#14 Digital Consumer Fintech Propositions

Core factors to consider when building the next iteration of Consumer Finance Apps

Hi all - This is the 14th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends. 🚀

Consumer facing fintech applications are a growing area of interest for investors, banks and consumers as well. Over the last decade, underlying technologies such as APIs, Artificial Intelligence, Cloud Computing and Big Data have all converged to enable companies to create new digital offerings. I will focus on the banking sector and will look at the evolution of bank apps and where they should be headed. There are four big themes that emerge within this field;

Social;

Lifestyle and Marketplaces

Artificial Intelligence and Machine Learning;

Integrated Finance;

Any bank that is building a digital consumer app will have to figure out how to embed these four core elements onto their app.

Evolution of Bank Apps

Most bank apps globally were launched following the advent of the iPhone and the app economy. Prior to this particularly in Africa, bank apps were built using either STK or USSD technology. Many apps still run on USSD largely due to the prevalence of feature phones in the market. The first iteration of apps either USSD or Android/IOS apps were simple transactional apps where banks created new digital transactional journeys for basic transactions such as funds transfer, buy airtime, account balance queries and mini-statement requests. This phase started in the mid 2000s and lasted until say 2015.

Thereafter, with the launching of apps such as Revolut and N26, the story changed towards creating sleek user interfaces. At the time, Netflix had gone global and other social media apps such as Instagram and Twitter had achieved mass adoption and become cultural icons. The story was that customers have come to expect seamless customer journeys and sleek user interfaces and they will expect the same from their bank apps. A cottage industry of vendors and consultants formed out of this zeitgeist.

Banks then rushed to upgrade their apps and make them more sleek. Nonetheless, the core functionality didn’t change from the existing transactional capabilities. It was a sleeker way of doing a funds transfer and seeing your bank balances. A number of banks additionally tried to digitise the onboarding process, nonetheless due to both regulatory roadblocks as well as strategic missteps, these onboarding processes were clunky and inconvenient for customers.

Phase 2 of the bank app evolution has not been a big success. Globally most of the banks that were premised on sleek user experiences and a more seamless transactional experience have not yet hit profitability. Revolut for instance has gone global but has yet to achieve sustained annual profitability.

This is giving way to a new and more comprehensive framework for thinking about creating and building a digital consumer financial experience delivered via an app. This third generation of consumer apps will be more robust and will deliver intuitive financial experiences. Banks need to focus deeply on this because in the long-term, distribution will be purely digital and in this world, winner take all or most dynamics will be fully in play. With a sizeable Gen-Z population in Africa, this race is critical to banks if they want to maintain a profitable retail bank years into the future.

The Four Elements of 3rd Gen Digital Consumer Apps

Social

Traditional banking as well as any other traditional sales relationship were built around owning the customer relationship. This teaching has been handed down generation after generation to a legion of relationship managers and sales reps. It works, having a relationship with your customer is critical in business and good customer care is very important. Most of us have been unhappy with the services we are offered by our banks but turn a blind eye because we’re good friends with the branch manager or customer service representative.

With the digitisation of financial services, banks have to replace this emotional connection with something otherwise the customer relationship will turn cold and purely transactional. To counter this, it’s important to embed social into your app. According to Andreesen Horowitz, Social refers to mobile apps that enable peer to peer interactions within a definite network of users.

It’s important that your client base within your app share some specific characteristics such as age group, type of economic activity or shared interests such as trading or investing.

The idea behind this is to drive engagement with metrics such as the DAU/MAU ratio i.e. daily active users divided by the monthly active users. This shows whether your client base interacts with your app on a daily basis and is a measure of “stickiness”.

Source: a16z

The table above shows DAU/MAU ratios for some of the most popular apps. Audio apps have the highest DAU/MAU ratios followed by social apps such as instagram and Facebook. It’s interesting to note that Sberbank of Russia has a DAU/MAU ratio of 64% or just slightly above Twitter.

To embed social into Fintech you need to separate your transactional layer and interaction layer. Thereafter you have to figure out how you want to create social features based on factors such as type of client base, demographics, social maps and common interests amongst your client base.

Tinkoff has done this by launching Tinkoff Pulse, a space where Tinkoff investment clients can share ideas on trading and share their portfolios. Apps such as Public and Commonstock have built a business model around social and investing. In Kenya, there’s a platform called Wazua that’s really good for connecting and talking to fellow investors in the Nairobi Stock Exchange. Apps such as SoFi and Liv by Emirates NBD have embedded features such as “Stories” - company generated content that’s delivered in the “Instagram Stories” format to app users. This social element also has the powerful capability of driving cross-sell, if you see that your friend who you like has just bought an insurance policy, then it will make your decision easier. 11onze a catalan neobank has launched a Facebook style private social network.

