in the middle of your delivery will be mostly overlooked;

The old brain is visual - This implies that visual processing enforces the old brain first which can lead to very fast and effective connection to the true decision maker;

The old brain responds to emotion. The old Brain is strongly triggered by emotions that directly impact the way information is memoriised and processed;

Selling 180 - Tom Batchelder

Positioning is something we all grasp intuitively but often fail to execute properly. I for one struggled at first but I’ve become good at positioning. April Dunford, who writes extensively on this topic, defines it as "the process of establishing how your product uniquely delivers value to a specific set of customers, distinguishing it from competitive alternatives." In essence, it’s about explaining your product in a way that makes its value clear and easy for customers to grasp.

According to April Dunford, positioning is built on five key components that collectively define how a product is perceived in the market:

Competitive Alternatives - Identify what customers would use if your product didn’t exist. These are the solutions your customers currently consider as viable alternatives, which can include direct competitors, substitute products, or even manual workarounds.

Key Differentiators - Determine what makes your product unique compared to the competitive alternatives. This includes specific features, capabilities, or approaches that set your solution apart in a meaningful way.

Value - Understand the value your product delivers as a result of its differentiators. Focus on the benefits customers gain, such as time savings, cost reduction, increased efficiency, or better outcomes.

Target Market - Define the specific group of customers who benefit the most from your product. These are the customers for whom your differentiators and value proposition are most relevant and impactful.

Market Category - Choose the category that best frames your product in the minds of customers. The category helps them quickly understand what your product is, what problem it solves, and why they need it. Selecting the right category can significantly influence how your product is perceived.

In our previous article, the idea was that we were selling a digital banking platform to the corporate banking team at the Bank of Westeros. If we were to use this approach, then this is how the positioning framework would work;

Competitive alternatives - the bank could continue using whatever they’re currently using or work with a solution from Temenos, Backbase, Finastra or CR2;

Key differentiators - In our case, we could differentiate ourselves by our advanced integration platform as well as our suite of APIs that enable the bank to innovate whilst ensuring data integrity;

Value - The value of our technical differentiation is that the bank can now ensure that its corporate banking product teams can continue building out suitable products for its customers given that our integration platform abstracts all the complexity of integrating into their core banking system. They can now innovate like a tech company whilst protecting their data integrity;

Target Market - The target market could be banks in East Africa with strong corporate and wholesale banking departments that are looking to grow their market share in these segments;

Market Category - Our market category is the Digital Banking Platform market;

The goal is a clear, simple positioning statement that resonates with your audience. For example: “We help corporate banks launch new products quickly while staying stable and secure.” This statement addresses key concerns for buyers, especially the Director of Corporate Banking.

The following things are critical in developing your positioning statement;

Drop Intellectual baggage - One thing I’ve come to understand through my own personal journey is that intellectual baggage stops many people from being able to simplify things. Humans are generally lazy, we look for simplifications so that we can understand things. Speaking to humans therefore requires you to speak to their basic selves and not their enlightened selves. Too often, a typical founder or CEO is very intelligent and has an enlightened understanding of their product. The outcome is a tendency to use sophisticated language and concepts to explain their product thus losing people. The greatest marketers are able to make their messaging super simple and targeted at our basic selves. Consider these examples;

Apple (early iPod) - "1,000 songs in your pocket."

Slack: - "Be more productive at work with less effort."

Dropbox - "Your stuff, anywhere."

Uber - "Tap a button, get a ride."

Zoom - "Video conferencing that just works."

Simplify your message—it doesn’t diminish your product’s value.

Cross-functional alignment - To develop world class positioning requires cross-functional alignment. The best way to do this is to get product, sales and marketing together to develop it under the guidance of the CEO. Insights from product should be combined with insights from sales to sharpen the positioning statement and the CEO should ensure that marketing is keeping things super simple;

Targeting banks based solely on size often limits your market and weakens your positioning. Instead, focus on ownership, management style, strategy, and commercial focus. For example, tier 3 government banks may behave like parastatals, while owner-operated tier 1 banks often prioritise innovation and growth. At Sote, we initially targeted tier 2 and 3 banks but found more success with tier 1 banks that aligned with our value proposition.

