#38 - Adventures in De-Fi Land

Actually participating in De-Fi to get a better feel of it

Hi all - This is the 38th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. 🚀

Introduction

I’ve had attempts at covering the crypto world. The first one talked more about the opportunity behind cryptocurrency particularly in Africa. There were two main ideas, the first that value is an idea driven by consensus. The second; that financial exclusion has serious ramifications in Africa and that dual exchange rate systems in Nigeria and places like Zimbabwe deny genuine people the opportunity to make a living. This drives bad outcomes such as crime and in worse cases militancy and armed rebellion.

The second attempt was me trying to ideate about what De-Fi can solve for in the global south particularly Africa. This was less elegant and in retrospect not very useful. To talk about De-Fi and Crypto, you actually have to get into the space and enter the world of Decentralised Finance. You can’t usefully speak about something that you have no experience in. This is the basis of today’s article where I actually get into De-Fi and play around the space so that I can have a proper view.

My interest in this space stems from my experience in Burundi as well as parts of Eastern Congo. These areas are largely excluded from the global financial system and the ramifications are there for all to see. I remember back when Libra was announced by Facebook, my face lit up with excitement because I saw the promise of what a “Libra” can do for the large mass of people excluded from the global financial system due to reasons that exist outside of their control. My idea at the time was that Libra would enable two critical things. Libra would enable people to trade through enabling settlement finality as well as stable pricing via a stable currency. Additionally, Libra would enable people to maintain a store of value through their Libra wallets.

Eventually this project didn’t see the light of day and in my view, future global stablecoin based projects will also suffer the same fate largely due to macroeconomic considerations in markets such as Europe and the United States.

I have a friend who works as a gym instructor in Bujumbura. His name is Joseph and he is one of the most intelligent and hard working people I know. He is fluent in multiple languages such as French, Kirundi, English, Swahili and a bit of Spanish. Joseph makes his income both as a boxing instructor with the distinction of one of his students recently qualifying for the Tokyo Olympics as well as an online French tutor. The internet enables him to tutor French to students from across the world with the benefit being that he can offer competitive rates. Most of these students are referral based and thus his business model lacks the scalability and discovery that comes from a centralised platform such as Upwork and Fiverr.

For a long time, Joseph sent his students my Paypal address for payments. They’d send money to my Paypal and I’d convert it into M-Pesa and thereafter give him the equivalent in local currency. Clearly this process was clunky and didn’t make sense. Joseph needed both a way to earn on platforms such as Upwork and Fiverr so as to increase his revenue as well as own a global store of value wallet that would enable him to receive payments. I finally convinced Joseph to open an Upwork account. This was easy. Next, we needed a Visa Card so that he can link it to Paypal. This is where the problems began. Everything we tried simply couldn’t work because he had a Burundian ID and IP address. He was dejected after all these attempts and I was sad because I had given him hope, false hope in retrospect.

The question for me remains, why can’t someone like Joseph have an opportunity to earn? Josephs exist across the continent due to a global financial system that wantonly discriminates against whole swaths of the population through measures such as sanctions lists and decrees. Honest people in Nigeria lack access to the global financial system because Nigeria is “high risk”. A whole population suffers because of the actions of a tiny minority who despite the limitations, will still have access to the same financial system that’s trying to punish them.

As the world digitises, access to globally relevant financial primitives will be critical for the youth of the “global south”. This is a moment in time where internet enabled search and discovery will give Africans real opportunities. Think of digital art for instance, internet enabled search and discovery will enable an African’s art to reach as many people as possible. This then increases the value of this art. This can only be useful if the African in question has access to a financial system that enables him to make and receive payments globally. This is the crux of my never ending interest in Crypto-currency and Decentralised Finance and why the Libra project got me off my seat. For many people in the West and in countries such as Kenya and South Africa, the idea of full exclusion does not really resonate given that traditional finance works well for these countries. For many other people, it’s a nightmare.

