#25 Buy Now Pay Later

Breaking down the BNPL Business and how it could succeed in Africa

Hi all - This is the 25th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. 🚀

Introduction

This week I cover the Buy Now Pay Later business analysing the commercial model behind the likes of Klarna and Affirm whilst discussing how the model could be applied to Africa.

The Buy Now Pay Later (BNPL) model has exploded in the past 24 months with significant moments marking its growth. These include, the recent fund raise by Klarna, that valued the firm at US$ 46 billion as well as Affirm’s IPO that had an implied valuation of US$ 12 billion. Recently, Goldman and Apple partnered to launch a BNPL feature on Apple Pay that’s being referred to as Apple Pay Later. Usually, Goldman Sachs and Apple don’t get into a business if they don’t think it’s lucrative. Clearly, BNPL has significant potential. The idea this week is to analyse the business and see what factors need to be present for it to succeed. As always, ideas around how BNPL can work in Africa are discussed.

What is BNPL

The term Buy Now Pay Later seems pretty self-explanatory. The idea behind BNPL is that consumers can at the point of purchase split the payments for an associated purchase into smaller, more “affordable” instalments. The idea is as ancient as civilisation as humans have always split purchases often through informal agreements. In the West, the concept of “lay away” used to exist where you’d buy something at a store by paying small instalments, once you finished paying, you would then pick up the item. In Africa, most BNPL agreements are informal arrangements driven on trust between the buyer and seller. People buy many things on BNPL including shoes, electronics, cars and insurance policies on informal agreements. In most African countries, shops are the biggest source of consumer credit. In the 70s and 80s, a number of retail stores used to offer BNPL for durable goods albeit to a very small formal sector minority.

BNPL as we now know it and as we discuss in this article is based on a more formal credit agreement that is designed around digital principles and is seamless. This is often presented as a checkout option at e-commerce sites.

The diagram above represent the checkout flow, a consumer upon selecting specific goods on an e-commerce website can proceed to select a BNPL payment method. This would then be followed by a page showing the breakdown of expected payments with the consumer being prompted to agree or disagree with the terms presented. These credit agreements are defined along a number of parameters;

Charging interest - Most BNPL players don’t charge interest particularly on short-term instalment transactions. They charge the merchant a higher take rate with the promise of lower cart abandonment and higher average order values (AOVs). If the customer pays on time, no interest is levied. Thereafter, late fees and deferred interest can be charged. Players such as Afterpay and Paypal’s Bill me later don’t charge interest on specific payments. Affirm on the other hand charges interest with the interest rate depending on your credit quality;

Credit reporting - BNPL players often don’t pull a credit report and don’t report payments once you’ve paid. These make them popular with thin-file borrowers. Unfortunately, upon missed payments some BNPL players report payments. This can be followed by a demand to clear the full balance and account closure. Some players such as Klarna go further to charge your credit card for the unpaid amount;

The table below shows a breakdown of the different BNPL players in terms of interest charged;

Why BNPL?

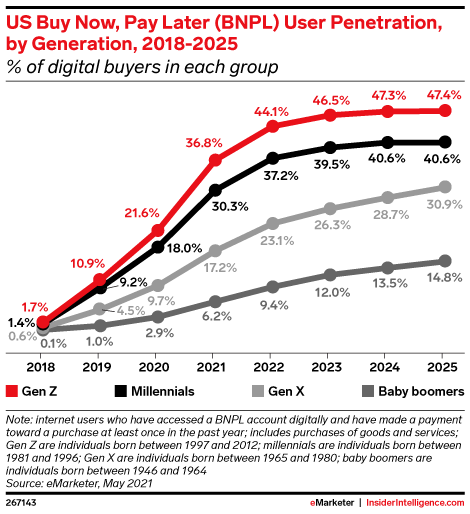

The diagram below from e-marketer.com shows the adoption of BNPL by generation.

