#59 CBK's Push for Faster Payments, What it Means and Why it Matters

How Faster Payments will light the spark to Kenya's Fintech Boom

Illustrated by Mary Mogoi - Website

Hi all - This is the 59th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. Support Frontier Fintech by becoming a paid subscriber🚀

Sponsored by Skaleet

Accelerate Digital Banking with Skaleet’s Next-Gen Core Banking Solutions

Large banks within the continent need to be seen as paragons of stability in the market, but at the same time they need to respond to rapidly evolving customer preferences particularly with Gen-Z. A core plank in such a dynamic is the ability to quickly launch digital propositions. This could be digital propositions that are segment specific in their main market or could be propositions for their regional subsidiaries. Skaleet’s nex-gen core banking solutions empower banks to launch digital propositions with unprecedented speed, allowing them to capture new customer segments without major overhauls. Skaleet’s modular architecture allows for quick configuration of products like SME banking and youth-focused offerings, helping banks differentiate themselves and stay relevant.

With Skaleet, banks can roll out new features in real time and update their digital offerings in response to customer feedback without having to switch their entire core banking platform. The platform’s cloud-native design enables banks to move from concept to launch efficiently, putting powerful digital tools in the hands of their customers and reducing time-to-market from years to months. Moreover, Skaleet has a robust partner ecosystem that includes companies like SmileID, Paymentology and ComplyAdvantage that enable banks to launch fully functional solutions. - Contact Sales to Learn More

🔊🔊 Introducing Frontier Fintech Partner Pieces - We’re launching Partner Pieces, these are sponsored deep dives where I write about specific companies, organisations or initiatives. To maintain trust with my readers, I’ve highlighted my ethics policy here that should guide the Partner Pieces” 🔊🔊

Introduction

A couple of weeks back, my good childhood friend Amboko Julians, who also happens to be Africa’s foremost business journalist, gave me a call. He said “Samora, Central Bank have issued a statement about the new Faster Payments System and I was expecting you’d have something to say about it”. My mind immediately went back to an old Dave Chappelle stand-up comedy where he was making fun of Celebrity culture. Specifically, the tendency to always ask celebrities for their opinions even in domains that they know nothing about. In the video, Dave Chappelle references a situation (didn’t happen), where MTV during September 11th, reached out to Ja Rule to get his thoughts on what’s happening. Chappelle rightfully questions, why on earth does Ja Rule’s opinion matter on such a thing? This was my self-deprecating millennial self-speak. I was like, “Why should I have already said something about the Central Bank press-release?”

Once I processed the question, what Amboko was saying was that “I respect your views on Fintech in Africa and I’d appreciate your input into this”. With that in mind, I walked him through my initial thoughts and what I anticipate will happen to the Kenyan Fintech ecosystem. I’m learning that my voice matters and that is represented in my growing and deeply engaged subscriber base. I then thought it useful to write something about the proposed Faster Payments System (FPS) in Kenya. This article is about breaking down a number of things to drive clarity about Faster Payments in Kenya. It was one of those moments where a seemingly nondescript press release by the Central Bank went under the radar despite its immense significance in terms of the future of Fintech in Kenya. This week, I’ll go deeper into what Faster Payments would mean for the Kenyan ecosystem, but first, it’s important to understand some foundational concepts. This article will be structured as follows;

What are Faster Payments Systems;

How do they fit into Kenya’s existing Payments Ecosystem;

What will Kenya’s Faster Payments Look Like?

Why could it fail? - An exercise in inversion;

Implications for the Kenyan Fintech Ecosystem looking at Banks, Fintechs and M-Pesa;

What is Faster Payments?

How Central Banks view Payments

To even begin understanding faster payment systems, one has to understand how Central Banks view payments. James Scott in 1998 wrote a fantastic book called “Seeing like a State”, one of the core ideas behind it was that the State requires legibility in society so as to implement policy. This need for legibility nonetheless can have disastrous consequences and lead to “high-mindedness”. For me a key insight was that it’s important to understand the institutional and policy incentives that underpin an organisation be it a bank, a judicial system or any other institution for that matter. It’s therefore important to understand how Central Banks “see” payments.