Through PMF insights and your positioning process, develop a unique and truthful market perspective. This should serve as the foundation for all sales materials, including decks, your website, and FAQs.

The Sales Pitch

Now that you’ve identified your place in the market using the PMF framework and positioned yourself with a clear target and value proposition, you’re ready for the sales pitch. Before pitching, ensure you’ve answered these key questions:

Why change: Why must the bank adopt your corporate digital banking platform? The case for change must outweigh the inertia of the status quo.

Why now: What market dynamics make this change urgent?

What matters most: Among the factors influencing their decision, which is the most critical?

Who else cares: Are there other stakeholders in the buying process you haven’t identified?

What I’ve found works the best when it comes to pitching is having a point of view in the market and communicating this point of view clearly. As highlighted in The Challenger Sale and The Jolt Effect, a great vendor acts as an educator, teaching the market their perspective. April Dunford’s pitch structure supports this approach with two key elements:

The Set up;

Explain through your experience your insights into the market and the customer’s situation - Show them that you have truly differentiated insights;

Walk them through the different alternatives that the market uses to deal with the problem;

Tell them what the perfect world should look like;

The Demo;

Show them how your product solves the problems identified in the set-up;

Proactively walk them through the different objections that a customer may face;

Close with a clear ask for the next steps;

Let’s make it more practical using our digital banking platform example. In this Pitch, I managed to get James to organise a meeting with his boss Peter and the CIO David.

Scene: A conference room at the bank, everyone seated. You’ve just finished introductions.

VENDOR: Thank you for making the time. I’ve got quite an interesting background, I used to head corporate product at Green Bank a number of years ago before I transitioned to building this business so I have the unique advantage of once having sat at your side of the table. I won’t waste time so I’ll get straight to it. Peter, would I be wrong to say that your customers are becoming more and more sophisticated and are asking for more from your digital platforms?

Peter - Nope, you’re right.

VENDOR: I remember once a customer asking me when I was at Green Bank whether our platform could help them forecast their cash trends using historical banking data. The market is getting more savvy particularly as the management at these corporate customers shifts towards millenials and Gen-Zs. Peter you’re therefore under a lot of pressure from your clients particularly at the golf club (Peter at this stage starts shifting in his chair). Not only do you have to provide a world class experience, you have to keep improving your products on a regular basis.

VENDOR: The challenge though is that you have to provide a world class experience whilst ensuring that at the back end you have data integrity and your core systems are secure. Most companies that build these corporate platforms tend to focus on the front-end customer facing features and not the integration platform that sits between the customer and the core banking system. What you then get often is unbalanced GLs as well as cyber attacks due to poor API security.

VENDOR: David, I’m sure you’ve experienced this and Peter, I’m sure you’re spending more time in IT audits than out meeting your clients. Your platform has the body of a Ferrari but the chassis of a wheelbarrow.

DAVID: You’ve hit the nail on its head. Those APIs are giving us nightmares;

PETER: Laughs sheepishly before stating - It’s like you have been stalking me;

VENDOR: Now, imagine a perfect world: your corporate banking teams can focus entirely on building innovative products for your customers without worrying about whether those products can integrate with your core banking system. A world where integration is seamless, security is airtight, and the bank is set up to transition smoothly to AI-powered banking when the time comes. That’s the world we’re building.

The Demo

(You pull up the product demo on a screen.)

VENDOR: Let me show you how our solution works. At its core, our platform simplifies and secures the integration process. This means your product teams can build and deploy new corporate banking solutions faster, without being held back by technical bottlenecks.

(You click to a visual dashboard showing integrations.)

Here’s an example: Say James’s team wants to launch a new cash management tool for corporate clients. Instead of spending months figuring out how to integrate it with your core banking system, they can use our platform to abstract all that complexity. The platform ensures data flows securely and consistently between the new tool and your core system, allowing James to focus on delivering a great product.

JAMES (Product Owner): How does this handle API security? That’s one of our biggest concerns when integrating with third-party tools.