Samora’s Adventures in Cryptoland

I wanted to do four core tasks and additionally, I wanted as little help as possible. The main idea is that the bulk of the users of any platform are “Laymen”. For De-Fi to be useful it has to be accessible to the layman. The four main tasks I wanted to achieve are;

Open a store of value wallet;

Move money (Send/Receive);

Save Money;

Borrow Money;

Opening a Wallet;

To start with, I opened an account with Binance. Binance is a global cryptocurrency exchange which enables people to buy and sell cryptocurrencies from the comfort of their phone. In Africa, Binance is largely used as a peer to peer cryptocurrency exchange given that most Central Banks in Africa have banned crypto. The process is quite simple;

Download the Binance App from either the Google Playstore or IoS. Alternatively, it’s accessible as a web page.

Register to open a Binance wallet. The information required in this case is;

Your country of residence - confirmed usually via your IP address;

Your email address and a password of your choice;

Finally, to be a verified account, you have to go through an onboarding process that involves a selfie and a picture of your passport or ID. This is powered by Refinitiv;

Interestingly, for a number of countries such as Burundi and D.R.C, restrictions still apply. However, I understand there are ways to get across this although they require technical savvy.

In addition to my Binance wallet, I needed to get a wallet that would enable me to participate in the De-Fi world. Metamask enables you to connect your “money” to Decentralised Apps or DApps such as Uniswap, Opensea, Maker and Sushiswap. I decided to get a Metamask wallet although there are alternatives such as Hyperledger, Trust Wallet and Exodus. Metamask was the easiest. The Set-Up was easy;

Go on to the Metamask webpage and download the browser extension. I used the Chrome Browser Extension;

Create a wallet - At this stage, you’re asked for a password;

Thereafter you receive a secret phrase which is a phrase made up of randomly generated words. This is critical to securing your wallet. You should store this phrase safely. Some people write it down on a piece of paper and then proceed to store that piece of paper in a safe deposit box. I find this extremely ironic though. The whole point is decentralisation, it’s ironic that you trust a central authority to keep your money safe;

Moving Money;

Once my wallets were set-up, I needed to get about actually moving money around the crypto world. First I needed to get money into the system. Given that I was looking at this from an African perspective, the amounts involved needed to be realistic. The whole idea was for accessibility and cost that would make sense to someone in the “global south”. I decided I would spend a maximum of US$ 100. First, I’d buy Ethereum and then convert Ethereum into a stablecoin such as USDC which would be my store of value in the De-Fi world.

