#122 - Expansion Mode

Why payment data won’t make African retailers more competitive, and what will.

Illustration by Mary Mogoi (New Link)

Hi all - This is the 122nd edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends.

A Map of the African Entrepreneur

How much of what we call inefficiency in African commerce is actually adaptation we have not bothered to read?

Take John (not his name), a Burundian entrepreneur I came to know during my years banking in Bujumbura. John was a client and, over time, a friend. He grew up an orphan, selling individual cigarettes on the streets of Bujumbura, the kind of micro-retail that fills the gaps in cities where the salaried economy is thin and the cash economy is everything. By the time I met him, he had built two ships that worked Lake Tanganyika, moving freight between the Burundian, Tanzanian, Zambian and Congolese shores.

His business was specific. He bought Dangote cement in Zambia, where it carried a reputational premium over the local product, and moved it across the lake into Bujumbura and eastern Congo. The economics worked because he owned the ships; he had pulled marine transport inside his own balance sheet. He planned to extend the routes to the Comoros and Beira. His insight was that the real money lay in trading the goods being ferried, not in offering shipping as a service.

The longer I knew him, the more his operating principles read like a careful summary of Warren Buffett. He worked inside a defined circle of competence, carried no debt, reinvested cash flow rather than diluting equity, thought in terms of moats, and held a margin of safety on every shipment. He had never read Berkshire’s annual letters; he had taught himself to read only much later in life. He had derived these principles himself.

The story does not end well. Competitors coordinated with people in Zambia to overload one of his ships beyond its safe waterline, and the lake did the rest. That is Africa for you in one sentence; the same environment that produces operators of John’s calibre also produces the rivalries that can sink them.

Entrepreneurial talent on this continent runs deep, and John is one expression of it. The most visible version is Aliko Dangote, whose cement John was shipping, scaled from a home market into the largest industrial fortune in African history and now, through his refinery, catalysing industrialisation across Africa. Between John and Dangote sits an enormous middle of traders, hauliers, shopkeepers and small manufacturers whose behaviour, viewed through a Western retail lens, looks informal or sub-optimal. Most of it is contextually rational behaviour by operators who read their environment more accurately than the frameworks applied to them.

This week’s issue is the digitisation of retail payments in Africa. One argument I have heard repeatedly is that retailers should adopt digital payments because the data exhaust improves their business through better product insights and inventory management. The evidence does not support this. Operators like John have read the situation accurately; a specific set of conditions has to exist before payment data becomes useful for African retail. The argument runs through the global cases that built the playbook, the state of African retail today, and the structure of the data that digital payments here actually generate, before closing on what would make the data story a real pull factor.

The Argument for Payments Data

The argument for digitising retail payments comes in three layers. The most defensible is operational; cash handling carries costs that digital does not. The second concerns credit; transaction history substitutes for collateral and underwrites working capital, which I have explored at length elsewhere. The third is the one that interests me here. The data exhaust from digital payments, the argument runs, helps the retailer run a better business; better assortment, sharper inventory, more targeted marketing, eventually a share of the advertising revenue that brands pay to reach the retailer’s customers. It is the argument cashless advocates reach for when the cost case alone does not move a merchant, and it has the longest intellectual lineage of the three.

Clive Humby and Edwina Dunn - Image Source

In 1989, two London marketing researchers called Clive Humby and Edwina Dunn founded a consultancy named dunnhumby. Their bet was that supermarket transaction data, properly analysed, would reveal more about consumer behaviour than any survey panel could. The bet had a quiet six years before Tesco hired them in 1995 to design a loyalty card, which the retailer launched that February as the Tesco Clubcard. Within months, dunnhumby presented the first analysis to the Tesco board. The line that came out of that meeting has been quoted in every retail business school case since. Tesco’s chairman, Ian MacLaurin, told the room that this small consultancy had, in three months, learned more about his customers than Tesco had learned in thirty years.

Former Tesco Chairman Sir Ian MacLaurin - Image Source

The line is usually told as a parable about the magic of data science. Tesco in 1995 had several hundred stores nationally, an established Clubcard infrastructure that within five years would reach 14 million UK households, basket-level scanning at the till, and a CPG ecosystem already paying for syndicated consumer panels from Nielsen and IRI. dunnhumby could read the data in three months because Tesco had spent thirty years building the conditions under which it became readable.

