#23 How to Grow SME Access to Finance

How firms should approach SME Access to Finance in Africa - With help from Hilda Moraa of Pezesha

Hi all - This is the 23rd edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. 🚀

The financial system of the past 200 years was designed for the industrial era and served only 20% of the population and organizations. As we enter the digital age, we must better serve the remaining 80%. Together with our like-minded partners, our vision is that consumers and businesses will no longer have to navigate inefficiencies to find capital, but rather, capital will be matched with consumers and businesses based on data-driven predictive technologies, which will enable every consumer and small business in the world to benefit from tailored financial services. - Ant Group Chairman Eric Jing

Summary

The aim of this article is to scope out the SME lending space in Africa. I speak to Hilda Moraa, the founder of Pezesha to discuss the key issues being faced in driving SME Access to Finance. IFC estimates that the SME financing gap is approximately US$ 330 billion. This increases to US$ 5.2 trillion when all developing countries are considered. I review the SME sector in general in terms of key activities, trading relationships and existing financing practices.

My take is that an SME financing stack needs to be built that includes digital ID and KYC with an e-commerce layer whose key function is to enable people to generate and grow revenue. On top of this, payments and origination layers can be built that can enable embedded finance and access to not only credit but other financial products such as insurance and wealth management. An insight into Ant Group is given showing the core factors that need to be present to scale SME finance.

Introduction

The topic of Small and Medium Enterprises and the enablers to their growth is a very critical topic for me and I think it should be for anyone in Fintech, government and finance in general. The rationale underpinning this perspective centres around the expected role SME’s will play in the future as demographics, technology and economic structures all point towards micro-entrepreneurship. At a macro-level, Sapiens by Yuval Noah Harari as well as this podcast where Tim Feriss interviews Naval Ravikant are useful for understanding these shifts.

Ultimately, Sapiens traces the development of society from hunter gathering to the agricultural revolution and finally to the industrial revolution. All through these epochs, society has been shaped by the latest technological advances from fire to the steam engine. Through these shifts, economic design has also morphed from hunter gathering and barter to surpluses and trade brought about by the Agricultural revolution. The industrial revolution brought about concepts such as economies of scale, the theory of the firm and mass production. Industrial design thus rewarded the largest firms which were run efficiently.

The fourth industrial revolution thus portends a trend towards micro-entrepreneurship as technology eliminates barriers such as information access, market access and potentially financial access that necessitated large firms. One can read up on Coase’s Theorem of the firm. The idea was that large firms are necessitated by transaction costs. If transaction costs reduce because of technology then it’s clear that the playing field shifts towards smaller nimble niche firms.

How then should we use technology to scale access to finance for SME’s and drive this shift particularly in Africa.

To learn more about the SME lending space, I reached out to a good friend; Hilda Moraa, who is the founder of Pezesha and one to watch in the African Fintech space.

Scoping the SME Space in Africa

The definition of an SME is a nebulous shape-shifting concept. In most cases, a standard definition can’t be taken because this is directly correlated to the size of the market in which they’re operating. Nonetheless, they can be defined based on standard parameters such as the number of staff, their annual turnover and the degree of informality with this lying within a spectrum that considers elements such as their accounting processes, corporate governance and financial savvy. In terms of economic activity, SME’s engage in all forms of economic activity from service to trade to manufacturing.

In terms of impact, most estimates point at 90% of all businesses being SME’s in Africa contributing to over 60% of employment and 40% of GDP. In countries such as Nigeria and Kenya, over 80% of total employment is in the informal sector showing a bigger contribution towards job creation by SMEs.

In most surveys done of SME’s, access to finance is often categorised as the biggest issue facing SME’s. World Bank estimates put the SME funding gap at US$ 330 billion annually. Globally the SME funding gap in developing countries is estimated at US$ 5.2 trillion which corresponds to 20% of the GDP of the scoped countries. Of these figures, the biggest constraint financially is access to working capital.

Global SME Funding Gap

Source: International Finance Corporation

The nature of SME’s in Africa is diverse and complex. A significant chunk of SME’s operate within the informal trade sector. These are kiosks and shops that sell a variety of goods at small physical stores. Usually, these shops act as the customer facing leg of larger supply chains that trace back to multinational companies operating in industries such as beverages, breweries, FMCG and tobacco. The supply chains are run on old distributor frameworks in most cases where each distributor has territories and route to market plans governed by the producer/supplier. Financing in most cases is governed on credit terms which at times are loosely defined and managed on a relational basis.