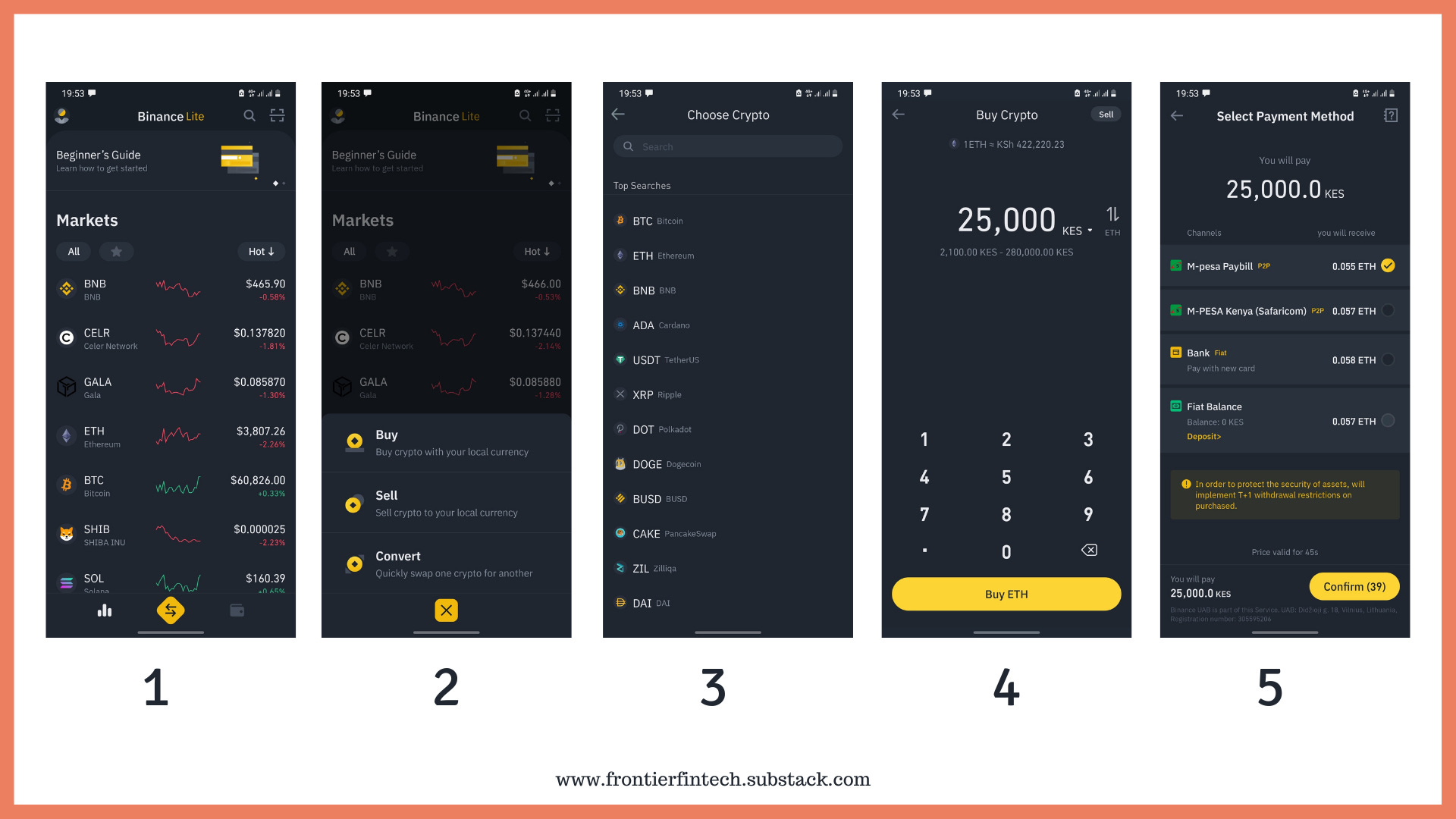

The Ethereum buying process was as follows;

Select the Buy Crypto icon;

Select the specific cryptocurrency you want to purchase;

Enter the amount you want to spend, in this case KES;

Select the option you want to use for settlement. In Kenya, this is primarily M-Pesa based as well as bank account transfer;

Binance then connected me to a seller and mediated over the transaction enforcing penalties for non-settlement. For instance, if I didn’t send the money, my account would be suspended and similar enforcement would happen for the seller.

The diagram below represents the flow.

To note, Binance didn’t enable me to buy USDC with Fiat. I was offered the opportunity to buy USDT (Tether) and then convert into USDC. In retrospect I should have taken this option. I was influenced by the fact that Tether was undergoing scrutiny over claims that it misled investors that it had liquid assets to fully back the currency. It was later fined US$ 41 million by the US Commodity Futures Trading Commission for making misleading claims. This is one of the issues around crypto. There’s a lot of rogue activity that makes it hard for laymen to fully trust the space.

What stood out is that after paying KES 10,000, I ended up with roughly 0.025 ETH which at the time was valued at roughly 86 dollars. There were roughly US$ 2 dollars of fees on that initial transaction.

I then moved my ETH to my Metamask wallet. I did this by copying my metamask wallet address to the Binance withdrawal functionality. I ended up withdrawing ETH 0.0195 with the transaction passing through the ERC20 network. This cost me 0.0035 ETH or roughly US$ 12 dollars. The costs were starting to pile up but I soldiered on for the sake of science. It was already dawning on me that nobody in the “global south” would accept a US$ 12 charge for moving the equivalent of US$ 70 dollars across platforms.

My Metamask wallet now had 68 dollars and my Ethereum wallet had around US$ 7 with this amount being influenced by the increase in the ETH price that happened during the course of the week.