Additionally, companies can rely on existing social networks such as Youtube, Instagram and Facebook. At a lower level, banks can create Telegram groups for specific customer segments to experiment on the type of interaction and engagement that will emerge from their customers. Building social is very difficult from both a technical and commercial perspective but going back to the initial hypothesis, the nature of the “customer relationship” is changing from a face to face relationship towards a digital app relationship. Social features will enable stickiness. Moreover, I have always been skeptical of the idea of “you must own the customer relationship”, ultimately in the past this relationship has been owned by the sales rep or branch manager and not the bank. Proprietary social features will enable the bank to fully own the relationship and no longer worry about losing RM’s to rivals.

The key considerations are;

How do you want to segment your clients as regards to social interactions - SME clients can have an SME hub where they discuss business hacks and other commerce related issues and retail can discuss their finances - this can also be useful for Rotating Credit and Savings Associations (ROSCAs) or chamas in Kenya;

Everything has to be data driven - all social apps run on big data to determine what content to deliver to their clients. I have seen bank apps that have media content but it’s delivered in the old media way of creating expensive content and distributing it en masse to the clients. Social works when you only see content that’s relevant to you;

Content teams need to be built and led by a senior executive. The KPIs around this should be growth in DAU/MAU as well as Net Promoter Scores. Kaspi a mammoth super app from Kazakhstan, manages its products exclusively on their NPS and sets minimum NPS standards. They can even pull a profitable product if it has a low NPS.

It’s a big gamble, but it’s worth taking. A world class digital app with a well designed social element will aggregate market share. Key to remember is that distribution will be fully digital.

Lifestyle

Commercially, the lifestyle element is driven by the same considerations as social in the sense that Lifestyle enables you to create stickiness by increasing DAU/MAU ratio. Ultimately, if a customer is interacting with your app on a daily basis then with time it becomes easier to monetise that customer.