What Tesco built on top of that base is the playbook every modern retail media network has followed. By 2001 the retailer had bought a controlling stake in dunnhumby for around thirty million pounds; by 2010 it owned the business outright. The consultancy itself last filed revenues of £372 million, a substantial business but smaller than its mythology suggests. The real value sits one layer above. Tesco Media and Insight, the in-house retail media network, now runs 17,000 campaigns a year for Coca-Cola, Procter & Gamble, Nestlé, Unilever, L’Oréal and McDonald’s, reaching the 23 million UK households that hold a Clubcard out of 28.3 million UK households in total. Tesco is no longer selling groceries with advertising on the side. It is selling audience access to consumer goods companies and using groceries to assemble the audience.

The model has scaled internationally and the numbers are now large enough to reshape the industry. Walmart Connect generated $4.4 billion in advertising revenue in its 2024 financial year, growing 27 percent year on year, reaching the 255 million customers who walk into a Walmart store each week across 10,500 outlets in nineteen countries. Amazon Advertising generated $56.2 billion in 2024 and captures roughly 77 percent of US digital retail media spending. Kroger Precision Marketing sits on 60 million American households whose behavioural data is tied to a Plus Card loyalty profile, with 96 percent of transactions identified at the basket level. Retail media as a category passed $140 billion in global revenue in 2024 and is projected to clear $200 billion before the end of the decade. In several markets it has now overtaken traditional television in absolute scale.

This is part of the playbook African payments companies and cashless advocates point at when they argue that digital payments will, in time, generate similar value for African merchants. The argument is not foolish; it has working examples, substantial revenue, and a clear mechanism. The narrower question is what Tesco, Walmart, Amazon and Kroger actually had in place before any of this became possible, and how much of that exists in African retail today.

The Nature of Retail in Africa

Tesco had several hundred stores at full national coverage by the mid-1990s, all operating against a saturated United Kingdom grocery market in which the only remaining growth lever was extracting more value from each existing customer. Walmart Connect launched in 2021, by which point the company operated 4,700 US stores, served roughly 240 million customers a week, and had reached every viable American town. The expansion phase that built the network was structurally over; the marginal growth lever had shifted from opening new stores to monetising the audience the existing ones had assembled. Amazon Advertising became material on the same logic, after the marketplace had spent two decades assembling a user base it could then sell access to.

Retail value-added services is the playbook of mature retail. Its prerequisites are specific: massive store networks at near-saturation, persistent customer identifiers linked to baskets across visits, and a consumer goods ecosystem already paying for audience measurement and ready to redirect that spending to a richer source. None of these are about payments. They are about the stage of retail development on which payments data eventually sits.

I made the same structural argument in the BNPL piece. Point-of-sale-integrated consumption financing works in South Africa and not in Kenya because South Africa has formal retail at the density that checkout-integrated products require, while Kenya’s overwhelmingly informal retail makes productive-asset financing the dominant model. The optimisation layer requires the formalisation layer to have been built first.