In my view, this is one of the biggest causes of misunderstanding particularly amongst industry commentators, not understanding a Central Bank’s payment mandate. Across the world, Central Banks have been very active in “innovating” on digital payments. China’s PBoC has been toying around with CBDCs despite the success of Tencent and Alibaba in solving for digital payments. The Central Bank of Ireland recently released a Strategy report on Faster Payments and the Brazilian Central Bank has piloted Drex, its own CBDC despite the overwhelming success of Pix. Recently, the Governor of the Bank of England Andrew Bailey had this to say about Central Bank Digital Currencies;

"For commercial bank money to function effectively, it must keep pace with the needs of its users. Our work on retail CBDC is considering these trends in the payments landscape closely. Absent innovation in commercial bank money, central banks may be left as the only game in town insofar as retail payments innovation is concerned. That is not my preferred outcome, but not one that we should rule out.”

Essentially, even with high inclusion rates and a world class Faster Payments System, the Bank of England continues to push the envelope in terms of retail payments innovation.

Whilst introducing their National Payments Strategy back in 2021, this is what the CBK had to say;

Central banks have always been about money – how money is created, how money is held, how money is exchanged and how money or monetary value is moved. In turn, these roles accord particular core functions to any central bank – monetary policy, bank supervision, foreign exchange and payments oversight. Payments, therefore, has been an integral feature of how CBK has operated since its inception in 1966. This Strategy carries on from that tradition and heritage of supporting Kenya’s quest for sustainable development of her people.

To understand why this is so important to Central Banks, people must understand the role of money as a public good. A public good is something that is available for everyone to use, without reducing its availability to others, and without people having to pay for it. Classic examples are clean air, street lighting, and national defence—everyone benefits from these without using them up or excluding others from enjoying them. The reason why the ability to pay is seen as a public good is because everyone has a right to earn income and thus contribute to GDP. Remember, GDP is the market price of all goods and services produced, key term being “market price” thus inferring a payment. It’s for this reason why Central Banks have always been involved in payments. Traditionally this has been through printing cash and building the infrastructure to distribute it across the country. Moreover, ensuring that cash is legal tender i.e. by law you must accept cash payments.

As payment methods digitise and payments become digital, it’s important that the Central Bank can maintain the ‘ability to pay’ as a public good. In addition to this, Central Banks must ensure that payment systems are robust and resilient to support economic growth. If payment systems fail, then by default the economy will struggle. We saw this with India’s demonetisation efforts. Given that economic growth is one of the mandates of most Central Banks, then the availability and resilience of payment systems is a core function.

Understanding Faster Payments System

Now that we’ve understood why payment systems are so important to Central Banks, it’s useful to look at Faster Payments. Central Banks are involved in all types of payments. At the high level, Central Banks manage higher value payment systems, these are usual Real Time Gross Settlements (RTGS) and Cheque Clearing Systems. At the lower end, many Central Banks participate primarily through distribution of cash. This has been changing in the past decade with the introduction of Faster Payment Systems (FPS) or Instant Payment Systems across the world. It’s important to understand what a Faster Payments System is.

A Faster Payments system, like UPI in India or Pix in Brazil, is a digital payment infrastructure provided and regulated by the central bank to enable secure, real-time payments across the country. By developing and managing this infrastructure, central banks play a foundational role in ensuring that banks, financial institutions, and fintechs can connect to a common network, creating a seamless ecosystem where funds move instantly and reliably. This central-bank-led infrastructure reduces reliance on private networks, promotes financial inclusion by reaching the unbanked, and fosters competition and innovation among financial service providers. As an infrastructure provider, the central bank also enforces standards for security, speed, and cost-effectiveness, making faster payments widely accessible and efficient for all citizens and businesses.