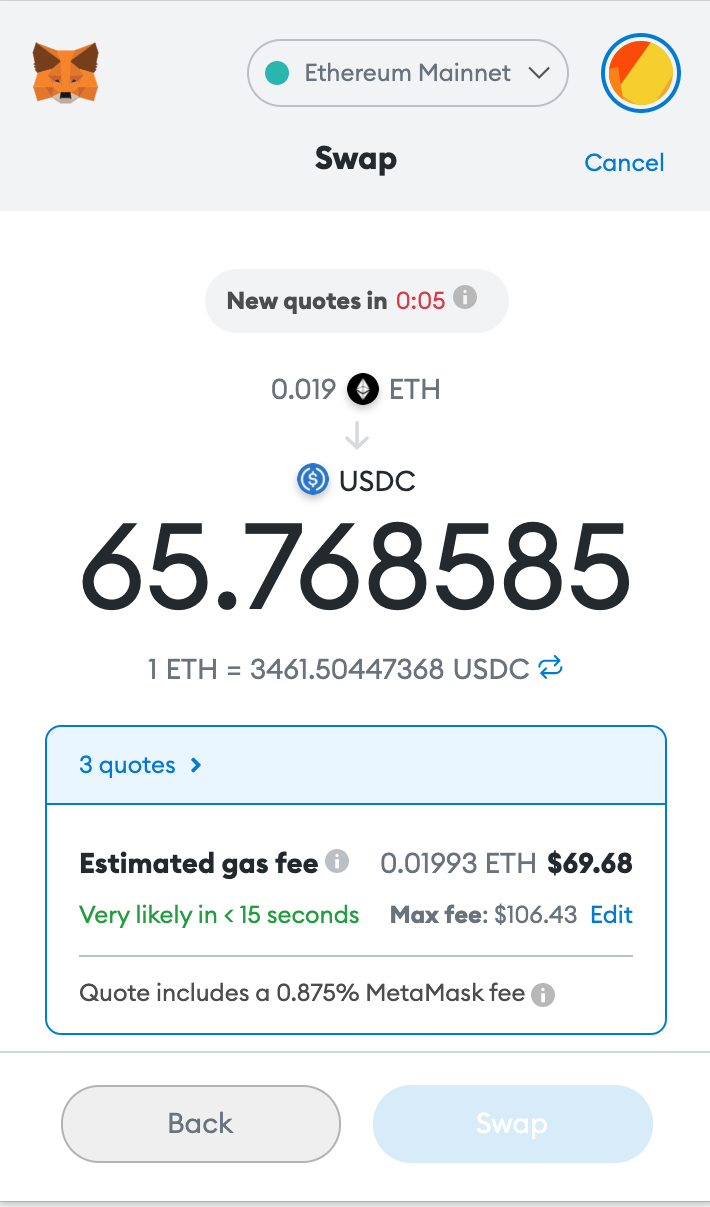

The next thing for me to do was to get USDC via swapping it for ETH on Metamask. I’m sure there are cheaper ways of doing this, but I had to approach it as a layman and not a technically gifted crypto-bro.

The above page appeared on my Metamask extension. To convert my 0.019 ETH into USDC, it would cost me a similar amount in gas fees. Total gas fees would be almost US$ 70. This unfortunately is where my Metamask journey ended. There was no point in moving on. As someone in Kenya, why would I pay so much in fees to move money around the internet when I had access to similar services. For an excluded person like Joseph, what would be the point of participating in a system where the bulk of your revenue would be eaten up by gas fees?

One thing that became clear is that Crypto in Africa is being driven by other factors rather than financial inclusion. Back in 2017, Vitalik Buterin, the founder of Ethereum tweeted the following after the cryptocoin market cap hit US$ 500 billion. It’s a very interesting thread that probably still rings true.

Despite it’s useful functionality. The space is yet to offer useful everyday banking solutions for the unbanked. Most Africans seem to be using De-Fi for the following reasons;

In Kenya where there’s a mature forex market, De-Fi is being used mostly for yield farming, trading and as an investment tool;

In Nigeria, in addition to the factors driving usage in Kenya, many users there are also using it as a store of value given the depreciation of the Naira. Additionally, it’s offering many people a payment option given the second order effects of the currency problem is the difficulty in making and receiving payments through traditional channels;

Enter Celo

I then moved my money back to the Fiat world. First, I moved the money from Metamask to Binance and then moved it to Fiat via the P2P functionality. Luckily, between the time I bought ETH to the time I was selling it, the price had gone up by 14% and I thus booked some of these capital gains.