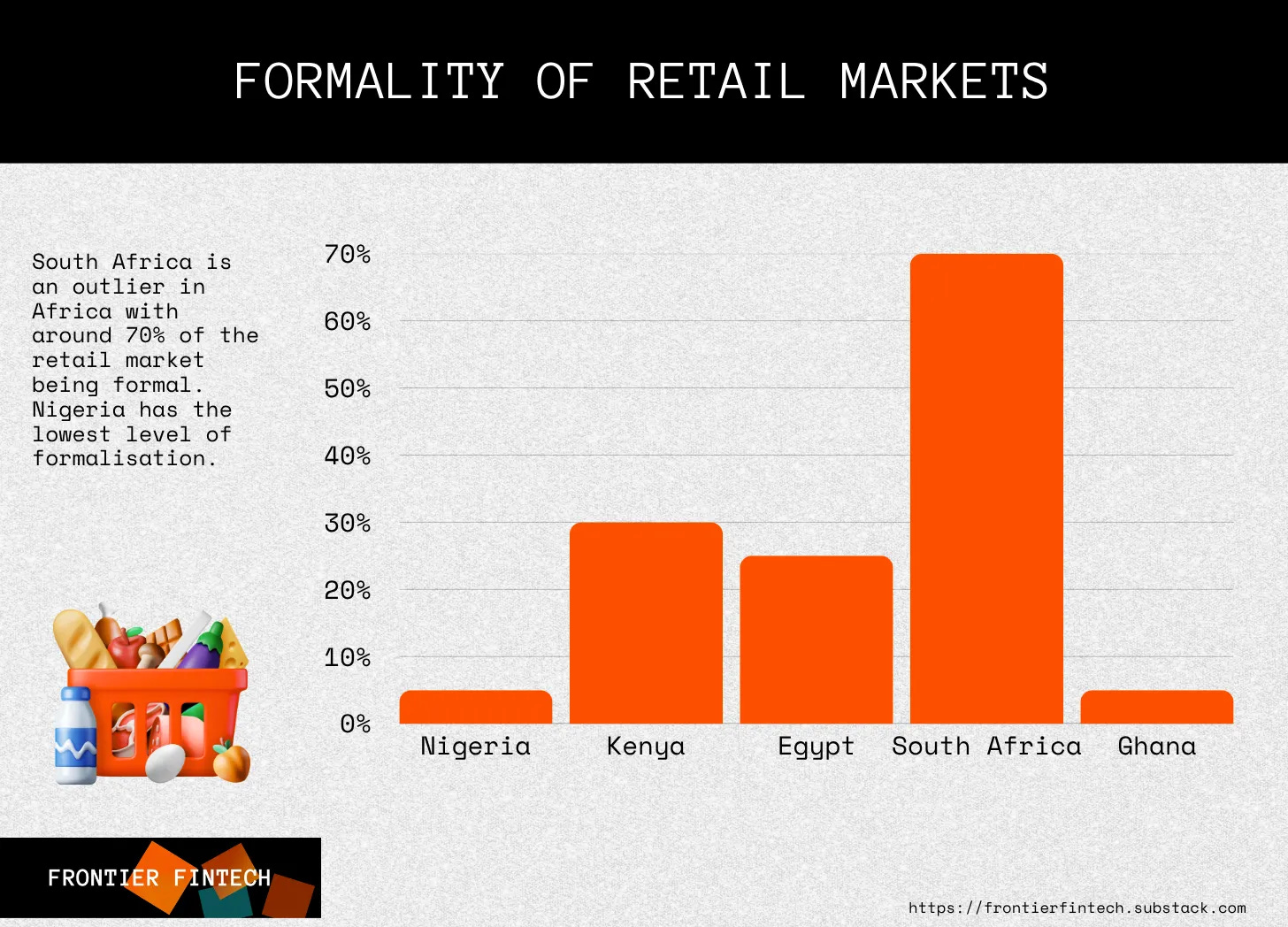

The honest exception in African retail is South Africa, and within South Africa the exception is Shoprite. The Xtra Savings programme covers 33.7 million members. The card processes more than 2,500 swipes per minute. The Shoprite Money Market Account it anchors sits on over 530,000 active users, and the Xtra Savings card itself now functions as a debit card. This is the only African operation whose data density approaches dunnhumby or Kroger Precision Marketing levels, and it exists because South Africa is the one African market where the prerequisites are present; a $72.6 billion formal retail base, five chains controlling most of the grocery market, and a banked middle class trained on loyalty cards.

Formality of African Retail Markets

The detail that matters is where the data play sits. Xtra Savings is owned by Shoprite. The data layer was built by the retailer, on top of its own store network, using its own identity infrastructure. No payments operator built it, because no payments operator could. The data play in mature retail is internal to the retailer because the retailer owns the prerequisites; the network, the loyalty identity, the basket-level capture. A payments network sitting outside, however large, cannot assemble the data into the form a CPG buyer will pay for.

This also explains why the wider South African case complicates rather than refutes the thesis. South Africa is two economies. The first, where Shoprite operates, looks structurally similar to a developed market. The second, where spaza shop networks carry the bulk of township grocery spending, looks nothing like it. The South African informal economy is estimated at US$61 billion, with the spaza sector alone at US$11 billion, and BFA Global puts the share of informal retailers accepting electronic payments at 1 percent. The exception that proves the thesis is not Shoprite as a whole. It is the precise wedge of Shoprite that sits inside the first economy, with a customer base whose identity and basket are captured at the till.

