# 113 - The Foundation That Was Never Built

What Victorian England's friendly societies, a Rwandan health scheme, and a failed Kenyan car company reveal about why insurtech in Africa is solving the wrong problem.

Illustration by Mary Mogoi

Hi all - This is the 113th edition of Frontier Fintech. A big thanks to my regular readers and subscribers. To those who are yet to subscribe, hit the subscribe button below and share with your colleagues and friends.

In Partnership With

Ambitious lenders in emerging markets hit the same wall. The loan book grows, the product roadmap expands, and then the core banking system - built for a bank in Frankfurt or Singapore - becomes the bottleneck.

Fee structures that don't map to local amortisation conventions. Regulatory reporting workflows that require expensive custom builds every time the central bank issues a new circular. Product releases that take nine months when your competitors are iterating in nine weeks.

The problem is not unique to one market. It shows up in Nigeria, Indonesia, the Philippines, Vietnam, anywhere lending is growing fast, regulations are dynamic, and the distance between what the business needs and what the platform supports keeps widening.

Oradian is built for this. A cloud-native core banking platform designed specifically for the realities of high-growth lending markets, flexible fee structures, configurable product logic, teams that understand your context and regulatory-ready workflows out of the box. FairMoney, one of Nigeria's leading digital lenders, chose Oradian precisely because scaling their loan book required a platform that understood their market, not one that had to be coerced into it.

If you're building a lending business that intends to grow fast, your core banking infrastructure is either an accelerant or a ceiling.

Discover how Oradian powers the world's most ambitious lenders.

We’ve updated our advisory deck to reflect the interesting work we’ve been doing. Check it out below.

Work with us to find your next great executive - We have the context and the infrastructure. Powered by Triage

Click the link below for media enquiries

Introduction

In 2015, a Nairobi-based startup called Mobius Motors launched what it described as Africa’s first purpose-built vehicle. The pitch was compelling in the way that many African tech pitches are compelling: the continent has unique conditions, rough roads, dispersed populations, limited service infrastructure, and the vehicles designed for European and American highways are poorly suited to them. Mobius would build something different. Stripped down, durable, designed from first principles for African terrain. The company raised millions in funding, generated significant press, and spent years refining its engineering. However, despite all this, it closed its doors in 2021.

What killed Mobius was not bad engineering. By most accounts the vehicle worked. What killed it was a misdiagnosis of the problem it was trying to solve. The assumption embedded in Mobius’s entire existence was that African consumers and traders were waiting for someone to build them the right vehicle, that the market had identified a need and was passively sitting with an unmet one. This assumption was wrong. African market participants are not passive. They had already found their vehicle, and they had found it long before Mobius arrived.

A Toyota Probox in the wild doing Probox things

The Toyota Probox is a small Japanese station wagon, originally designed as a sales rep’s car for urban Japanese roads. It is not built for African conditions. It has modest ground clearance, a small engine, and parts that were never intended for the punishment of unpaved highland roads or the humidity of coastal trade routes. None of this has stopped it from becoming the dominant light transport vehicle across Africa. In Kenya, Proboxes carry khat from Meru to Nairobi, leaving before dawn and arriving while the city is still waking up, because the freshness of the leaf is the product. Rwandan and Burundian food traders use them to move produce across border crossings that larger vehicles can’t navigate efficiently. They serve as taxis, delivery vehicles, small business workhorses, and family cars simultaneously. They are everywhere because they are cheap to buy, cheap to run, cheap to repair, and understood by every roadside mechanic from Kisumu to Kigali. Toyota didn’t set out to build the Probox for Africa, much like they didn’t set out to build the Land Cruiser for Sahelian Rebel Groups. Nonetheless, the Probox found significant and enduring product market fit amongst Africa’s merchant class.

This story, I find, is very useful for discussing product market fit. Whenever I speak to founders, I like to review the assumptions made and compare them to the Mobius assumptions. I have tremendous respect for the Mobius guys. What they accomplished, very few ever will. The Probox story makes me think of insurance and whether Insurtechs are approaching the industry much in the same way that Mobius approached the transport industry. Building an elegant problem based on inaccurate assumptions.

The big challenge in African insurance is one of pricing risk adequately so as to sustain a profitable insurance industry. We have so far failed at this as a continent. Some may argue that it’s because of very robust communal risk management mechanisms.