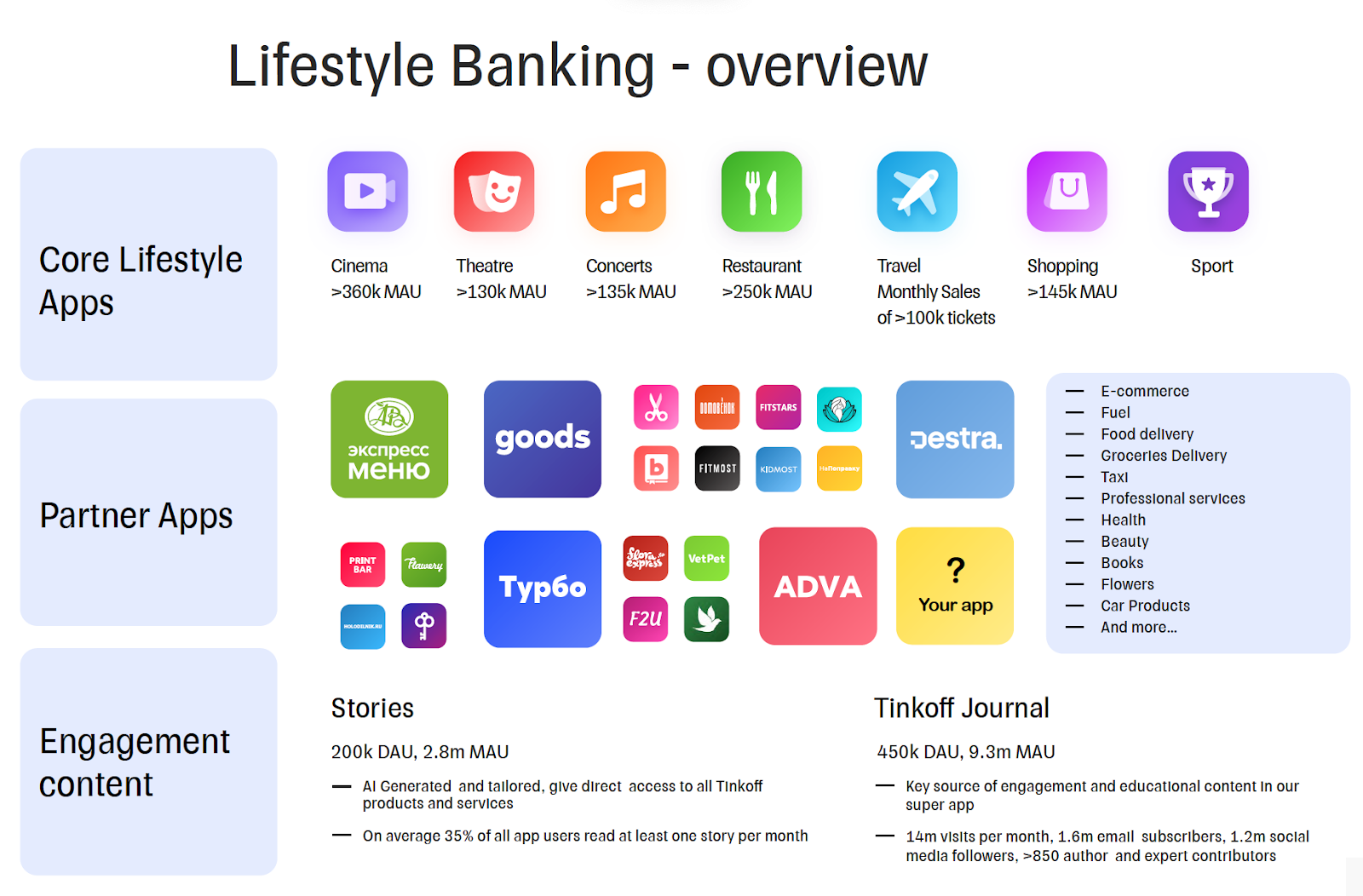

Lifestyle is really built around being a core app that caters to the lifestyle requirements of your customers. This includes shopping, travel, education, health and wellness and other lifestyle considerations. The image below from Tinkoff shows how the bank thinks about lifestyle banking.

Source: Tinkoff

The bank has core lifestyle apps such as cinema, theatre, concerts and others whilst at the same time integrating via APIs to enable e-commerce, food delivery, taxi services and others. This is all delivered in-app in an intuitive way running on top of the payments and transaction layer.

The above is an interesting video that shows how commercially, the lifestyle segment is managed. In addition to driving NPS and DAU, lifestyle is managed on a break-even basis with commissions from third party integrations being given back to users as direct cash-backs. So for instance, if you have integrated into a travel agency and have a 3% sales commission as the bank, then you give this 3% back to the customer. The idea of social and lifestyle is to drive engagement and stickiness.

Banks have catered to the idea of lifestyle banking for a long time. It’s not a new concept really. Banks offer discounts on travel, club membership and other items based on concepts such as bank points (driven by your transactions) as well as credit card membership. However, the key with the new lifestyle paradigm is the same as social, it needs to be driven by hyper customisation that runs on big data and AI/ML. It’s largely a distribution issue.

That being said, there are some core issues that make integrating lifestyle intuitively difficult to implement;

Poor client data largely due to legacy data infrastructures thus making it difficult to customise lifestyle offerings;

Most partners e.g. travel, health and entertainment are yet to APIfy their businesses particularly in Africa so most travel agents can’t give you good, scalable APIs to integrate to. This significantly impacts your lifestyle and marketplaces strategy - some banks have had to build their own ecosystems around this;

GDP per capita as a proxy of discretionary income in Africa is still low. Kenya has a GDP per capita of US$ 1,816 with Nigeria and South Africa having GDP per capitas of US$ 2,229 and US$ 6,000 respectively. This compares against countries like Singapore and UAE which have GDP per capita measures in excess of US$ 50,000 - this hampers both smartphone penetration and the spending power to actually monetise lifestyle offerings;

Current bank organograms are not optimised for the effective implementation and management of a lifestyle offering. Banks that have hived off their customer propositions and integrated their teams into product management, marketing and technical mini squads are better placed to execute;

Artificial Intelligence and Machine Learning

AI and ML are two of the most over-used yet least understood aspects of modern technology. Everybody bandies around these terms in their product presentations and long-term strategy documents. In this case, I will simplify this to mean the effective use of aggregated customer data to be able to predict the following. I’m not an AI expert;

Consumer Intent;

Consumer demand;

Consumer wants and preferences;

Content and engagement;

With regards to consumer intent, this basically means that the AI should be able to predict what the customer wants to do and what his/her intentions are. This is typically implemented through chat bots. Liv by Emirates NBD has a chatbot called Olivia which is a personal assistant on your Liv app. In the case of a chatbot, when you type in “i have lost my card”, through natural language processing, the AI should interpret this and give you options for renewing your card and potentially give you tips on how you should secure your card in the future. This can also be applied to customer decisions, based on your interactions within the app, the AI should be able to predict that you actually intend on purchasing an insurance policy or book a holiday. Consumer intent goes beyond superficial elements such as what the customer is requesting to what the customer actually wants.