Outside that wedge, across the rest of the South African economy and across virtually all of the rest of the continent, the conditions that made Tesco’s 1995 moment possible have not yet been built. Which raises the next question. Even setting aside the structural readiness problem, what does the data exhaust from digital payments in Africa actually look like? What is in the file, and what is not?

What Payments Data is Generated in Africa?

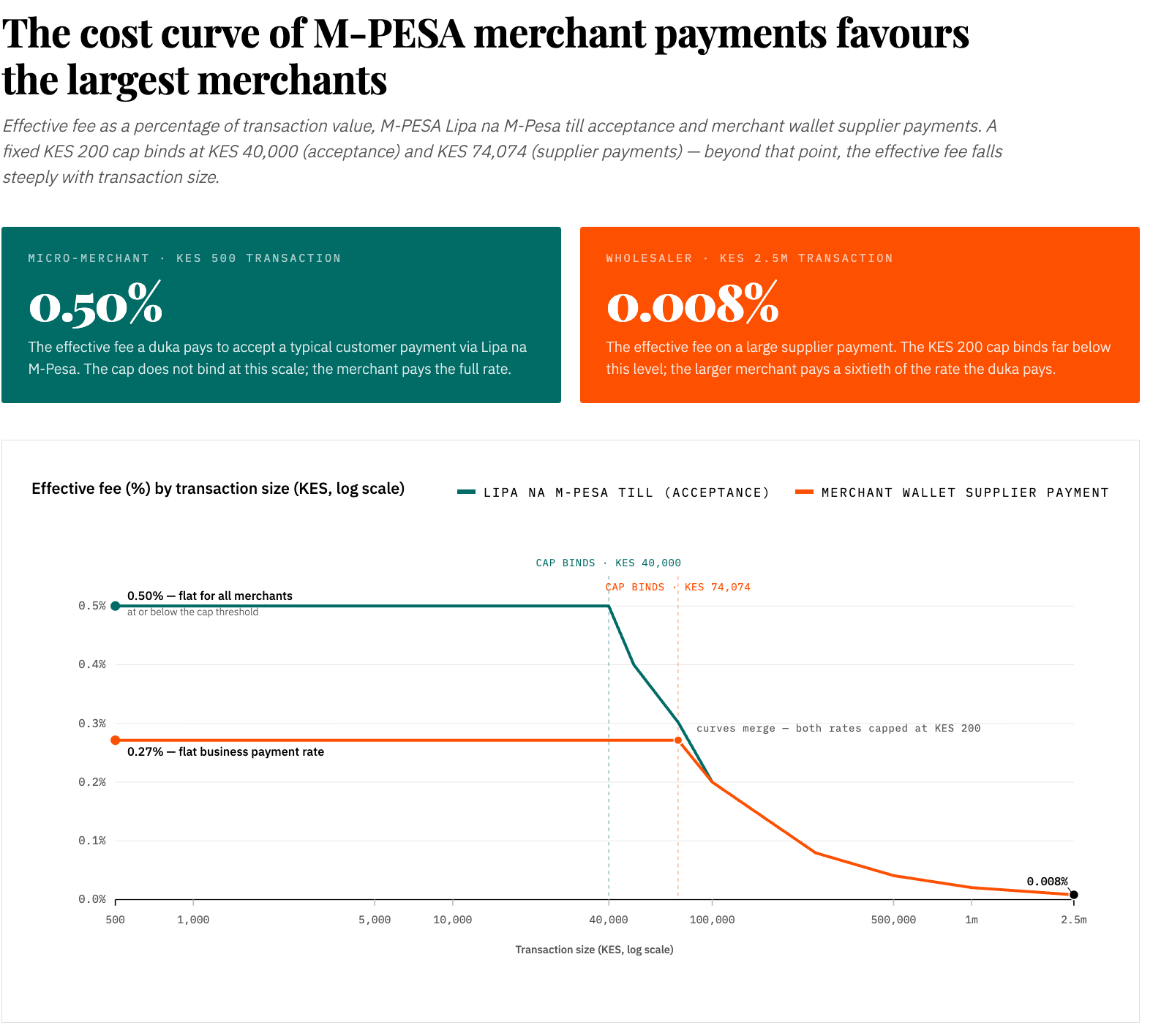

Set against this background, the data that African digital payments actually generate becomes the question worth interrogating. We can look at Nigeria and Kenya which represent card, mobile money and digital bank dynamics. The data that a Lipa na M-Pesa till generates when a customer pays a Kenyan merchant arrives as a callback message containing the transaction type, a transaction identifier, the timestamp, the amount, the business shortcode, the customer’s phone number, and the customer’s first, middle and last names.

That is the extent of the payment file. There is no SKU, basket, category, product code, demographic enrichment or persistent customer identifier across visits. A Moniepoint POS card payment generates a thinner file still — amount, timestamp, masked card number, terminal identifier, merchant category code. The data exhaust that the cashless argument depends on, the basket-level signal that dunnhumby reads in three months, is structurally absent from the rails that currently dominate African merchant payments.

What I find most striking in the latest Safaricom results is buried in the Pochi la Biashara line item. Pochi is not a true merchant rail. It is a personal M-Pesa wallet relabelled for business use, with no business shortcode, separated reconciliation API, or callback identity beyond what the sending customer’s phone number reveals. By the end of FY26, Pochi tills had reached 1.15 million accounts, growing 81.7 percent year on year. Active Lipa na M-Pesa merchants, the proper merchant tills, sat at 675,000. The dominant “merchant” channel in the most digitised payments market in Africa is, structurally, P2P with a different label. Whatever data exhaust this channel generates is not merchant data in any meaningful sense.

Safaricom waived merchant fees on transactions below KES 1,000 during the COVID period, and the band remained free thereafter. The arithmetic that has followed is striking. Of the 21.9 billion M-PESA transactions processed in H1 FY26, 13.9 billion sat under the free Kadogo band. The bulk of M-PESA’s transaction volume now flows through a tier that generates no per-transaction revenue, which sharply limits the pool available