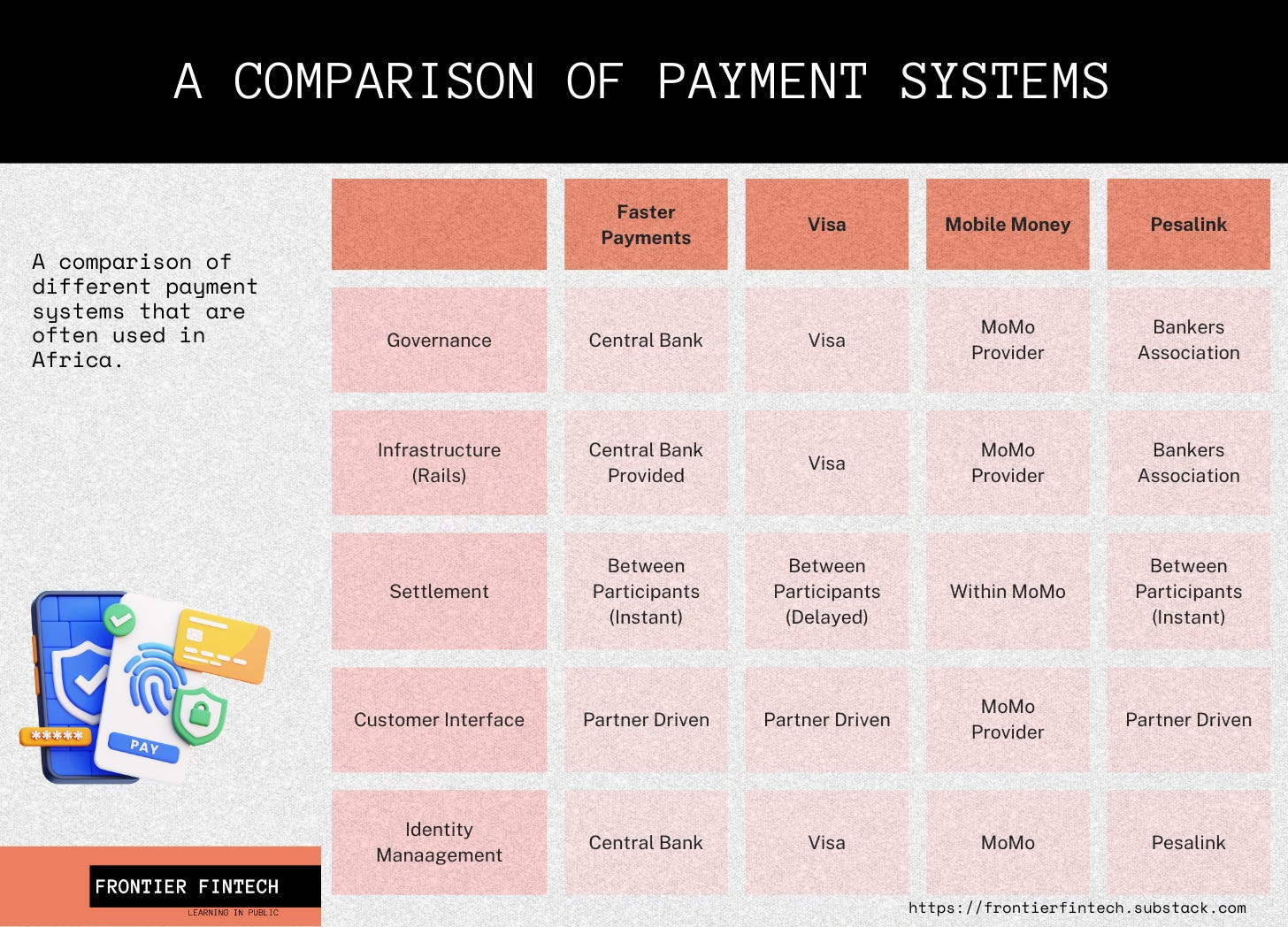

A payment system at least at the lower level needs to have 5 core elements;

Rules and Governance Frameworks - A set of rules covering things like complaints, refunds, fraud management and other similar issues;

Communications Infrastructure - Each payment is always an act of communication, payment systems therefore need systems to record payment messages as they happen. The biggest consideration here is often reliability and throughput;

Settlement Infrastructure - At the end of a payment communication, money must move between accounts. The settlement infrastructure manages the money movement element;

Customer Interface - This is where the client interacts with the payments system, it could be an app, branch, agent or card;

Identity Management - An internal way of identifying all the different users and participants within the payment system. In Visa or Mastercard, this is usually your card number.