Within the service space, most SME’s operate barbers, hairdressers, tailors, plumbing and electrical firms as well as various other professional service firms. These tend to operate on word of mouth advertising and in some cases loose credit terms to preferred clients. Manufacturing is another key industry. In Kenya it’s referred to as the “Jua Kali” sector (Jua Kali refers to the fact that they’re working under the hot sun). Manufacturing is mostly focused around locally used goods such as furniture, low value equipment and items such as curios, jewellery and similar items. In most of these businesses, access to both markets and finance is a constraint with most firms constrained to localised distribution and sales.

On an overall basis, SME’s in large parts of Africa suffer from some more structural issues that affect their ability to grow;

Lack of access to export markets largely due to trade barriers as well as infrastructural issues;

Fundamental issues such as skills shortages in the labour markets;

Erratic and unfavourable regulations particularly around elements such as business registration, taxes, permits and licenses;

Underdeveloped financial infrastructure from the number of bank branches to the quality of credit scoring infrastructure;

Legal barriers to owning and registering property particularly for women;

Barriers to obtaining legal identification;

Of course issues around smartphone penetration and internet access;

This is a useful resource particularly around the factors affecting women led SMEs;

Insights from Hilda and the Pezesha Team

Hilda generously gave me the following pointers as regards the main issues affecting SME finance;

On SME Workflows - “SME’s rely on antiquated business models particularly in retail trade which limits their productivity. The constraints in this regard are largely centred around the supply chain. Most SME’s in this case are in informal trade where they have to wake up very early in the wee hours to get the best prices from their suppliers in order to make a good margin. Sometimes they might not have the capital to buy inventory in bulk in order to then double their revenues. Not forgetting delayed payments from suppliers for goods sold.”

On how access to finance can help SME’s - “Access can help increase efficiencies and operational capacities, productivity, long term scale and competitiveness in the local and international markets. This can be further harnessed by the digital transformation of SMEs to reduce their operational costs and increase their productivity, which in turn can lead to improved data and potentially more access to finance.”

On why SME’s lack access to finance - “The root cause of the small and medium-sized enterprise financing difficulties lies in the information asymmetry that exists between SMEs and financial institutions. Asymmetric information means that one party has access to relevant information, while the other lacks the relevant information, or the information is no more than the former has.

Information asymmetry leads to adverse selection- credit rationing behaviour (leads to higher rates that could result to default, exclusion in the formal financial system because of ineffective ways to know ability to repay),

Information asymmetry leads to moral hazard (once loan is issued not knowing what it was used for, challenges of tracking productivity of the loan to effectively measure willingness to repay which then leads to bad debt or over indebtedness)

The transaction cost increase caused by asymmetric information (credit evaluation, alternative data sets access though fragmented and not complete to determine true creditworthiness, cost of acquisition/origination as most are informal)

Reduces Quality of SMEs that can be funded”

Given all this, Pezesha is focusing on the retail trade focused SME’s by sitting at the intersection between SME’s, the suppliers and sources of finance. Pezesha can define an SME and map all of their commercial relationships thus having a clear picture of both transactional and commercial data. This powers their “patascore” credit scoring system. According to Hilda, “Pezesha is a capital enablement lending infrastructure that is building a partner networks of SMEs that translates to a strong origination layer for our capital providers who are largely institutional lenders looking for productive optimal capital utilization by channelling quality credit worthy SMEs. Through our embedded financing approach we then integrate across supply chain verticals through our robust APIs to then access real time transactional data sets and at the back of that complete data we offer credit limits to merchants of a partner we work with such as Twiga Foods, Jumia among others. These partners are incentivised to use our lending infrastructure to bring efficiencies across the value chain from payments to credit value add that boosts sales and revenues across the entire chain”. In Hilda’s words, there will be significant value within the origination layer.

What elements are missing from the SME Access Stack?

When analysing the SME space in Africa, it’s clear that a lot has to be done before you can have widespread access to finance by SMEs. The issue can be summarised by telling the parable of the six blind men that originates from the Indian subcontinent. The story is one where six blind men who have never come across an elephant are told to learn and conceptualise about the elephant only by touch. Each man touches one part of the elephant and describes it based on their limited perception. One says it’s a tree by touching its legs and another claims that it’s a snake by touching its trunk. The lesson is that we’re quick to describe situations based on our limited perception.

Although conceptually different, approaches to SME finance have somehow mimicked this dynamic. Banks approach SME finance by trying to canalise the supply chain through proprietary SME value chain programs. FMCG’s view retailers in an almost exclusive manner as if that retailer only works with them and belongs to them. A new breed of tech enabled distribution platforms have a smarter approach but don’t yet have the scale to shift the needle so as to be the native distribution partners for anyone seeking to sell in the continent.