to fund deeper merchant data infrastructure even if Safaricom wanted to build it. The same cost logic shapes merchant behaviour. In downtown Nairobi, merchants routinely ask customers to send to a personal number or withdraw from an agent rather than pay to a till, because the till charge, however small, eats directly into a margin that is already thin. The cheapest rails win, and the cheapest rails are the ones that generate the least merchant-attributable data. Pochi is the product of that selection pressure as much as it is a deliberate Safaricom design.

Nigeria adds the parallel distortion from the other direction. The headline figure of 1.5 billion POS transactions worth 18 trillion naira in 2024 is overwhelmingly cash-in and cash-out activity by agents rather than retail purchase, after the industry built a network designed primarily to replace failing ATMs. The Central Bank of Nigeria’s October 2025 guidelines now explicitly require agent banking to carry merchant category code 6010, separated from genuine merchant transactions. The data exhaust from a CICO transaction reveals cash demand at a point in space and nothing about what was purchased.

The direction of travel reinforces all of this. In March 2026, Safaricom announced that by the end of the year it would extend data minimisation across M-PESA, removing full customer phone numbers from merchant SMS and callback notifications for both Buy Goods and Paybill flows. The Tesco arc moved toward richer customer identification at the till; the Safaricom arc is moving deliberately away from it. The rails that the cashless argument depends on to eventually generate dunnhumby-grade data are, in the dominant African case, walking in the opposite direction.

Why the Data Argument Doesn’t Hold

The data exhaust argument assumes a retail sector in optimisation mode. The African retail sector, at every level, is in expansion mode.

Begin with the large formal chains. Shoprite has 2,000 stores across eight brands and has already built the loyalty layer; it is the exception. Everywhere else the picture is structurally different. Naivas operates around a hundred stores in Kenya and continues to open new locations. Carrefour is still building out its Kenyan footprint through Majid Al Futtaim. Bokku has opened more than a hundred discount stores across Nigeria since 2022, and the wider Nigerian discount-format wave is in early innings. The growth lever is opening more stores; the tools are real estate, supply chain, working capital, and operational consistency. Africa is where Sam Walton was in the 1960s and 1970s, when the goal was supply chain optimisation and store expansion, not data.