VENDOR: Great question, James. API security is like locking every door in a building, but the locks change depending on who’s trying to enter. Traditional methods focus on keeping attackers out, but APIs are doors that need to stay open for communication. Our approach adds an extra layer by checking details like who’s making the request, where they are, and what device they’re using. We also hide sensitive data using tokenization and keep an eye on every API request in real-time to catch anything unusual. This way, even if someone gets in, they can’t misuse the system or move around freely.

PETER (Director of Corporate Banking): This sounds promising, but our focus is growth. How does this help us grow market share?

VENDOR: Peter, this platform enables your team to launch new products and services faster than your competitors. The thing is Peter, banking is changing and what matters is that you’re able to adapt and eventually this will reflect in your product positioning. Look at Red Bank for instance, they decided to focus on hosting golf tournaments instead of innovating and now they’re slowly losing market share. What matters to you Peter is that you can respond to your clients’ needs.

DAVID (CIO): You’ve mentioned the transition to AI banking. How does this platform prepare us for that?

VENDOR: David, our platform isn’t just about integration—it’s about future-proofing. As you explore AI tools for fraud detection, credit scoring, or personalised recommendations, our platform ensures these tools can plug into your core banking system seamlessly. Remember that the integration platform is largely about data and data integrity thus preparing you for AI. You can adopt AI without a major system overhaul.

Front-load objections

VENDOR: Now, I know this may raise concerns. You might wonder: Can this platform handle the complexity of your specific core banking system? The answer is yes—we’ve designed it to integrate with both legacy and modern cores. Another concern could be: Does this add another layer of complexity for your IT team? On the contrary, it reduces complexity by automating many manual processes.

DAVID CIO: Yes, I was about to ask about how you handle integrations and whether you have done this with Finacle before.

The Close

VENDOR: I hope this has shown you the possibilities for your bank. My ask today is clear and simple: Let’s schedule a deeper technical session with your IT team to map out how this would work specifically for your core system. If you’re open to it, I’d also love to provide you with a trial environment where James’s team can test out the platform with a use case of their choice. Does that sound like a good next step?

DAVID (CIO): I think a technical session makes sense. Let’s coordinate with my team.

PETER (Director of Corporate Banking): Agreed, but I’d also like to see how this impacts the cost structure for corporate product innovation.

VENDOR: Absolutely, Peter. I’ll include a breakdown in our next discussion including a business case done in your bank’s format to show the ROI of the project. We’ve taken some numbers from your audited financials to inform our assumptions. James, any use case you’d like to prioritize in the trial?

JAMES (Product Owner) - Yes, a solution for automating reconciliation for our top corporate clients would be a great start.

VENDOR - Perfect. I’ll follow up with those details. Thank you all for your time today—I’m excited about what we can build together.

Here are some of the things I’ve found work in a Sales Pitch;

Ensure there’s alignment by asking people to speak. When you make a point, ask people directly for their input e.g. Peter, am I wrong to say that your innovation efforts have stalled due to all the technical problems you’re facing? This forces people to be engaged and to think;

Don’t be afraid of discomfort. In Africa, particularly East Africa we’re focused on being consensus seekers and making people feel good. Remember, sales is about getting a deal done, not making people feel comfortable. Drive home the point that they’re currently screwing up to the point that they even laugh at themselves about it.

Embrace your role as an educator - You can build trust when you’re able to teach your buyers new things about the market and give them unique insights. Too often vendors just blurt out product features rather than giving people unique insights about the market. If you start your sales pitch with features, you’re unlikely to succeed. Note how the vendor explained his insights on API security

In Chris Voss’ book, “Never Split the Difference”, he talks about performing an accusatory audit. “List the worst things that the other party could say about you and say them before the other person can.”. The idea here is that it makes sense to front-load objections before they do. It builds trust and marks you out as a trusted partner.

The key aspect of this phase is to get that alignment that your solution matters and having your buyers commit to a next step that is actually tangible. In this case setting up a test environment and getting James to work on a dummy product. You want clarity at this stage and not confusion.