In this case, the Probox analogy only goes so far, however. Because unlike vehicle transport, where the informal solution genuinely works and continues to work, Africa’s communal risk management systems are showing serious cracks. The Busara Center for Behavioural Economics studied M-Changa, Kenya’s largest digital fundraising platform and the modern evolution of the harambee, and found that the majority of completed medical campaigns raised between zero and twenty-five percent of their stated targets. NASASA, the National Stokvel Association of South Africa, acknowledged in its own publications that burial societies frequently cannot cover funeral costs in full and that liquidity problems leading to disbandment are common. Families across Kenya are surrendering title deeds and vehicle logbooks as hospital collateral because neither their insurance nor their chama has covered the bill. The Probox is starting to break down, and unlike a Probox, you can’t fix it at a roadside garage.

The instinctive industry response has been to build better insurance products, more accessible, more digital, more embedded. I want to argue that this is the Mobius mistake made again: a product solution to what is fundamentally an infrastructure problem. To understand why, we need to go back to the moment when a very similar communal risk system, in a very different part of the world, faced the same structural failure, and what it actually took to fix it. That story starts not with technology, not with regulation, and not with consumer behaviour. It starts with mathematics.

In this article, we’ll trace how communal risk management evolved from the friendly societies of industrial England into the modern insurance industry, and map that history onto the chamas and stokvels of contemporary Africa. We’ll examine what broke the friendly society model, what the British government did in 1911 to replace it, and why the structural pressures that destroyed it bear an uncomfortable resemblance to what Africa’s communal systems are facing today. We’ll then look at Rwanda’s attempt to build insurance infrastructure from the State up, and Kenya’s more troubled experiment with the same instinct. We conclude with a simple argument: Africa’s insurance problem is not a product problem or a distribution problem. It is a foundational one, and until the foundation is addressed, building insurtech on top of it is a category error.

The Oddfellows and the Chama — The Same Idea, A Century Apart

In the industrial towns of 19th century England, the working class developed an answer to a problem that no government, no employer, and no charity had solved: what happens to a man’s family when he gets sick and cannot work? The answer they built was The Friendly Society. By the 1870s, there were over 32,000 registered friendly societies in England with roughly four million members , the largest working-class institution in the country. They bore names that mixed the grandiose with the earnest: the Independent Order of Oddfellows Manchester Unity, the Ancient Order of Foresters, the Hearts of Oak Benefit Society. They were, in the assessment of the historian David Neave, “the largest and most representative working-class organisation” of their era.

Image Source - History Hit

The mechanics were straightforward and the logic was sound. Members paid fixed contributions, usually collected annually or semi-annually, into a collective fund. In return, they received sickness benefits if they could not work, and a death benefit that covered a respectable funeral and left something for the widow. Membership was not open to all. Joining required an application and the written approval of the Grand Master of the local lodge, a process that served, as the LSE’s Nicholas Broten observed in his study of the Foresters’ archives, as “both a social and medical deterrent, ensuring that high-cost members were unable to join.” The societies met monthly, usually at the local public house, to collect dues, hear claims, and conduct the social business that was as important as the financial one. A clergyman of the period, not entirely admiringly, captured what these gatherings actually were:

“All who are familiar with friendly societies know very well that they mean a great deal more than the mere payment of certain premiums and the reception in time of need of certain equivalent benefits. They know that they are clubs in another sense of the word also. The name is associated in their minds with bands and banners, and processions with scarves and rosettes, with public house dinners and all their natural concomitants.”

Strip away the rosettes and the public house dinners, and you have described, with remarkable precision, the Kenyan chama and the South African stokvel. The social aspect of the Stokvels that to a great degree mirrors the concerns that the clergyman raised are best captured in this song from 13 years ago. The singers represent the social aspect of the Stokvels as more of a social phenomenon than an economic one. In their words “Fill up the tables, count the empties”.