It’s clear that the bulk of BNPL adoption is being driven by Gen-Z’s and millenials. The core reasons for the adoption of BNPL this age group are;

Negative perceptions around credit cards - The Global Financial Crisis had a major impact on the perception of credit cards by millennials particularly. Seeing parents struggle due to credit card debt led to lower adoption of credit cards by this generation. I also have a natural aversion to credit cards and use mine almost like a debit card, clearing payments almost instantly. The aversion to cards is driven by opacity and the cost of credit with APR’s in the USA running at around 16%;

Millennials and Gen-Zs have had their financial lives impacted by a number of significant macro events. The Global Financial Crisis, the digital transformation in production and lately the coronavirus. These have had the impact of making millennials more fiscally conservative due to the increasing volatility in their financial and economic lives. BNPL in practice is popular largely due to its transparency and clear repayment schedules enabling younger people to budget. This of course has to be seen in the context of crushing college debt that add to the financial obligations of this generation particularly in the U.S.A.

Additionally, the erratic economic environment has made merchants prefer to accept BNPL as a payment option as it allows customers to pay for goods that they previously wouldn’t have been able to afford. This has been the case with luxury brands such as Saks Fifth Avenue and Calvin Klein which sell particularly through Klarna. Improvements in technology and new business models such as open banking have accelerated the growth in BNPL. Klarna for instance has benefitted from open banking in Europe powering KYC and credit scoring. American players such as Affirm have benefited from partnerships with Plaid that also power onboarding and income verification.

Commercial Considerations

The idea behind BNPL is to make money by offering suitable financial arrangements that allow consumers to make purchases more “affordable” by deferring payments. This is often centred around e-commerce which is predicted to grow to over 22% of global trade by 2022. The diagram below presents the expected growth of retail e-commerce.

Different players have taken different approaches. Klarna for instance has taken a fully integrated approach offering the full gambit from a shopping app by signing up stores, offering delivery and logistics including returns, a debit card for offline payments and of course the BNPL payment option. This is super-charged by a loyalty program that enables customers to benefit from discounts from their favourite shops based on a positive repayment track record. Afterpay has adopted a similar business model.

Source: Klarna Investor Presentation

The idea behind this dynamic seems to be to build a positive marketplace dynamic where more customers attract more retailers/merchants with Klarna benefitting from improved data flows as well as higher gross merchant volume.

Most BNPL players report the following key metrics;

Gross merchandise volume (GMV) - this is basically the value of all merchandise purchased through a company’s BNPL product. This defines both the take rate that will be charged to merchants as well as the interest rate that may be charged to customers. The more the GMV the better. Klarna for instance recorded a GMV of US$ 58 billion in FY 2020, a 46% growth from the year prior. Affirm on the other hand recorded GMV of US$ 4.6 billion in FY 2020 with FY 2021 guidance of US$ 7.2 billion. The bulk of Affirm’s GMV, approximately a third of it, is derived from their partnership with Peloton. Afterpay had reported GMV, in their case reported as “sales” of US$ 11.1 billion;

Number of customers - ideally the more the customers, the more you can drive GMV. Customer acquisition is driven by novel marketing campaigns with Klarna being clear leaders in this regard. Klarna reports 87 million global customers with 18 million monthly active users globally. Affirm has 5.3 million active customers;

Number of merchants onboarded - Klarna is the clear leader with over 250,000 merchants signed up on their platform. The more the merchants, the more the potential customers and naturally increased GMV will follow.

The banking element of raising low cost funds and having low defaults through good origination practices. This then increases your interest income. Different players approach this differently. Afterpay for instance, given that it doesn’t charge interest, accounts for unpaid instalments as receivables and any defaults are accounted for as impairments on receivables. Klarna on the other hand reports credit losses whilst reporting its assets i.e. future receivables, as loans to customers.

In a nutshell, if you can attract more customers to pay through your payment option, accurately assess your clients creditworthiness and originate loans responsibly whilst growing your merchant network, then you have a wonderful business that will profitably ride the growth in e-commerce.

In China, Alipay and Wechat offer their own variants of BNPL that ride on their existing vast networks of merchants, customers, credit data and payments settlement architectures.

Different BNPL Formats

When you break down BNPL into its core principles. Different BNPL models emerge. In principle, the following core elements need to be in place for BNPL to work well;

Customer on-boarding and proper KYC including income and affordability verification;

Ubiquitous payments and settlements architectures;

Credit decisioning and origination capabilities - ideally fully digital;

Merchant relationships both on-line and off-line at checkout;

A source of funds - capital or a balance sheet;

Below is an attempt at a BNPL stack;

Keep reading with a 7-day free trial

Subscribe to Frontier Fintech Newsletter to keep reading this post and get 7 days of free access to the full post archives.