The table below gives a general overview that enables a quick comparison between Central Bank Faster Payment Systems, Mobile Money, Visa and Pesalink.

The table above and the understanding of what matters to Central Banks in terms of payments can then answer the question of “Why do we need Faster Payments in Kenya when M-Pesa works perfectly”. This is a question that Amboko asked me in our call and most people would typically have.

The reasons can be broken down into two core reasons;

Foundational Reasons

Given its role in payments in the country, the Central Bank must provide a mechanism for people to pay that’s independent of private networks or companies. The same role Central Banks have with cash is the same they’ll have with digital payments. Even after launching Faster Payments, CBK will eventually launch a CBDC. It’s their role to play. Moreover, M-Pesa poses systemic risk to Kenya’s economy given that if it fails then the country’s economy is at risk given people won’t be able to transact. Of course, M-Pesa would argue that their reliability record is world class. However, that's not how governments see things. CBK has a role to play and it will play it.

Operational Reasons;

There are practical reasons why the Central Bank needs to launch an open Faster Payments network given the fundamental failures of other payment systems. In this case we’ll focus on Pesalink and Mobile Money given that Visa can perfectly co-exist with every other payment system in the world. I’ll just list them out;

Governance - Central Bank as a neutral entity is a better provider of open rails and an open ecosystem. Fintechs know how dangerous it is to build on top of Mobile Money from a commercial perspective given that your best ideas are often stolen or killed through pricing. MoMo players have a strong incentive to replicate promising business models given they’re a commercial entity and control the entire stack. I’ve heard of and experienced horror stories such as throttled USSD sessions, random pricing changes for remittance providers and other similar cases of skullduggery. From a Pesalink perspective, having banks govern payments means that they will prioritise payments so long as they benefit the banking system. This usually manifests in the larger banks designing payment process geared towards keeping liabilities within the bank;

Lack of Interoperability - payment systems such as MoMo are closed ended and not built for interoperability. Where interoperability exists, it’s based on bilateral agreements e.g. Safaricom and Airtel integrating their systems leading to higher costs and more bifurcation of the system;

The CBK believes that there are high transaction costs particularly in the retail payments space. This puts brakes on efforts to digitise payments and drive financial inclusion. Remember the CBK sees this from a ‘public goods’ perspective. For closed systems, the costs of maintaining the entire stack has to be monetised through higher charges;

Complexity in Payment Reconciliation - For businesses, reconciling payments can be time-consuming due to differing invoicing and notification standards across payment providers. Anyone who has run a business and had to accept multiple M-Pesa payments would understand this. Twiga had to build special in-house capabilities and teams just to handle payments reconciliations. At the end of the day, MoMo is SMS payments;

Limited Choice - Given that MoMo is closed loop i.e. M-Pesa for instance provides the entire stack, then there are limited options for the consumer in terms of customer experience. This therefore means that the ecosystem can only innovate at the speed of Safaricom. This is a binding constraint.

These reasons have necessitated a Central Bank driven payments system with a view of making Kenya a leader in the African Fintech ecosystem insofar as an open payment system will drive innovation.

National Payments Strategy 2022-2025 - What are the design considerations for the new Faster Payments System? What do I expect?

I think we now understand how Central Banks view payments and therefore why a Faster Payment System is very important. I am a huge advocate for a well managed faster payment system in Kenya. It’s therefore important to understand how this Faster Payment system is expected to look like given that the readers of this newsletter will need to inform their Faster Payments strategies. If it is designed in the way I expect, it will be a game-changer and I usually try my best to avoid using such terms.

To glean some insights into how Faster Payments in Kenya will look like, the Central Bank NPS strategy is the best place to begin. The NPS is a strategy document outlining the key design principles that will guide the development of a retail faster payment system. It outlines the problems with the existing payment methods, echoing what we’ve already discussed. It then goes on to state their core principles around payments.