Objections Handling and Negotiation - Navigating the Sales Process

Again, at this stage, I’ll focus on listing out the key things that I’ve seen work well. People may have different experiences. You have successfully pitched the bank and have set up a demo. The wheels are moving and your work is to ensure that they move to a successful close as quickly as possible. This means a signed contract and a first invoice out to the bank. This is usually the hardest part. According to Matthew Dixon in his book, Jolt Effect, 60-80% of deals end in no decision. Some insights that I think matter;

From the Challenger Sale and Jolt Effect the insight is that Inertia is your biggest enemy. How people deal with it is a key determinant to success. The thing I’ve found that works is being assertive whilst being an educator. Inertia shows itself in different forms. You may end up getting weird questions that don’t even make sense or you may be told of processes that you’ve never heard of. Your role is to spot the BS early and deal with it. For instance, I remember a bank we were pitching to. Our solution was a dashboard that didn’t need integration into any system whatsoever. Some guy who doesn’t even have a technical background asked “can you share your APIs?”. I tried my best to hide my displeasure but I quickly reminded him that no integrations are required. Such a question can trip you up, some vendors may decide that what they need is to implement APIs but what they need to do is to actually diagnose that question as a symptom of inertia. Be assertive and educate.

Position yourself as a trusted adviser by sharing your unique market insights freely. For example, engage Risk teams by explaining pitfalls in existing data protection methods and why your approach is superior. The goal isn’t just to gain approval but to build trust and credibility. People love getting new insights.

Invest in your champion - In our case this is James the Product Owner. He really wants this project to succeed because it may give him a leg up in his career. Invest time and energy to build this relationship. Your champion will help you handle objections before they even arise. What you must understand though is that your champion has his foibles. For instance, he may propose a strategy that is easier for him to execute without necessarily being the best strategy to reach close. Your champion should be able to recite your sales pitch in his sleep.

The Power of No - Like Chris Voss says in his book “It comes down to the deep and universal human need for autonomy. People need to feel in control. When you preserve a person’s autonomy by clearly giving them permission to say No to your ideas, the emotions calm, the effectiveness of the decisions go up, and the other party can really look at your proposal.” People naturally want to avoid rejection but the counterintuitive advice is to proactively seek it. Put your clients in a position to say no and this makes things move faster than before. For instance, we were dealing with a real shark in the banking sector. A grizzled executive who cared less about our solution and more that we had customers he wanted. After we pitched to him, he went quiet and completely ignored us. We then wrote to him; “Sir, we’ve emailed a number of times without response, is it safe to assume that we won’t be proceeding with this project?”. We got an immediate response and a meeting the next day. Moral of the story, actively seek out rejection.

There are a few tricks that I found useful during meetings such as mirroring and labelling.

Mirroring - Mirroring involves repeating the last few words or the most important words that the other person has just said. It helps to encourage the speaker to elaborate, showing that you are actively listening and interested. An example;

David: "We’ve been struggling with integrating this new software into our workflow."

You: "Integrating the new software into your workflow?"

David: "Yeah, it’s been causing delays because it doesn’t align with our legacy systems."Labeling - Labeling involves identifying and acknowledging the other person's emotions or feelings by saying something like, "It seems like..." or "It sounds like..." This helps to diffuse tension, build empathy, and create trust. The goal is not to agree or disagree but to validate their perspective. An example;

Susan: "We have been having major issues with some of you Fintechs due to the new data protection law that has been implemented”

You: "It sounds like you’re feeling frustrated because Fintechs are not taking data protection seriously"

Susan: "Exactly. This is serious work, we’re a bank and our reputation matters."

Mirroring and Labelling are great at driving empathy and should be used particularly with the key stakeholders who can be blockers such as procurement, risk and finance.

Wrapping it Up

Ultimately every sales journey is different, not all products, vendors and banks are the same. Nonetheless, it’s important to understand the value of placing your product in the PMF framework, doing solid positioning work, aligning your sales pitch to your materials, executing the perfect sales pitch and navigating the objections process assertively whilst educating your buyers. If you get these things right, your odds of success can be better. As a vendor you’re taking multiple shots and the aim is to get marginal gains for each shot so that your overall odds of success are better. This applies to sales, making improvements in each area and particularly the areas we discussed.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora@frontierfintech.io