The chama, from the Swahili word for group, is a rotating savings and risk-sharing collective, typically between ten and thirty members who know each other personally. Members contribute fixed amounts on a regular schedule. The pool is used both for savings rotation and for welfare payments when a member faces an emergency: a hospitalisation, a funeral, a sudden loss of income. Membership requires the approval of existing members. The group meets regularly, monthly is common, to collect contributions, discuss business, and maintain the social bonds that make the financial mechanism work. Burial societies in South Africa operate on almost identical principles: fixed monthly contributions, payouts on death, membership vetted by existing members, regular gatherings that are as much social as financial. There are an estimated 800,000 stokvels in South Africa with roughly eleven million members, aggregating approximately R50 billion annually. In Kenya, chama participation is woven into professional, religious, and neighbourhood life in a way that is difficult to overstate. Most Kenyan adults who have held a formal job have been members of at least one.

The structural similarity between the Oddfellows and the chama is not coincidental. Both emerged from the same underlying conditions: predominantly informal employment, irregular income, the absence of state social protection, and communities tight-knit enough that members could observe each other’s behaviour and verify each other’s claims. This last point is the key mechanism. The friendly society and the chama both solve the problem that formal insurance calls adverse selection, the tendency for sick people to seek coverage more than healthy ones, not through actuarial pricing but through social knowledge. Social visibility does the work that mathematical pricing does in a formal insurance market, and it does it at zero administrative cost.

The institutions are separated by two centuries and an ocean. The problem they are solving, and the mechanism they use to solve it, are the same.

When the Model Breaks - It Always Does

The friendly societies ultimately collapsed. Like most of these things, the reasons why they collapsed are very clear in hindsight. The economics of the model simply couldn’t withstand the massive societal changes that were taking place.

The societies priced their contributions on intuition rather than mathematics. A lodge in Manchester in 1850 would set its weekly dues based on rough observation, what seemed like enough to cover a few weeks of sickness benefit and a decent funeral among men of roughly similar age and health? This worked tolerably well when membership was young, communities were geographically stable, and medical science had few expensive interventions to offer. It stopped working when all three conditions changed simultaneously.

Medical improvements meant British workers were living significantly longer. The sickness benefits designed to cover a few months of working-age illness slowly transformed, for aging members who could no longer work at all, into functionally indefinite pensions. The lodges had priced for illness. They had not priced for elderly members drawing benefits continuously for years. By the late 1880s, official actuaries had identified the problem with clinical precision: the societies were charging fixed contributions regardless of age or risk profile, generating what they described as “too much benefit for too little contribution.” By 1897, official summaries determined that only 4% of friendly societies were genuinely solvent.

Simultaneously, urbanisation broke the social enforcement mechanism. As industrialisation accelerated migration, the intimate lodge, where the Grand Master knew every member personally, gave way to large national federations. The visibility, the reciprocity, the threat of community ostracism for a false claim: all of it degraded in proportion to anonymity. Younger, healthier members, once they understood their contributions were subsidising an ageing cohort they barely knew, began to defect. The good risks leave the pool, the pool becomes more expensive, which accelerates further defection, until the mathematics become terminal.

The British government’s response in the National Insurance Act of 1911 was not to replace the friendly societies. It was to build the infrastructure their own model could not generate: compulsion to solve adverse selection, standardised actuarial tables from the newly formalised Government Actuary’s Department, and a state guarantee shifting catastrophic risk onto the sovereign balance sheet. The societies were incorporated as “approved societies”, their community trust networks intact, but the mathematical architecture underneath them now state property.

The structural parallels with contemporary Africa are traceable in data being collected right now.

The disease burden is shifting from the acute shocks that communal pools were built for, funerals, seasonal illness, agricultural disruption, toward chronic, expensive, ongoing conditions. Cancer, diabetes, cardiovascular disease, renal failure. A burial society sized to cover a funeral is woefully unable to cover a terminal disease like cancer.