Trust - The CBK does a good job in defining what trust means “While trust may be a subjective concept, in the context of the payments system, it is about certainty and reliability of payment systems and channels. In short, a payer having the assurance that a payment will promptly and securely reach the intended payee.” With this in mind, the key planks that will govern the Faster Payments System from a trust perspective are;

Adoption of relevant common standards in this case ISO20022 - very critical for commercial payments and payments reconciliation;

Promote integration of digital identity - How they do it will be critical but how Pix in Brazil has done this is through a Digital Identity register. In Nigeria, they’ve done this through the BVN. In India, it’s through Aadhar. Given we lack a truly digital identity register, the Pix approach would be best. You can read about it here.

Customer protection, primarily a standardised complaints handling framework.

Data protection framework tailored for digital payments;

Customer awareness;

Pricing principles - The primary aim will be to ensure that tariffs and pricing policies and practices are underpinned by principles such as transparency, disclosure, cost effectiveness and customer-centricity;

Security - The idea behind security in payments is the ability to safeguard all players in the payments ecosystem from fraud and cyber risk. The key planks underpinning security will be;

Adoption of Common Security Standards;

Robust Data Reporting and Analytics;

Capacity Building for Complaints Resolution;

Usefulness - Again, CBK does a great job at explaining what this means. “A payments system can only contribute with a wider economic and social development, if customers find it relevant and applicable to their day to day payments needs. While being a subjective concept, usefulness is taken to mean that the payments needs of users are reliably met in a cost-effective manner.” The core planks under usefulness are;

Promote full-scale interoperability that is embedded into the system through open APIs and not bi-lateral agreements like currently exist;

Facilitate efficient clearing infrastructure that is important for interoperability. How this will work is through KEPSS which currently is only accessible to banks;

Promote standard customer experience standards in CBK’s words "This will include standards, principles and procedures on payments such as QR code payments, NFC payments, mobile push payments, domestic card payments and cardless withdrawals.” In essence make the customer journey standardised making it easier for users to not only learn but operate multiple apps;

Drive more governments payments into digital channels;

Choice - “A key feature of a competitive market is availability of viable payments options. These options need to be priced at the appropriate point that meets the needs of customers and encourages uptake.” This is a direct dig at M-Pesa’s dominance of digital lower value payments. What this means from a strategic perspective is;

Facilitate the emergence of a competitive ecosystem. We’ve seen UPI in India governing how much market share an entity can have in the UPI system;

Executing standard pricing principles - I think this is a coded way of imposing pricing e.g. transactions below x should cost y or the maximum commission per transaction should never exceed x% of the transaction;

Creating standard APIs for the payment system enabling not only interoperability but true innovation on top of the payments system;

Promoting market entry - Critically, CBK will say that they will actively encourage players to enter into the payments system. This is what happened when India launched UPI with players like Meta and Google launching their own payment propositions;

Innovation - This was a critical part of the 2022 strategy and CBK outlined what the governor of the Bank of England referred to as their role in payments. CBK explicitly said “For Kenya to enhance its global leadership in digital payments, CBK will continue to facilitate uptake in new payment solutions anchored on the Strategy principles, and more importantly, based on the degree to which the proposed innovation meets customer needs in an efficient and affordable manner (people-centredness). It’s key planks were;

Promoting APIs;

Creating regulatory support for innovation;

Facilitating digital government payments;

To influence global standards for payments and always learn from current global outcomes.