The natural consequence is disaggregated supply chains and most importantly, disaggregated and siloed data flows. Nobody has a single view of an SME by way of their commercial relationships, operational performance and transactional flows.

Traditional methods of credit analysis have always reiterated the need to understand some core elements of a customer. Ultimately, the repayment of a loan depends on a borrower's character, the businesses’ ability to operate as a going concern and afford the repayment as well as the borrower having some skin in the game in the form of equity contribution, collateral or something else of value. Additionally, in finance you have to ensure that moral hazard is avoided by checking that the proceeds of the loan are used for the right purposes.

All these have traditionally been verified by financial intermediaries such as banks and Micro-finance institutions. Banks and MFI at first identify the business through application forms and then conduct further due diligence prior to disbursing a loan. Credit officers then do continuous verification through site visits and monitoring. According to Hilda, the average annual credit demand for a small micro business from their experience is US$ 2,500. Thus the unit costs of lending to an SMB (Small and medium sized business) if traditional lending is to scale and cover the finance gap are not attractive. A different approach is required all together.

Additionally to this, one has to also solve for market access and in many instances education and business training on elements such as bookkeeping and financial management. SME’s need to actually grow their income even with existing financial constraints meaning wider access to markets. To solve for this, the following needs to be built;

A commerce platform that gives SME’s wider access particularly in terms of algorithmically matching buyers and sellers and lowering search and discovery costs;

Identity and KYC that maps individuals to their businesses including multiple businesses with underlying algorithms that lower fraud;

Data for both trade performance i.e. performance against trade agreements as well as operational performance i.e. efficiency. All this should enable someone to know whether the underlying SME is well run;

Off-line sales data;

Of course transactional data that can ideally match receipts with specific sales invoices or commercial actions;

Insurance and some form of skin in the game - credit life policies or a form of restriction to accessing commercial opportunities due to default;

The diagram above is a good representation. Starting at the bottom, one should solve for ID and KYC including commercial KYC. This then should interface with an e-commerce platform that acts more as a marketplace such as Taobao or AliExpress. Of course a payments layer that enables commercial payments orchestration including elements such as accounts receivable matching and reconciliation should be layered on top of this. At the end, data should be orchestrated to feed to third party sources of capital and financial products such as insurance and wealth management. Whether this is built by one person or is built by different people and orchestrated by one party is yet to be seen.

Hilda is trying to create the origination layer with Pezesha. The aim is to be the lending infrastructure that anyone can embed productive credit to SME’s. This is being done through three key elements, a credit scoring mechanism, a credit market place and lending APIs that can be embedded onto any platform.

Has this been done?

I started this newsletter with a quote from Eric Jing, the chairman and CEO of Ant Group since 2016. Ant Group has recently been in the cross-hairs of the Chinese government and in my view this is because they created a Leviathan that few had even comprehended prior to their IPO. Ant Group is an off-shoot of Alibaba which is one of the largest e-commerce platforms in the world through their various brands such as T-Mall, Taobao, Lazada, Ali Express and Alibaba. These cover the full gambit from local B2C to global B2B. In 2004, Alibaba formed Alipay to solve a trust issue within the commercial side of the business. Alipay enabled escrow transactions between two parties, holding funds until one side of the transaction fulfilled their obligation.

From this, the company has gone strength to strength to become a giant. Currently, the empire that Jack Ma has built is a commercial leviathan. Imagine if Bill Gates owned Shopify, Spotify, Netflix, Amazon, E-bay, Paypal, Metromile, AWS and Lemonade all under one roof and all being no.1 in their respective categories. Despite these companies having different ownership structures, one thing that is emphasised in the Ant Group IPO prospectus is their sharing of “insights” read data. This enables them to develop capabilities that few companies in this world can.

Prior to its IPO, Ant Group had partnered with over 2,000 financial institutions to power an array of products ranging from wealthtech to credtech. It had SMB balances of US$ 62 billion and total loans disbursed via its credtech platform of US$ 262 billion. Investment and AUM enabled through their platform totalled US$ 617 billion.