I asked around the crypto space particularly on Twitter about low cost alternatives to Ethereum and I was introduced to Celo. Celo is a cryptocurrency that runs on the Celo blockchain and is accessible via the Valora wallet. It has many similarities to Ethereum including the fact that it will enable Decentralised Apps on its platform. Additionally, it runs on a proof of stake framework where each validator node needs at least 10,000 CELO to vote on changes. This blog gives a good overview of Celo.

Celo has attracted global investors such as a16z and Social Capital given that it’s designed to be the financial infrastructure for global payments. It’s a super low cost network where the cost of transfers is significantly lower than other platforms such as M-Pesa, RTGS, SWIFT and of course Ethereum or Blockchain.

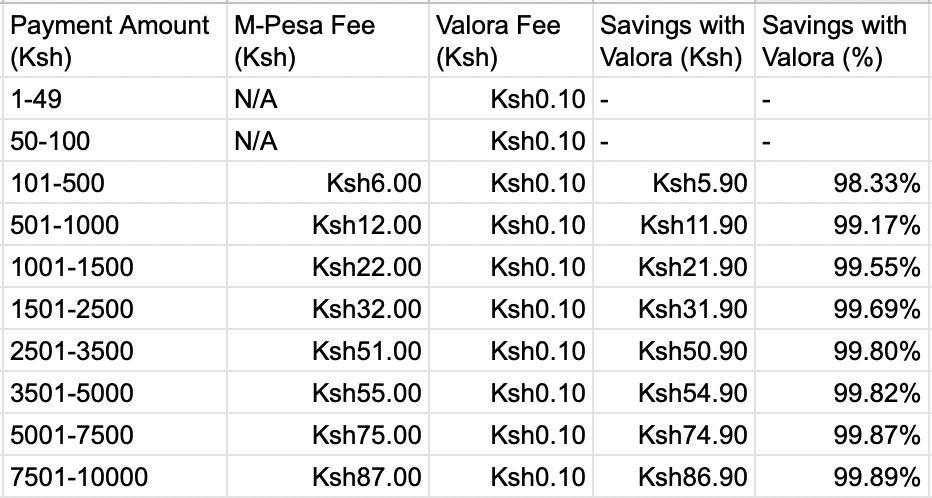

To access Celo, one needs to download the Valora wallet with the onboarding process slightly similar to that on Metamask. You will need a phone number or email address as well as a password and secret phrase. My good internet Buddy Charles Nichols helped me through the process and created this interesting table that compares the costs of Celo to those of M-Pesa.

Source: Charles Nichols

Once my wallet was up and ready, Charles set me up with my first receipt of 5 dollars. I however wanted to load my wallet by myself. The only way to add funds on the Valora wallet is through a bank transfer, Debit Card, Cryptocurrency Exchange or via M-Pesa through Kotani Pay.

The Debit Card and Bank option work through either Ramp or Moonpay (both Crypto payments infrastructure providers). Both these options don’t support the Kenyan market. Kotani Pay apparently works well for withdrawals but not deposits into Celo. I was then left with the option of P2P but in this case, there was no mediation. I just had to trust that my counterparty came through. I managed to get someone called Brian who was introduced to me by Michael Kimani known on Twitter as Pesa Africa. Michael in my view is one of the foremost thinkers on African Crypto and Fintech. If you’re really keen on understanding the space, Michael is the go to guy.

Eventually I received Celo Euros cEUR 51.66 or the equivalent of KES 6648.77. I converted this into actual Celo and eventually held 10.45 Celo which is the equivalent of KES 7,400. I also benefited from an increase in the Celo price during the week. I made a payment of KES 1,000 to my wife and indeed it only cost me like 10 cents. With Celo, I could send and receive money to and from anyone in the world.

By converting my Celo to Celo USD (cUSD), I could benefit from a 50% APY savings wallet on Celo. I could also map my Celo wallet to Ubeswap from where I could participate in the De-Fi world by yield farming, participating in liquidity pools and swapping cryptos. Lending activities were limited on the Ubeswap platform. However, given that I’m in this system now, I will continue to explore the space. I will dedicate the next blog to saving and borrowing.