The new Faster Payments System will therefore look like what Pix have in Brazil or what UPI have in India. It will be national open infrastructure that every ecosystem player can plug in to. The key design considerations should revolve around 6 core issues;

Mandatory Participation - Like Pix and UPI, the Central Bank should drive mandatory onboarding for all banks and PSPs i.e. everyone that is licensed as a bank or a PSP should immediately onboard all their customers onto the system once its live;

Participants - It’s clear that CBK intends both banks and Fintechs to participate in the new system. Moreover, one of their core principles is to promote market entry. It would be very important if the CBK allows even PSPs to maintain settlement accounts with CBK just like Pix in Brazil;

Pricing - P2P pricing should either be free of super low cost e.g. 0.1% per transaction;

Identity - The Central Bank should build and maintain their own identity infrastructure. The best way to do this is through an internal identity register where users can create aliases, hashtags that are mapped to a primary account or wallet. For instance, I can register my number or email and map it to my bank account. I’d then create an alias like my PS5 username “Samkiki” (don’t ask), and have this as my digital identity. If a customer wants to send money to me, they’d just enter Samkiki and the money would come to my bank account;

API - The system should be built on secure and open APIs that enable seamless integrations and innovation;

Product Roll-Out - One of the challenges with MoMo is the limited product function. For instance, direct debits and standing orders are not easy to implement with the latter only being recently launched by M-Pesa. The Central Bank’s payment system should intuitively support direct debits, subscriptions, standing orders, scheduled pull-payments and other types of payments;

Post-Mortem

If well implemented, then Faster Payments should drive not only innovation but significant investment into Kenya’s Fintech industry with players eyeing the revenue pools that would come from the new payments ecosystem. Nonetheless, if poorly implemented then it won’t live up to its promise. To understand what this looks like, Charlie Munger’s refrain of “All I Want To Know Is Where I'm Going To Die So I'll Never Go There” is the best way to approach failure. Inversion is critical to understanding. Therefore we won’t ask how it will fail, we’ll carry out a post-mortem. If the Faster Payments System doesn’t fulfil its promise, this is what I will write in 5 years time;

One of the challenges with Faster Payments in Kenya was the onerous onboarding system. CBK insisted on in-person registration for users of Faster Payments, this led to a situation where customers had apathy given that M-Pesa was already working perfectly for them;

Another challenge was that CBK appointed a few settlement banks to settle transactions. This led to situations where those settlement banks prioritised their own payments therefore leaving some Fintechs out in the cold. It would have been better if CBK allowed PSPs such as M-Pesa, Cellulant and Paystack open their own settlement accounts therefore having more control over reliability;

CBK didn’t make it mandatory for participants to use Faster Payments. Large Banks and PSPs therefore preferred to not onboard customers preferring them to use their own proprietary rails. This delayed adoption leading to general apathy towards the system;

CBK insisted on a very rigid monitoring framework when it came to transaction sizes. Best practice would have been to allow participants to set their own limits based on their internal KYC, fraud and risk data. Nonetheless, CBK insisted on transaction limits of only KES 70,000 (US$ 540) per client per day;

Whereas the system is working ok, some issues have held back the virality and widespread adoption of Faster Payments. CBK decided not to remunerate the settlement accounts for all the settlement participants i.e. banks and PSPs. This led to large banks having significant opportunity cost of holding so much cash with CBK. Banks have therefore limited how much they keep in their settlement accounts thus leading to failed transactions;

These are the issues that would in my view prevent Faster Payments from truly taking off in Kenya. This requires leadership and first principles thinking by the Central Bank and I’ve written about this before. The design choices will be presented by both the bank and Mobile Money lobby as well considered proposals. For instance, the lobbies could argue “Given the high rate of fraud, we think it’s important that we onboard clients manually, each customer should come to a branch due to AML. This is critical to avoid grey listing by FATF”. This is pure BS and should be ignored by CBK.

Implications

What then would be the general implications of this System across the industry? I’ll give an overview of what will be possible then look at the implications for banks, Fintechs and M-Pesa. Sometime back Satya Nadella was talking about Microsoft’s collaboration with OpenAI and how this will impact the industry. Speaking about Google, he said “At the end of the day, [Google is] the 800-pound gorilla in this, I hope that, with our innovation, they will definitely want to come out and show that they can dance. And I want people to know that we made them dance.” This is a useful framing of the overall implications.

In terms of General capabilities, what is happening in India and Brazil is a useful barometer of what will happen with a Faster Payments System.