The informal segment is the larger and more interesting case. A duka in Kawangware, a spaza in Soweto, a kiosk in Onitsha typically carries thirty to eighty SKUs and serves a customer base the owner knows by name. The owner is the analytics engine. He knows that Royco cubes outsell Knorr and by how much, which customers buy on credit and which pay cash, which days move volume and what stock is sitting. A payments dashboard would tell him things he already knows. The framing assumes a retailer operationally distant from his own business; the informal African retailer is inside it in a way no dashboard improves.

He is also not pessimistic. BCG’s 2022 work on traditional retail in Africa found that 79 percent of Kenyan retailers and 88 percent of Nigerian retailers expected their businesses to grow. These are growth-oriented operators whose binding constraints are working capital, stock, supply, and security. The data exhaust diagnosis has identified the wrong constraint, and it is at odds with observed behaviour: BFA Global’s work in South Africa found that only 1 percent of informal retailers accept electronic payments at all.

Two issues run underneath this. For the large chains, the real lever is moving formal retail’s share from 20 to 40 percent — that is where the upside sits. For the small merchant, payment data adds nothing he cannot already see, and the binding constraint is working capital, which is downstream of data. What connects them is cost structure. The charts below show the cost of receiving and sending payments on a Lipa na M-Pesa till; the logic holds for OPay and Moniepoint. The cost curve favours larger retailers, which explains a lot. For the chain, digitisation is a cash-handling improvement, not a data play.

This brings us back to where the article opened. John was not running a sub-optimal business because he had failed to digitise his payments. He was running a disciplined operation inside a circle of competence. The cement traders, the spaza owners, the dukawalas, the Nigerian discounter operators, the Naivas store managers are doing the same thing at different scales. The continent’s retail economy is operating on the toolkit appropriate to its current stage. The data layer will become useful in time, on the same trajectory Walmart followed, once the expansion phase has built the network on which it can sit. Trying to summon it first solves a problem that does not yet exist at the merchant’s level.

The Direction of Travel

The most interesting voice on this question is not a critic of cashless payments but a believer. Ali Mazanderani, chairman of Lesaka, has built one of the largest fintechs in Southern Africa around the conviction that digitising African commerce is one of the defining themes of his generation. In a recent conversation he reached for an analogy I have heard him use before. The digitisation of commerce is like electricity. The first use case may have been illumination, but many others followed. It may begin with the authorisation and settlement of a payment, but ultimately the data flow and consequences will be far more profound.

I think Ali is right about the direction. The point on which I want to part company gently is the timing of the word “ultimately.”

His own operating decisions tell the story. Lesaka serves around 120,000 merchants across South Africa and several neighbouring markets. Its competitive proposition is not that the data exhaust will make those merchants better operators. It is that cash is expensive to handle and unsafe to hold; that traditional digital settlement takes days and so a merchant who needs working capital tomorrow cannot use yesterday’s till receipts; and that once the merchant has a digital float, Lesaka can extend credit against it and connect it to supplier payment rails so the float is genuinely deployable. The Bank Zero acquisition closes the last gap, which is the cost of funding the credit book. At a fundamental level, this is plumbing. Settlement, supplier rails, credit, ARPU expansion. The data will accrue along the way, but the work today is building the conditions under which digital payments cost less than cash for the merchant accepting them.

This is also where my disagreement with the cashless advocacy narrative sits. The argument I hear most often is that African merchants should digitise because the data will help them run better businesses. The argument one of the most successful operators in the region is actually executing is that African merchants will digitise when settlement is instant, when cash handling becomes a liability rather than a convenience, and when the rails enable credit they cannot otherwise access. Those are the two pull factors. The data story arrives later, on the same arc that took American retail four decades from Walton’s pickup truck in 1972 to Walmart Connect in 2021.

For now, traders and retailers in Africa are operating on the toolkit appropriate to their stage of the curve. The data layer will come. It will not be summoned by digitising payments ahead of the network it depends on, and it will not be the reason merchants finally make the switch. The reasons will be more prosaic, and they will be more decisive, and they will look a great deal like the things Ali is already building.