Main Thoughts and Outtakes;

The biggest issue with De-Fi and crypto in Africa is on and off-ramps and this is largely a regulatory issue. Cryptos such as Celo offer multi-currency stablecoins but on/off ramps is a problem. If the on/off ramp issue is fixed, then P2P payment platforms such as Mobile Money could face formidable competition;

It’s quite clear that stablecoins can solve global money movement very easily. The issue comes around the currency impact in African markets. By allowing a stablecoin such as cUSD or USDC, a Central Bank is allowing dollarisation in that market. No Central Bank will entertain a dual currency system in the local payments market and dollarisation will likely come at the cost of a weakened local currency. I don’t see any Central Bank in the near term allowing this to happen. Stablecoins should perhaps be priced in local currency such as say cKES or cNGN. However, what then becomes the difference between such a stablecoin and either a CBDC such as eNaira or the money in your M-Pesa wallet? The only difference would be cost and programmability but global money movement wouldn’t be solved. The money in your mobile money wallet is a stablecoin!

Given that onboarding, ease of use and cost are the key blockers to mass adoption of crypto in the “Global South”, organisations such as the Celo Foundation with Celo and Emerging Impact with their Umoja product should be keenly watched. Umoja has so far the most compelling use case that would soften a Regulator’s stance and that is a donor/humanitarian angle for cash disbursements. I’ve participated in cash disbursements and an Umoja like product would be a game changer in terms of cost and transparency;

The De-Fi world is functionally superior to traditional finance. The idea behind Metamask where you just link your wallet to any Decentralised App is super intuitive. In fact, this is the idea behind Open Banking and platforms such as Plaid. In addition to the superior functionality, the fact that most of De-Fi is open source means that any useful functionality needs to be built only once and then this is available to all the participants.

Given this superior functionality as well as the difficult on/off ramps, the idea of the De-Fi mullet becomes interesting. What this means is that the back-end i.e. payment rails and functionality will remain De-Fi while the front-end will be centralised via Fintechs. This is already happening via apps such as Robinhood and arguably Coinbase and Stripe’s recent announcement adds credence to this point. This is well articulated by Simon Taylor on Fintech Brain Food. My idea is decentralised agency banking operations in Africa for De-Fi;

The future of global e-commerce and trade becomes very interesting in a De-Fi world. Imagine wanting to buy something from across the world and paying via De-Fi. Smart contracts and this programmability would enable you to define payment terms that include escrow prior to negotiation, 10% upon sale agreement, 50% upon shipping and 40% upon arrival. The opportunities are vast and only limited by imagination;

The Fintech Mullet argument lends itself to a situation where every bank should have a crypto/De-Fi strategy because it’s an innovation that can fundamentally change the way people bank;

When speaking to Crypto bros, the talk is always around how crypto is permissionless and enables them to build outside of government regulation and interference. The question always is whether Crypto is promising as a significant technological advancement or because of its existence outside of government purview? My thoughts around this are quite clear. Governments aren’t going anywhere and if people want to change things, they have to do the dirty work of controlling the government and thus making changes. All of the biggest changes over the last 100 years to our systems of global governance have been based on post-conflict conferences where a bunch of folks (traditionally men) sit down and agree how things will be done. From the Berlin Conference to the Yalta Conference to Bretton Woods.

For De-Fi to become mainstream it needs approval by the government. If it’s not in the general interest of the government, then it will not become mainstream. Crypto bros will just have to do the hard ugly work of lobbying and influencing. That said, the technology behind De-Fi is super impressive and can usher in significant improvements to the outcomes generated by today’s global financial system. I’m particularly keen on the impact of Trade Finance.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@frontierfintech.io or samora.kariuki@gmail.com

I love this

This is very detailed, thank you. As someone who is still very new into this space, De-fi, while interesting, still has a whole lot of concepts that I'm still trying to figure out. I am grateful though that you're writing from an African perspective as while everyone talks about why decentralized finance is great, few talk about how practical its applicability is for the average African and your post explains this. So thank you.

Meanwhile, I am really looking to get more into this space but I'm not even sure where to begin. Defi is the future no doubt but how does a writer like me get to acquire as much knowledge as you in this field and what possible opportunities are available? Would love to hear from you. Cheers!