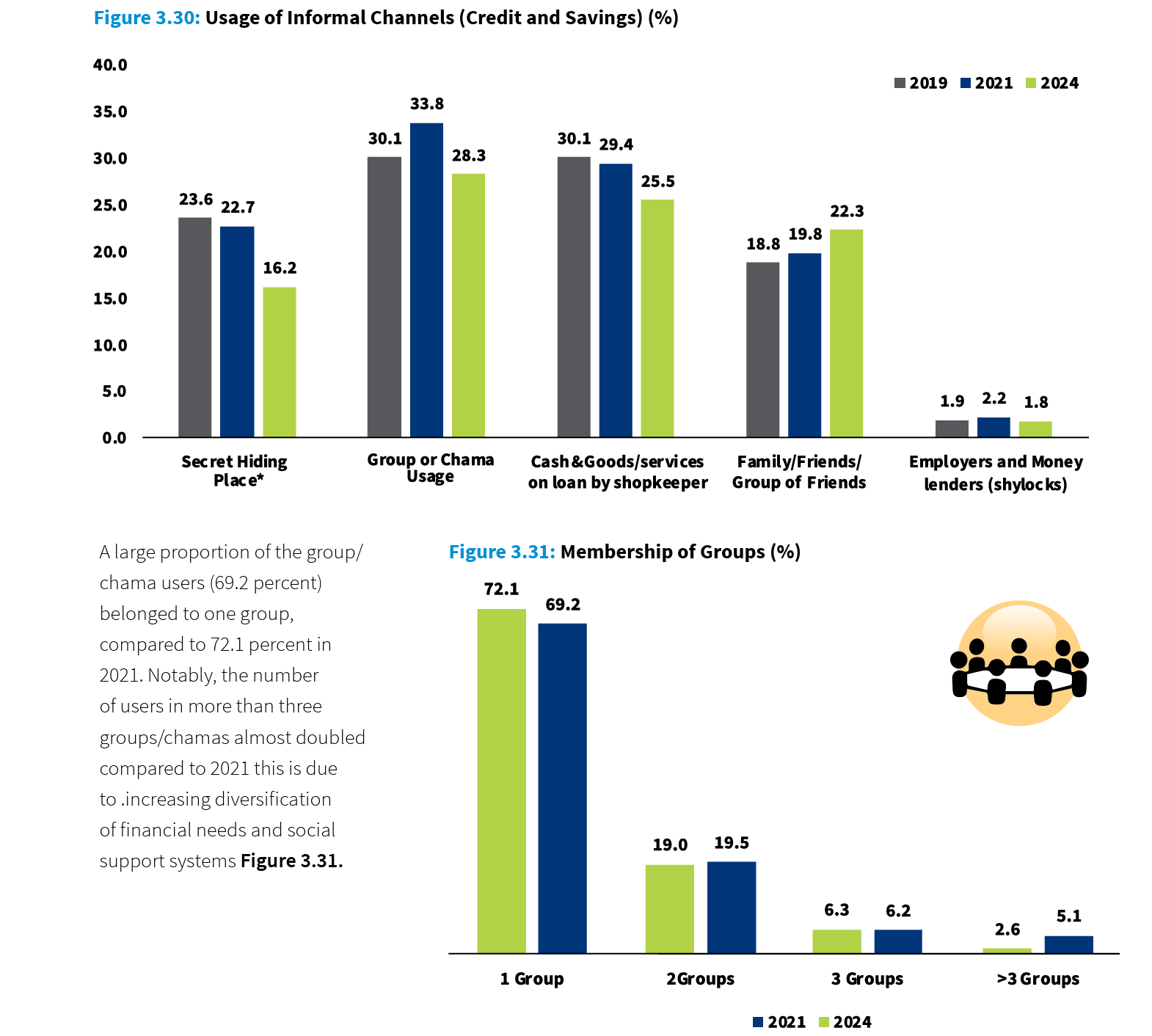

Urbanisation is eroding the social collateral that made these systems work. Sub-Saharan Africa’s urban population is projected to nearly double over the next twenty-five years. The FinAccess 2024 survey found that the proportion of Kenyans participating in more than three chamas simultaneously had almost doubled since 2021, not a sign of deepening community, but of desperation. A single pool can no longer cover modern financial shocks, so people fragment their contributions across multiple groups hoping the aggregate is sufficient. It rarely is. The same survey found nearly 29% of Chama participants reporting unexpected charges or friction, the internal strain of institutions being asked to do more than they were designed for.

Image Source: Central Bank of Kenya FinAccess Survey 2024

Medical inflation has run amok in the continent and it’s increasingly beyond the reach of the normal citizen. Given such a situation, chamas become irrelevant. The M-Changa data makes this precise: the majority of completed medical fundraising campaigns on Kenya’s largest digital harambee platform raised between zero and twenty-five percent of their stated targets. The community tried. The mathematics of the problem had simply outgrown the mathematics of the solution.