The P2P market will open up given interoperability and common rails, this will enable a new breed of payments companies targeting the P2P market outside of M-Pesa;

Richer merchant propositions will come up that embed more useful payments data. I expect merchant payments to be the biggest beneficiary and most of the innovation to happen here;

There might finally be a viable alternative to M-Pesa in terms of retail payments. Remember the 800 pound gorilla dancing;

For Banks;

If Faster Payments are cheaper and as reliable than M-Pesa, then I expect Remittance providers to prefer settling through the FPS. This will necessitate banks to build relationships with remittance providers and in my view there’s room for a bank to focus on building reliable APIs and connectors into FPS for the sole purpose of managing remittance business. This is an FX play. In the past, there have been bilateral agreements between MoMo and Banks to control the remittance market. If I were a UBA, GT Bank or SBM i.e. Tier 3, I’d build world class infrastructure and FX capabilities just to serve the Faster Payments market. DTB already has a head start with their Alpha program;

Liquidity - If wallet providers licensed as e-money issuers come to take significant market share in the P2P or even C2B space, then I expect that new trust account business will emerge. What this means is that those wallet deposits will be held in one trust account at a bank. This could have implications for overall liquidity, moving away from larger banks with a wide branch network to banks that bank wallet providers;

Race to acquire Merchants - If identity is built in through the CBK system - then it will be critical to acquire merchants and small businesses so that their payments settle with you. Transaction teams should keep an eye on this. The idea is to race and acquire merchants on the digital identity register that CBK sets up as that will affect where a merchant’s payments are settled. You snooze you lose;

If costs are low on the FPS, then it’s likely that we should see an explosion of merchant payments and even P2P payments insofar as the constraint to merchant collections growth is the cost of being paid on M-Pesa. This is likely the case. I remember a story during Covid when the CBK mandated that payments below KES 1,000 be free, some people would split a KES 60,000 payment into 60 different KES 1,000 payments. This is what drove I&M bank to make bank to M-Pesa transfers to be completely free. With a cheaper payments system, then we may see lower cash usage and this will impact bank branch business. This will have to be optimised;

Overall, the beneficiaries of FPS will be banks that have strong digital propositions such as I&M and Standard Chartered. Moreover, apps like Loop that have built go-to market motions independent of the core bank should also do well.

Banks should look to build strong payment propositions and the recent partnership between Network International Alipay + Payments Tech should benefit from this. Wallets are more intuitive than bank accounts for P2P;

For Fintechs;

The challenge with Mobile Money is that you have to share your number with someone for them to pay you. I suspect this is why a number of pretty waitresses are tipped, the underlying reason is that the person tipping wants their number. With an FPS that has embedded identity, Fintechs will be able to build unique P2P payment propositions that are built on aliases and markers such as hashtags, this explains the virality of apps like CashApp. Creators can just be sharing their aliases on their socials and not their numbers;

If Faster Payments is built on ISO 20022 then there will be an opportunity for PSPs to build rich merchant payment capabilities. For instance, a restaurant like Artcaffe can link invoices and specific products to payment instructions therefore having better visibility on their sales. This can even lead to more useful customer engagement systems such as loyalty points. This is both an infrastructure and front-end play. Companies like Pesapal, Flutterwave, Kopo Kopo and even Craft Silicon should keep a close eye on this;

Open payments infrastructure should open up the agent market to new players. Agent markets are the cash-in cash-out networks that enable people to deposit and withdraw hard cash from the system. Currently, this is dominated by M-Pesa. At the end of the day, agent payment operations are simple fund transfers. There’s an opportunity to build an interoperable agent system that enables a customer to deposit and withdraw to any wallet independent of the wallet provider. This opportunity can be taken by players like Tanda or existing banks that have agent networks. In Nigeria, you have multiple agent network providers and we could see the same. Ultimately, they will all consolidate around two to three reliable players;

The Remittance market will be up for grabs so long as PSPs can maintain settlement accounts be it with banks or directly at CBK. This will therefore mean that a Nala or Sendwave will directly work with a Cellulant for Remittances rather than having to partner with a bank. Through this, a Verto or other FX provider can step in and therefore create a tripartite agreement for remittance settlements obviating the need for banks. The idea would be cheaper FX and cheaper fees;