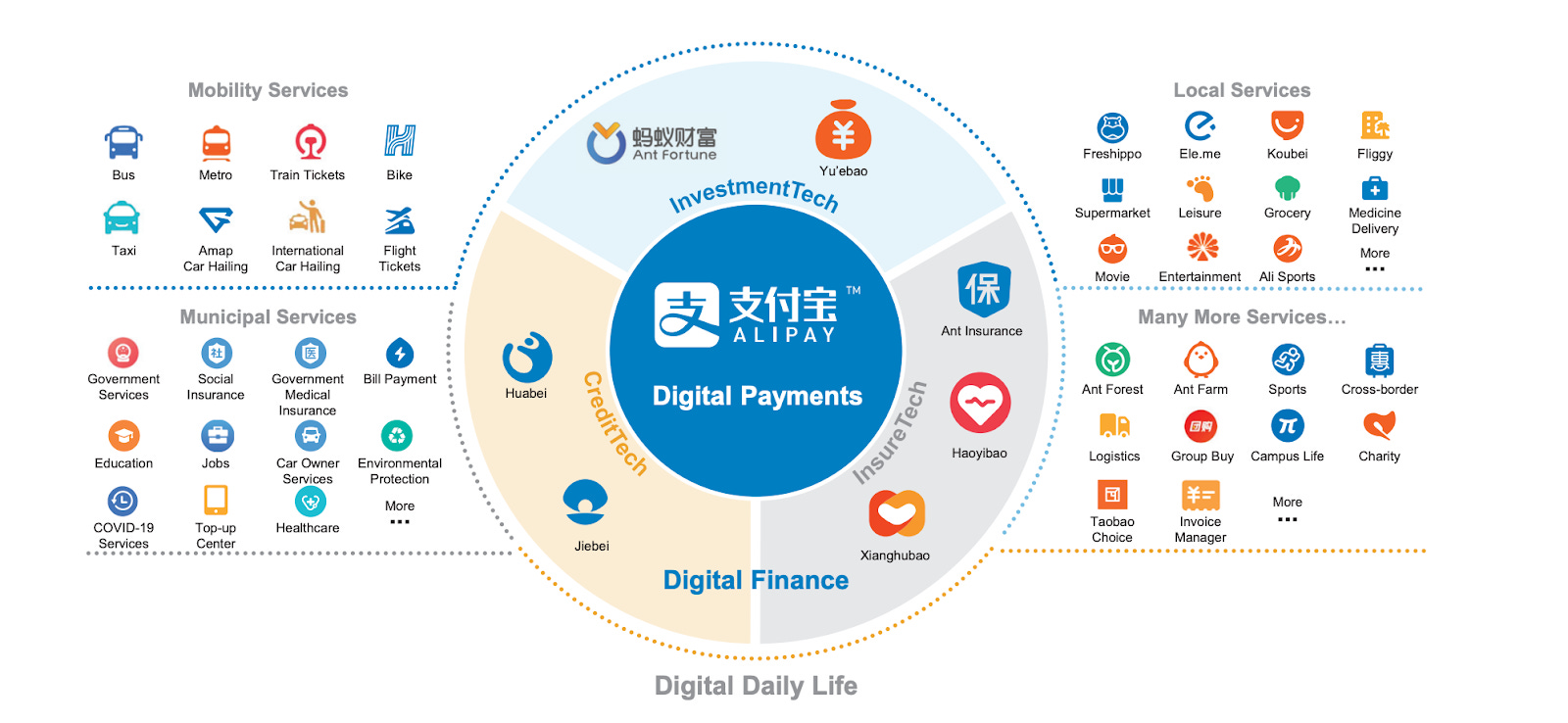

Alipay Ecosystem

The above shows the Alipay ecosystem which of course is augmented by an additional layer that includes T-mall, Taobao, AliExpress and Alibaba data. Ant Group is thus able to solve for;

A clear understanding of a company’s operational and commercial performance;

Clear identity mapping both individuals and entities;

Online and off-line transactional performance from Alipay online and off-line QR code performance;

Transactional data that matches commercial actions such as invoicing to payments;

Additional data including insurance, utilities, education and tax data;

Real skin in the game since Ant Group essentially runs your life;

Ant Group has managed to achieve world beating performance with delinquency rates of 1.05% for loans that have been over 90 days overdue. For D30+ i.e. 30 days overdue, their delinquency rates are 1.56% as of 2019 prior to IPO. When you look at delinquency per vintage, their credit performance seems to have been improving. All this despite covid. Ant Group showed that SME lending can be empowered using a noble approach. One thing I admire about Chinese tech is their super first principles thinking based on a global macro view of how everything works. African fintechs should adopt the same thinking rather than trying to build the “insert American tech giant” for Africa.

The solution to SME Access to finance is thus a whole re-think of how SME’s relate to their clients, their suppliers, financial partners and any other commercial relationship. This ideally should be digitally native rather than a digitisation of current analog practices. This will then supercharge the access to finance. Remember, the industrial era had built in exclusion as part of design. SME’s lacking access to finance is thus part of the game. To change this, we have to build a different system.

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@gmail.com;

Interesting piece...Pezesha is doing good things, Hilda is amazing!

Disagree that every business needs some sort of online market to help get access to bigger markets. While having such a market would be nice not every SME would need it. Agree with almost everything else though.