The formal insurance industry has not filled this gap. Kenya’s insurers ran a combined ratio of 130.5% in 2024, paying out more in claims and expenses than they collected in premiums. The IRA’s claims settlement data shows third-party liability claims achieving a payment ratio of 10.96%. Nine out of every ten liability claims are not paid. I experienced this first hand. Recently I lost an aunt and the insurer did not want to settle her medical bill arguing that she was admitted for pre-existing conditions. Upon digging further into the insurance company, an insider pulled a relative aside and told him that if they were to pay such claims, the staff would go without bonuses. This is the textbook definition of market failure.

The Foundation that Africa Never Built

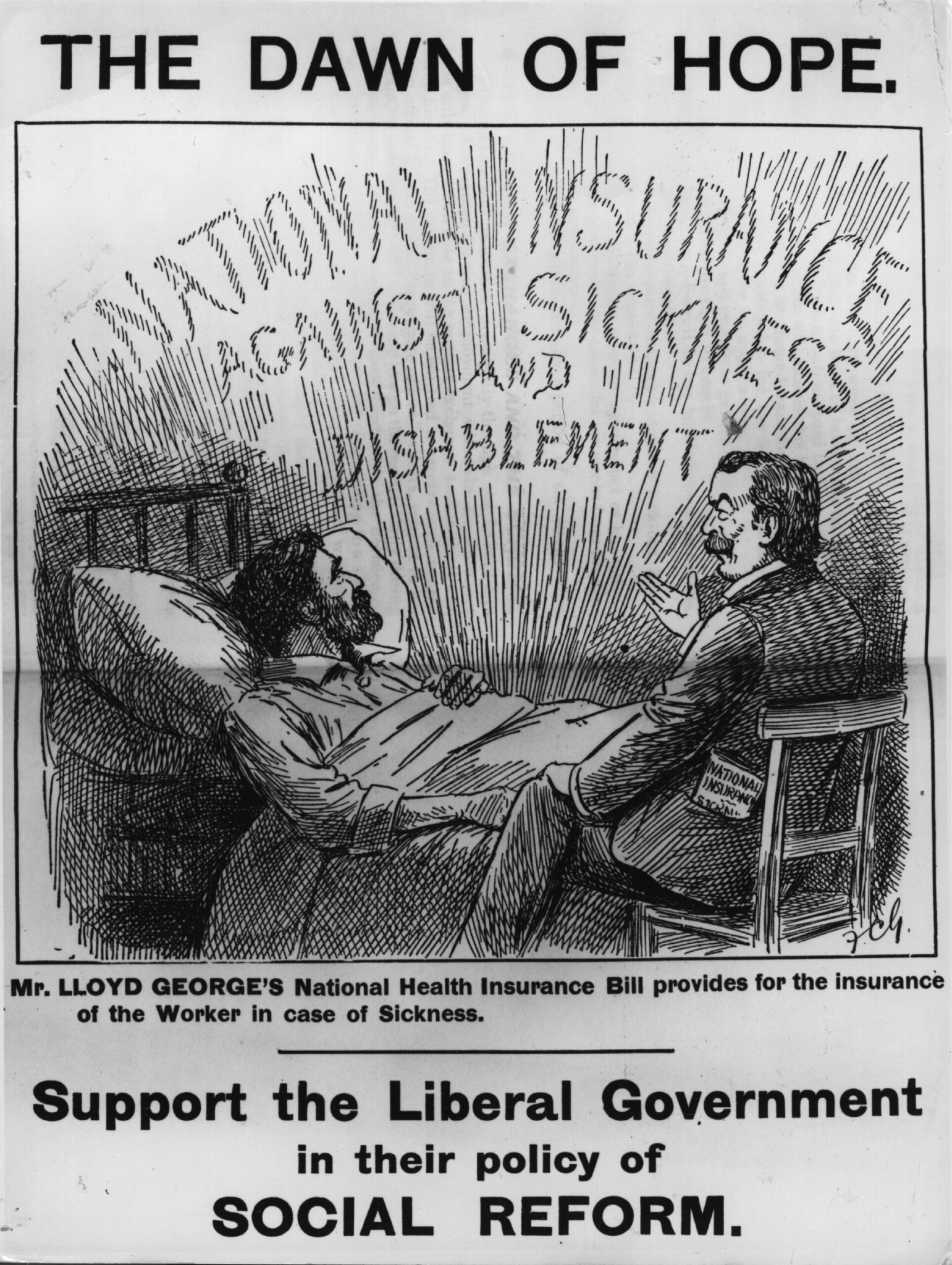

The British made major reforms to avert the Friendly Society Crisis. These were encapsulated in the National Insurance Act of 1911. At its core, it was a data infrastructure project disguised as social policy rather than a welfare program.