This ability to predict consumer intent is also useful for predicting consumer demand and understanding a consumer's tastes and preferences. This is a crucial issue actually. The 2nd iteration of consumer apps built Personal Financial Management (PFM) tools to help customers budget and track their money. Nonetheless, the issue with PFM tools is that most people actually dread budgeting due to the negative emotional feedback loops that occur when you fail to follow your budget. So asides from super-users who are avid budgeters like myself, these PFM based apps failed to scale. Shamir Karkal, the founder of Simple describes why PFM doesn’t work and the lessons learned from building Simple in this podcast. The idea is that the AI should learn how you transact and automate your money intervening only to show you better ways of managing your finances. For instance, if your app knows that you usually have US$ 500 sitting in your account at any given occasion, it can offer to move that money into a savings account automatically. It’s a critical point, social media has made people lazy and the plethora of choices that we have to make in the modern world has led to a populace that wants automation. How many of us have turned on the TV to watch Netflix only to spend an hour trying to figure out what to watch.

As regards content and engagement, big data should be utilised to customise your home page based on your intents, your purchase habits and your tastes and preferences. This will drive more engagement and spark a wow factor amongst your users. Ultimately social is built around customisation and the greatest social app of our time “TikTok” is built around a world class AI and ML engine. Everyone who downloads TikTok gets addicted.

Of course the main considerations around AI are;

It’s difficult to build expertise around this particularly in Africa where technical skills are scarce - My friend told me about Microsoft and Google offering developers in Kenya Restricted Stock Units (RSUs) with current strike prices of US$ 2 million. I can imagine that the rush for data scientists and AI experts is even worse - Nonetheless there are companies that offer AI as a service and integrate to your app;

Existing data architectures are not built for AI thus hobbling any AI/ML strategy - Anyone keen on jumping into a data architecture rabbithole should read this;

Attitudes towards AI and ML are evolving - there is the concern about utilisation of customer data and there is the issue that practices around how staff and management interact with AI are yet to be perfected;

Integrated Finance

There is a move towards a more integrated financial experience. My view is that people have one financial life that includes financial opportunities, goals and aspirations as well as risks and concerns. We live one financial life, but we are forced to have a disjointed financial experience. For instance, an impending car insurance premium that is due within one month has a direct impact on my future bank balances.

In the long-run, my view is that banks need to integrate their financial products to align with the financial realities of their customers. This means integrating insurance, savings, wealth management, private banking and consumer banking into an app. Of course this involves thinking about organisational structures and customer facing divisions. One of the main issues is that within a financial services group, different divisions typically have mis-aligned incentives. I remember working in a stock brokerage unit of a bank and the bank RMs didn’t want to refer their HNW clients to us because this resulted in a lost deposit and share of wallet for them. This is going to be disrupted by technology and banks need to develop strategies around this.

In a recent Ernst & Young report, survey respondents were asked how they expect to change their wealth management service providers. 73% responded that they will shift towards Neobanks and Fintechs whilst 10% said they will shift away from retail banks.

Neobanks are rebundling financial services. Starting with basic P2P propositions, players such as CashApp and Venmo are adding functionality to become financial super-apps. Therefore digital consumer apps need to include the full suite of services with a single integrated view of a consumers’ financial situation. Grab starting with a taxi service has built an integrated financial service behemoth in South East Asia. The new Mpesa app seems to be designed with this type of bundling in mind.

The graph below shows that mass affluent customers who tend to be younger would prefer to shift towards one single provider of all their financial needs.

Some Final Considerations;

There is a very high level of executional risk and this has been evident in the markets - a more agile approach will be very useful. Most banks have waterfall commercial decision making with agile software development tools. The whole approach should be agile from the get go;

Tech expertise is hard to scale and maintain;

Organisational structures need to evolve - the roles of a Director of Retail should be reviewed as regards what his main objectives should be and the reporting lines across marketing, technology and commercial;

There should be a review of core platforms and your vendor ecosystems - what do you build and what do you buy and even importantly, how do you buy - SaaS or annual licenses;

Different markets have different realities - building social in Russia and China has been made easier by the fact that existing giants such as Instagram and Facebook aren’t in those markets. Facebook is like the homepage of African internet and it is thus difficult to make a dent in terms of attracting attention to your app;

Of course all capabilities need to be omni-channel including relationship managers and advisors where necessary;

As always thanks for reading and drop the comments below and let’s drive this conversation.

If you want a more detailed conversation on the above, kindly get in touch on samora.kariuki@gmail.com;