The consumer market is up for grabs with the following use-cases being up for grabs;

Enabling subscriptions particularly for Telegram, Facebook, Instagram, X or Instagram creators. I think we are moving firmly into a creator economy and we need the rails for this;

Build a cultural brand around certain demographics - the Gen-Z market will need a payments app that’s reflective of the culture;

Embedding payments into vertical SaaS through companies like Zoho;

Stablecoin integration for gig-workers;

To do this will require serious technical chops, funding and commercial focus. This is where I see a Google, Meta, Wave or larger player like O-Pay coming into the market. It will need time, skill and funding.

There’s an opportunity in Infrastructure player, particularly abstracting the complexity of the entire FPS into a simple API that will enable people to get running from day one. I see Craft Silicon being a key player here.

What it means for M-Pesa;

M-Pesa won’t struggle and in fact could even thrive so long as management sees the opportunity as opposed to dwelling on what has changed. The best way to look at this is in two ways, what works for M-Pesa and threats to M-Pesa;

What works for M-Pesa

M-Pesa is a licensed PSP with a massive user base, world class infrastructure and skilled staff. All the ingredients needed to take advantage of FPS. Here are some ways that M-Pesa can be even larger and more profitable;

Neutral payments infrastructure can enable their already massive agent network to become a collection network for all banks in the country. How this would work is that customers can now deposit not only to their M-Pesa wallets but any wallet or account linked to the FPS. They can charge a small commission for this and therefore kill branch based banking for small amounts;

This requires open banking but assuming that we have both open banking and FPS, then M-Pesa can become the central hub through which customers manage all their accounts given the ability to move money between wallets easily and check balances. The customer interface layer may be aggregated through M-Pesa giving them enormous economic value;

M-Pesa still dominates USSD and STK through which the bulk of customer interactions take place given low smartphone penetration in the market. This should remain a useful moat for the company;

Threats to M-Pesa

There are some businesses that will be impacted;

A cheaper merchant collection method coupled with richer payments messaging will be a much better proposition than Lipa na M-Pesa. This will negatively affect their business propositions which are their fastest growing;

Similarly on business, remittance providers will prefer settling on cheaper infrastructure affecting their C2B business. Similar dynamics will work across verticals such as sports betting, merchant payouts and other C2B categories;

There will be margin compression across their entire product stack given a viable alternative that is potentially as reliable and ubiquitous;

If being on M-Pesa is no longer a matter of life and death for individuals and there are viable alternatives, I expect to see an up-tick in M-Pesa defaults. The cost of being kicked out of M-Pesa will no longer be significant and thus the incentive to repay will dwindle;

Ultimately, Vodacom in Tanzania makes a 6% net profit margin and MTN’s margins in Uganda are nothing compared to Safaricom in Kenya. If M-Pesa is the jewel in Safaricom’s crown given the fact that Voice and SMS are declining and data is being threatened by Starlink, then the overall outlook for Safaricom’s stock doesn’t look too rosy. Even if M-Pesa continues to be the main player in terms of market share, their margins will be compressed leading to a less than stellar business. This is actually the case across the continent. Mobile Money is not a great business if you don’t have dominance.

All this though is contingent on whether Faster Payments is implemented properly.

Wrapping it Up

Faster Payments has the potential to transform Kenya’s Fintech industry. We’ve seen that markets with Faster Payments such as Brazil, India, Nigeria, Singapore and the United Kingdom are all major Fintech hubs in their respective regions. Nonetheless despite this, we’ve seen different rates of ubiquity, Pix is almost 3x of Brazil’s GDP in terms of its annual payments volume whereas Nibss in Nigeria is less than 90%. The differences in my view are the different design choices for instance BVN vs Pix’ ID system. The devil will be in the details and CBK will need to show true leadership.

That's an easy problem to solve. It's an infrastructure problem and the solution is widely available.

They work hand in hand, Open Finance and Faster Payments are two peas in the same pod? They are complimentary products.