Three reforms followed in sequence, each addressing a distinct failure that voluntary mutual insurance had proven structurally unable to solve.

Image Source: New Statesman Archive

The first was data. The Government Actuary’s Department, formalised in the years surrounding the Act, was tasked with producing national mortality and morbidity tables that no individual society or insurer had been able to generate alone. These tables were built from decades of census records, death registrations, and hospital data that the British state had been systematically collecting since 1801. They answered the foundational question that friendly societies had been guessing at for a century: how many people of a given age, sex, and occupation will fall sick or die in a given year, and what will it cost? With that answer, premiums could be set correctly and reserves calculated accurately. The product could be priced to actually work.

The second was compulsion. Lloyd George’s genius was to understand that voluntary insurance pools always die the same death, healthy people opt out, the pool fills with the sick, costs rise, more healthy people leave. His solution was to make the choice disappear entirely. The National Insurance Act mandated participation for all employed workers. To secure working-class support for what was, in effect, a new tax, Lloyd George crafted one of the most memorable political formulas in British legislative history: the worker would contribute fourpence per week, the employer threepence, and the state twopence, “ninepence for fourpence,” as he put it on the floor of the House of Commons. The worker was getting more than double their contribution back in state-backed coverage. The political arithmetic worked because the economic arithmetic worked. Healthy young people who would never have voluntarily entered a risk pool were now inside it, balancing the pool, making the pricing hold.

The third was claims governance. The approved societies framework, through which friendly societies administered the scheme as regulated agents of the state, introduced for the first time a standardised, enforceable contract between insurer and insured. When a society defined a benefit and collected a contribution for it, it was now legally bound to honour it. As one contemporary actuary put it with pointed simplicity: “When a society by its rules offers benefits in exchange for certain fixed contributions, it is to be supposed that it looks upon those contributions as being enough to provide for the benefits; otherwise it would be dishonestly holding out promises which it cannot keep.”

These three interventions, public actuarial data, compulsory participation, and enforceable claims governance, are what transformed insurance from a product that occasionally worked into an industry that structurally could not fail the way the friendly societies had. Every mature insurance market in the world sits on this foundation.

The question for Africa is whether that foundation exists. Outside South Africa, it largely does not. The Actuarial Society of Kenya was founded in 2010 and today has fewer than 200 fully qualified fellows serving an entire national insurance industry. Nigeria’s actuarial profession is smaller still. The continent’s actuarial capacity is so concentrated in South Africa that ASSA holds over 90% of Africa’s qualified actuaries, which goes a long way toward explaining why South Africa’s insurance penetration sits at roughly 12% of GDP while Kenya and Nigeria hover at or below 2%.

The consequences are visible in the financials. Kenya’s insurers ran a combined ratio of 130.5% in 2024. They are not merely unprofitable, they are pricing products they cannot accurately cost. When an insurer cannot build a credible mortality table for informal workers who constitute 80% of the population, it either overprices to cover the uncertainty, excluding the mass market, or it underprices and absorbs losses that eventually destroy its reserves. African insurers have done both, sometimes simultaneously across different product lines.

The adverse selection problem has never been structurally resolved. With no compulsion mechanism outside narrow employer-mandated schemes, insurance pools across the continent are disproportionately composed of people who already know they are sick or at high risk. The healthy majority opt out, exactly as the young members of the Oddfellows did in the 1880s. The pool deteriorates. Premiums rise. More healthy people leave.

Lloyd George understood that you cannot build an insurance industry by designing better products. You build it by creating the conditions under which products can be priced honestly, pools can be balanced compulsorily, and claims can be paid consistently. Africa has built neither the data infrastructure nor the compulsion mechanism. What it has built, in their absence, is an industry that looks like insurance but functions like something considerably less reliable. This is particularly relevant as the continent urbanises.

The Rwandese and Kenyan Experiments

Rwanda and Kenya represent the two most instructive attempts on the continent to do what Lloyd George did, build the architecture underneath the communal instinct rather than replace it. One understood the sequencing. The other is still working it out.

Rwanda’s Mutuelle de Santé, launched as a pilot in 1999 and scaled nationally through the 2000s, followed the Lloyd George logic with remarkable fidelity. The state solved adverse selection first, making health insurance a legal requirement for all residents through Law No. 48/2015. Opting out meant losing access to public health facilities, a compulsion mechanism that required no enforcement bureaucracy, only a functioning health system that checked cards at the door. Rwanda then solved the pricing problem not by training an army of actuaries it didn’t have, but by deploying the Ubudehe poverty classification system, a community-validated database that slotted every household into a tier and set their premium accordingly. The poorest paid nothing, subsidised by a treasury injection of 6 billion Rwandan Francs (US$ 4 million) annually, supplemented by levies on traffic fines and telecommunications fees. The cross-subsidy was explicit and politically managed. And crucially, twenty-five years of centralised claims data flowing through the Rwanda Social Security Board has created what no private insurer on the continent has managed to build alone: a national actuarial dataset on low-income health utilisation that any insurer entering Rwanda can actually use. Coverage reached 91% of the population. It’s a simple example of the positive externalities that accrue when you get the infrastructure right.

Kenya’s SHIF experiment has the right instinct and the wrong order. The Social Health Insurance Fund mandates participation, increases contributions to 2.75% of gross salary for formal workers, and ambitiously targets informal sector inclusion through a means-testing instrument. On paper, it is attempting all three of Lloyd George’s interventions simultaneously. In practice, only 27% of informal workers, who constitute over 80% of Kenya’s workforce, are enrolled. The SHA portal excludes most hospitals where ordinary Kenyans actually seek care from accessing the emergency fund. Hospitals, burned by billions in unpaid NHIF claims, now demand cash upfront before treating SHA patients. The rails were not built before the trains were set running.

Lloyd George spent a decade building the data infrastructure, the actuarial tables, and the claims governance framework before the National Insurance Act came into force. Rwanda spent the better part of a decade piloting Mutuelle before mandating it nationally. Kenya launched SHIF and is now attempting to build the foundation underneath a system already in motion. The difference in outcomes is not a surprise.

It’s the Fundamentals

There is a useful comparison hiding in plain sight. When Nubank launched in Brazil in 2013, it did not need to invent the concept of a bank account. It did not need to prove that money could be stored, transferred, or lent. It did not need to convince regulators that deposits should be guaranteed or that interest rates needed a benchmark. The Banco Central do Brasil had spent decades building that architecture. IFRS accounting standards told Nubank how to reserve against its loan book. The CPF system gave it a national identity layer. Credit bureaux gave it pricing data. Nubank’s genuine innovation was distribution and experience , a better interface on top of a proven foundation. The same is true of every neobank that has scaled meaningfully, from Monzo in the UK to TymeBank in South Africa to Moniepoint in Nigeria. They are all, in the end, riding rails that somebody else built.

Digital insurance in Africa has no equivalent foundation to ride. There is no national actuarial dataset giving insurers a credible pricing base for the informal majority. There is no compulsion mechanism ensuring that healthy people enter the pool alongside the sick. There is no fast, low-cost claims enforcement architecture that makes the insurance contract credible to a consumer who has learned, correctly, that claims get disputed. The insurtechs building in this space are not riding existing rails. They are being asked to lay the track, run the train, and sell the tickets simultaneously, and then blamed for not moving fast enough.

This is the Mobius mistake, made with the best intentions. Building an extremely elegant solution to a problem that has largely been fixed.. The insurtechs risk the opposite error: they are building elegant products for a market whose foundations are genuinely broken, and no amount of product sophistication resolves a structural absence. I wrote about the Agri-tech story here and insurtech largely rhymes with it.

The window for African insurance to find real product-market fit is opening. Urbanisation, medical inflation, and the visible fracturing of communal risk systems are creating a genuine demand that did not exist at scale a generation ago. But the lesson of Lloyd George, and of Rwanda, is that the sequence matters as much as the intent. The data infrastructure, the compulsion mechanism, the claims governance architecture; these are not features that the market will eventually build. They are the preconditions without which the market cannot exist. Without these, then insurtech is an exercise in window dressing and will struggle to scale.

This is a thoroughly informative article. Why then, does any government try to touch health insurance when it's clearly unworkable and politically toxic?